This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

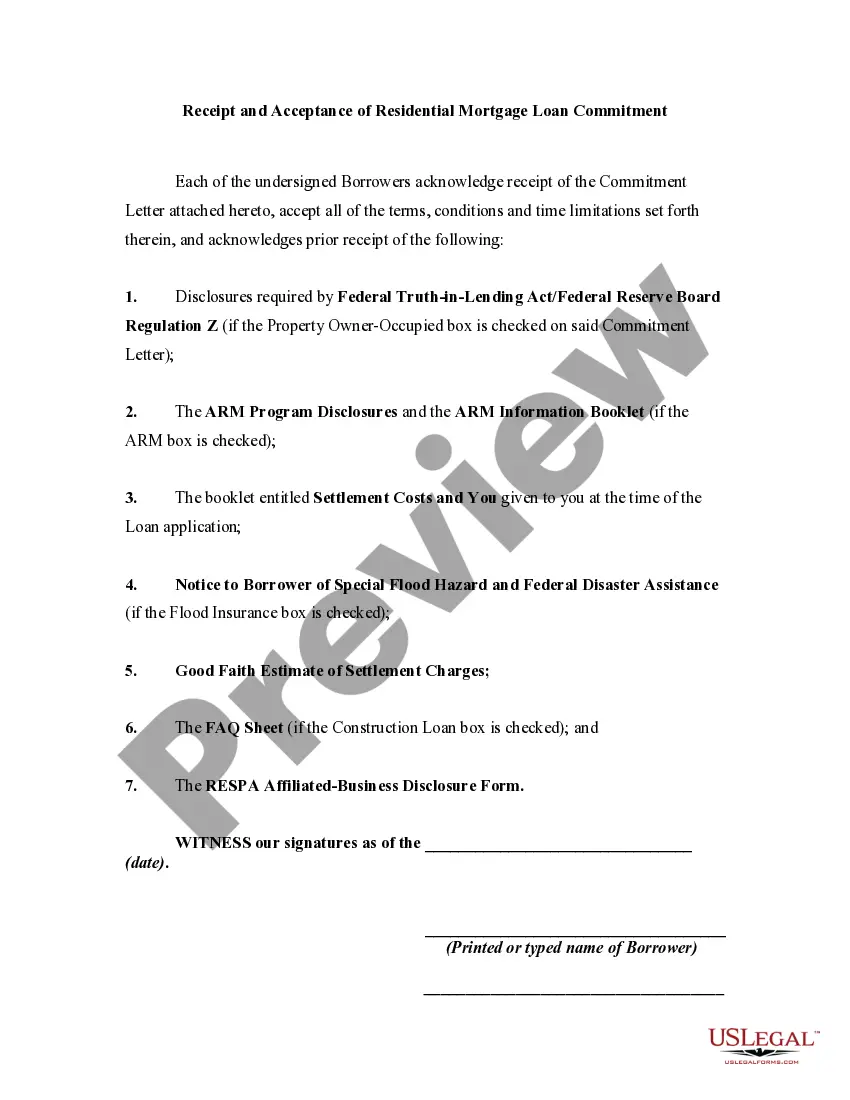

The New York Receipt and Acceptance of Residential Mortgage Loan Commitment is a legal document that serves as evidence of the borrower's receipt and acceptance of a mortgage loan commitment offered by a lender for residential property in New York. This document is an essential part of the loan origination process and outlines the terms, conditions, and obligations for both the borrower and the lender. Keywords: New York, receipt, acceptance, residential mortgage loan commitment, borrower, lender, loan origination, terms, conditions, obligations. There may be variations or different types of New York Receipt and Acceptance of Residential Mortgage Loan Commitment based on specific loan programs or types of residential properties. Here are a few examples: 1. Conventional Mortgage Loan Commitment: This type of commitment applies to a conventional mortgage loan, which is a loan that is not insured or guaranteed by a government agency such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). 2. FHA Mortgage Loan Commitment: This document is specific to an FHA-insured mortgage loan commitment, which is a loan offered by a lender that is insured by the FHA. The FHA provides mortgage insurance to protect lenders against losses in case of borrower default. 3. VA Mortgage Loan Commitment: For borrowers who are eligible for VA home loans, this type of commitment represents the acceptance of a loan commitment offered under the VA loan program. VA loans are guaranteed by the Department of Veterans Affairs and often offer favorable terms and benefits for military veterans and active-duty service members. 4. Jumbo Mortgage Loan Commitment: This version of the document applies to jumbo mortgage loans, which exceed the conforming loan limits set by government-sponsored enterprises like Fannie Mae and Freddie Mac. Jumbo loans typically have higher interest rates and stricter qualification requirements. It is important for borrowers to carefully review and understand the terms and conditions outlined in the New York Receipt and Acceptance of Residential Mortgage Loan Commitment before signing it. This document protects both the borrower's and the lender's interests and helps ensure a transparent and mutually beneficial mortgage loan transaction.