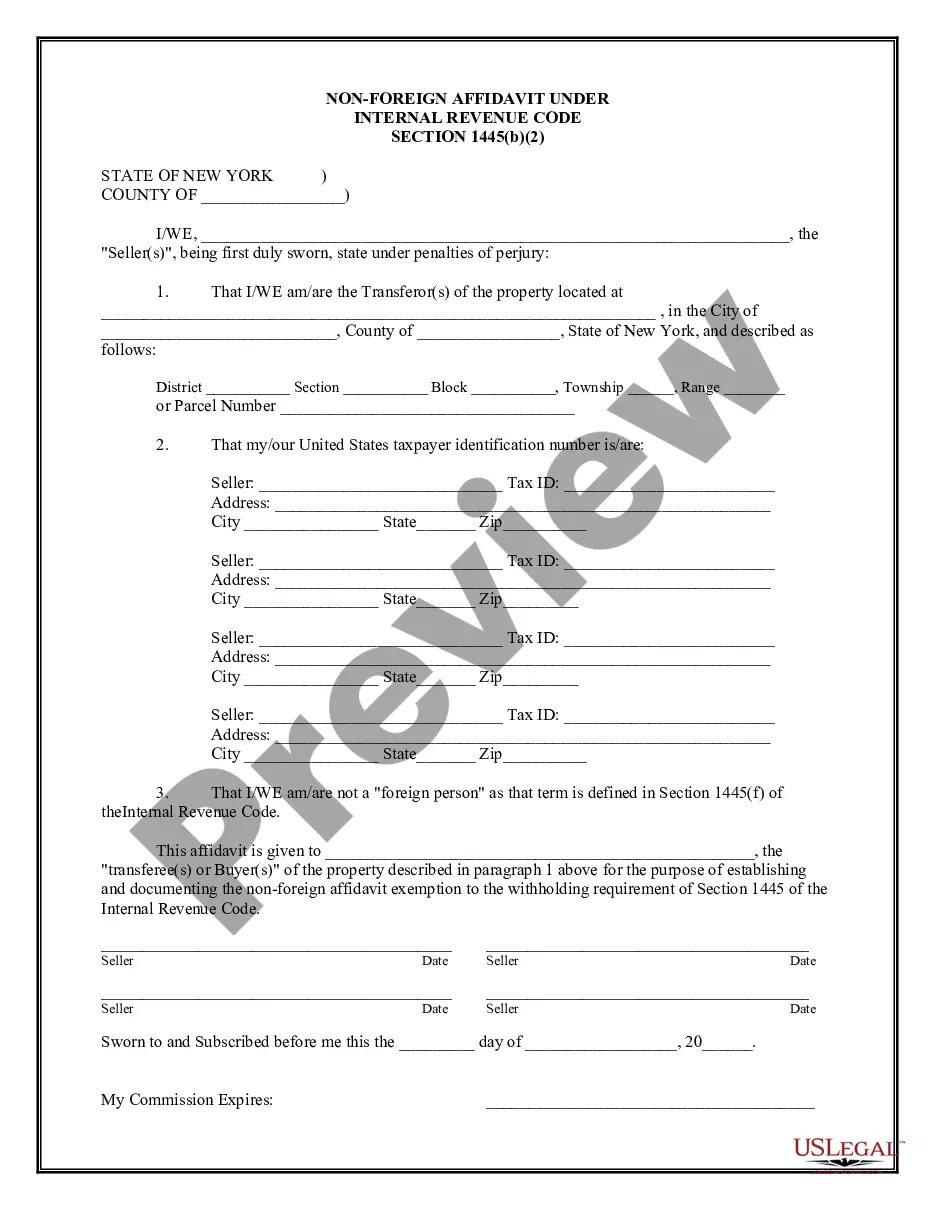

New York Non-Foreign Affidavit Under IRC 1445

Description Identification Affidavit

How to fill out New York Non-Foreign Affidavit Under IRC 1445?

In terms of completing New York Non-Foreign Affidavit Under IRC 1445, you almost certainly imagine a long process that requires finding a appropriate sample among countless very similar ones and then being forced to pay out legal counsel to fill it out for you. Generally speaking, that’s a slow-moving and expensive option. Use US Legal Forms and select the state-specific document in a matter of clicks.

If you have a subscription, just log in and click on Download button to have the New York Non-Foreign Affidavit Under IRC 1445 template.

If you don’t have an account yet but need one, keep to the step-by-step guide listed below:

- Be sure the document you’re downloading is valid in your state (or the state it’s needed in).

- Do so by reading the form’s description and by clicking on the Preview option (if offered) to see the form’s content.

- Simply click Buy Now.

- Pick the appropriate plan for your financial budget.

- Join an account and choose how you want to pay: by PayPal or by credit card.

- Download the document in .pdf or .docx format.

- Find the record on your device or in your My Forms folder.

Professional legal professionals work on creating our templates to ensure that after saving, you don't need to worry about editing content outside of your individual info or your business’s information. Sign up for US Legal Forms and get your New York Non-Foreign Affidavit Under IRC 1445 document now.

Firpta Affidavit Ny Form popularity

Firpta Other Form Names

FAQ

A: The buyer must agree to sign an affidavit stating that the purchase price is under $300,000 and the buyer intends to occupy. The buyer may choose not to sign the form, in which case withholding must be done.

The Foreign Investment in Real Property Transfer Act (FIRPTA) requires any buyer of a U.S. real property interest to withhold ten percent of the amount realized by a foreign seller. 26 USC § 1445(a).

FIRPTA is a federal tax law that ensures that foreign sellers pay income tax on the sale of real property in the United States.

Persons purchasing U.S. real property interests (transferees) from foreign persons, certain purchasers' agents, and settlement officers are required to withhold 15% (10% for dispositions before February 17, 2016) of the amount realized on the disposition (special rules for foreign corporations).

CERTIFICATE OF NON FOREIGN STATUS. Section 1445 of the Internal Revenue Code provides that a transferee (buyer) of a U.S. real property interest must withhold tax if the transferor (seller) is a foreign person.

What Is a Certification of Non-Foreign Status? With a Certification of Non-Foreign Status, the seller of real estate is certifying under penalty of perjury, that the seller is not foreign. Therefore, the seller and the transaction will not have the withholding requirements.

FIRPTA Exemptions The sales price is $300,000 or less, and. The buyer signs affidavit at or before closing stating they intend to use property for personal purposes for at least 50% of time property occupied for the each of the first two 12 month periods immediately after closing.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) income tax withholding. FIRPTA authorized the United States to tax foreign persons on dispositions of U.S. real property interests.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445).Withholding is required on certain distributions and other transactions by domestic or foreign corporations, partnerships, trusts, and estates.