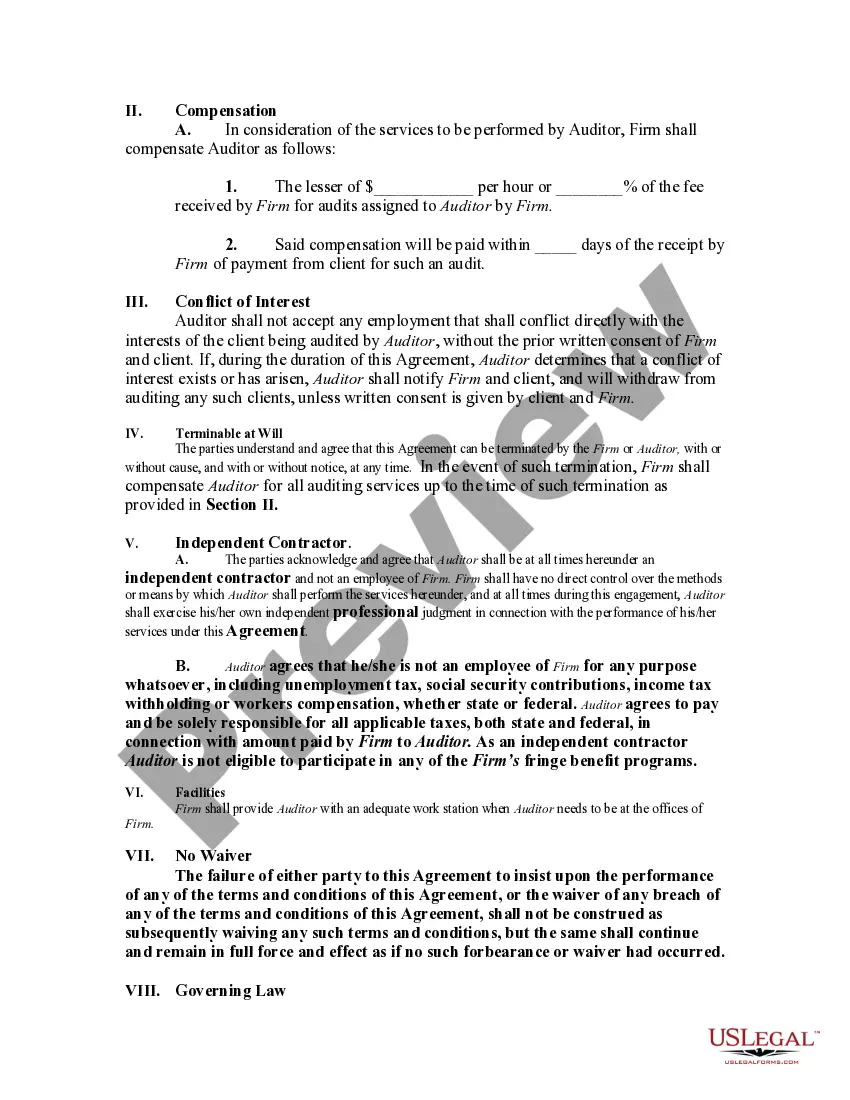

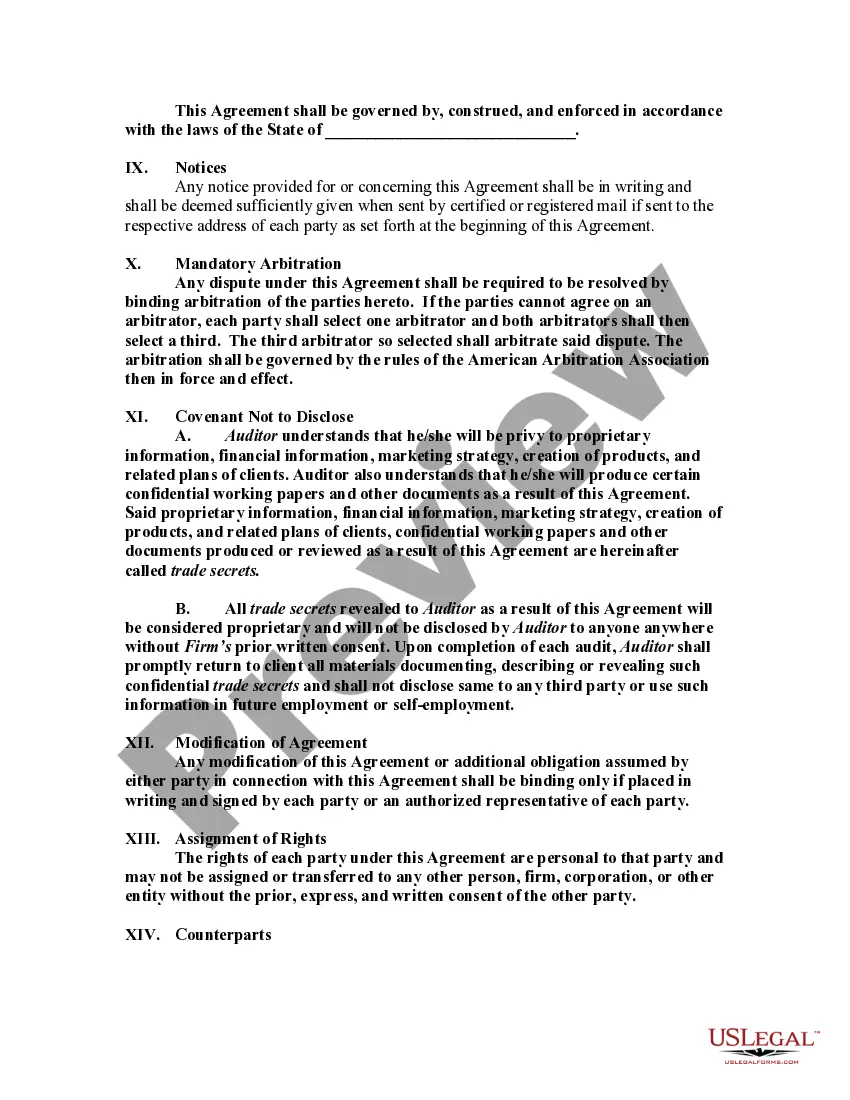

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

The New York Agreement by an accounting firm to employ an auditor as a self-employed independent contractor is a legally binding contract between the accounting firm and the auditor. This agreement outlines the terms and conditions of the engagement, establishing the independent contractor relationship. Keywords: New York Agreement, accounting firm, employ, auditor, self-employed, independent contractor Types of New York Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Standard Agreement: This is the most common type of agreement whereby the accounting firm hires an auditor as a self-employed independent contractor to perform specific tasks related to auditing services. The agreement would specify the duration of the engagement, compensation terms, scope of work, and other relevant provisions. 2. Project-based Agreement: In certain cases, an accounting firm may engage an auditor for a specific project or assignment rather than a continuous engagement. This type of agreement outlines the objectives, timelines, deliverables, and payment details associated with the project. It also establishes the self-employed independent contractor status of the auditor. 3. Non-Compete Agreement: Sometimes, an accounting firm may require the auditor to sign a non-compete agreement alongside the New York Agreement to restrict the auditor from engaging in similar audit services with the firm's competitors. This agreement sets forth the limitations and consequences of breaching the non-competition clause. 4. Non-Disclosure Agreement (NDA): An accounting firm may also include a separate NDA alongside the New York Agreement to ensure the confidentiality of sensitive information shared during the engagement. The NDA prevents the auditor from disclosing any proprietary or confidential information related to the accounting firm or its clients. 5. Termination Agreement: In the event that either party wishes to terminate the engagement before its scheduled completion, a termination agreement can be executed. This agreement outlines the reasons for termination, notice period, and any applicable financial settlement. Overall, the New York Agreement by an accounting firm to employ an auditor as a self-employed independent contractor is a critical document that governs the contractual relationship, protects the interests of both parties involved, and