- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

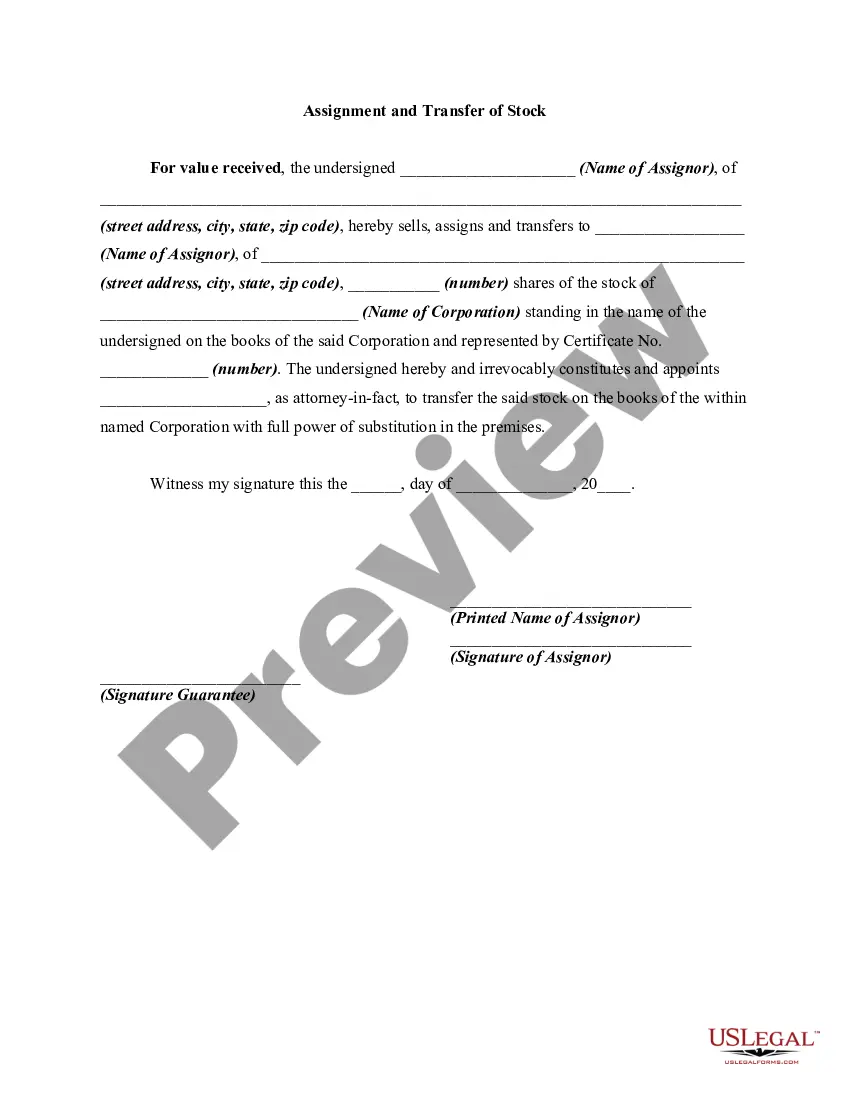

The following form is a gift to a family member of stock in a business owned by the donor.

In the context of New York, a "Gift of Stock Interest in Business to Family Member" refers to the transfer of ownership or equity interest in a business entity to a family member as a gift. It involves transferring shares or stocks of a business organization from one related individual to another without any monetary consideration. When someone gifts stocks or shares of a business to a family member in New York, they are essentially relinquishing their ownership rights and granting it to the recipient without expecting anything in return. This type of transfer is often carried out to facilitate the succession planning or estate planning strategies within a family or to provide financial support or benefits to a family member. The keyword "New York" indicates that the gift of stock interest in business is subject to the laws and regulations governing such transfers in the state. It implies that the transaction must comply with the specific statutes, rules, and requirements set forth by the New York State Department of Corporations and other relevant authorities. It should be noted that there are no specific subtypes of "Gift of Stock Interest in Business to Family Member" in New York. However, the nature of the business entity involved in the gift may differ, such as a corporation, partnership, limited liability company (LLC), or sole proprietorship. Each entity type may have its own unique considerations and implications when it comes to the transfer of stock interest. In summary, a "New York Gift of Stock Interest in Business to Family Member" is the legal process of transferring ownership or equity interest in a business to a family member as a gift without any monetary consideration. It is a strategic tool used for succession planning, estate planning, or supporting family members financially. The specific rules and regulations set forth by the state of New York must be followed throughout this transaction.