ensures compliance with relevant employment laws and regulations.The New York Agreement by an accounting firm to employ an auditor as a self-employed independent contractor is a legally binding contract between the accounting firm and the auditor. This agreement outlines the terms and conditions of the engagement, establishing the independent contractor relationship. Keywords: New York Agreement, accounting firm, employ, auditor, self-employed, independent contractor Types of New York Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Standard Agreement: This is the most common type of agreement whereby the accounting firm hires an auditor as a self-employed independent contractor to perform specific tasks related to auditing services. The agreement would specify the duration of the engagement, compensation terms, scope of work, and other relevant provisions. 2. Project-based Agreement: In certain cases, an accounting firm may engage an auditor for a specific project or assignment rather than a continuous engagement. This type of agreement outlines the objectives, timelines, deliverables, and payment details associated with the project. It also establishes the self-employed independent contractor status of the auditor. 3. Non-Compete Agreement: Sometimes, an accounting firm may require the auditor to sign a non-compete agreement alongside the New York Agreement to restrict the auditor from engaging in similar audit services with the firm's competitors. This agreement sets forth the limitations and consequences of breaching the non-competition clause. 4. Non-Disclosure Agreement (NDA): An accounting firm may also include a separate NDA alongside the New York Agreement to ensure the confidentiality of sensitive information shared during the engagement. The NDA prevents the auditor from disclosing any proprietary or confidential information related to the accounting firm or its clients. 5. Termination Agreement: In the event that either party wishes to terminate the engagement before its scheduled completion, a termination agreement can be executed. This agreement outlines the reasons for termination, notice period, and any applicable financial settlement. Overall, the New York Agreement by an accounting firm to employ an auditor as a self-employed independent contractor is a critical document that governs the contractual relationship, protects the interests of both parties involved, and ensures compliance with relevant employment laws and regulations.