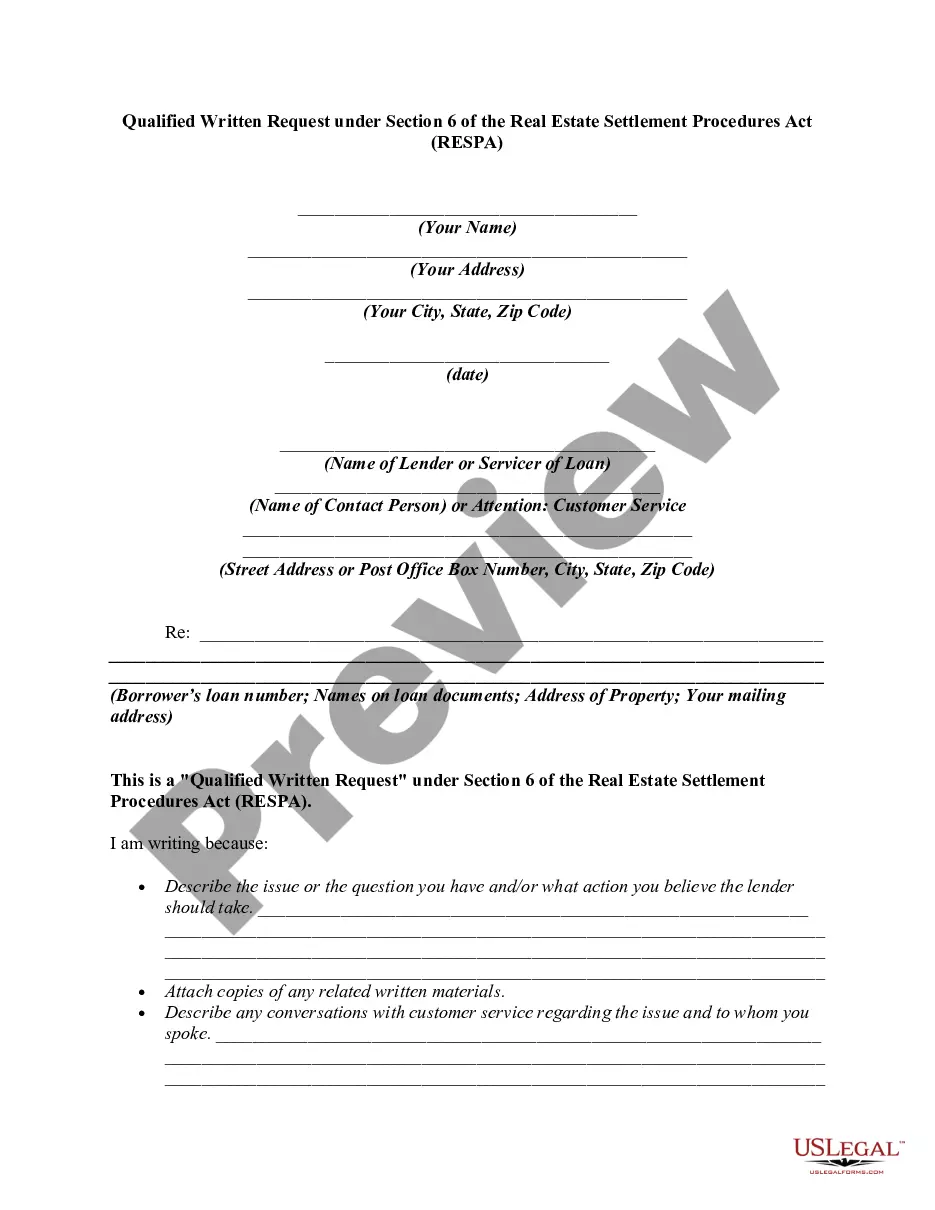

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

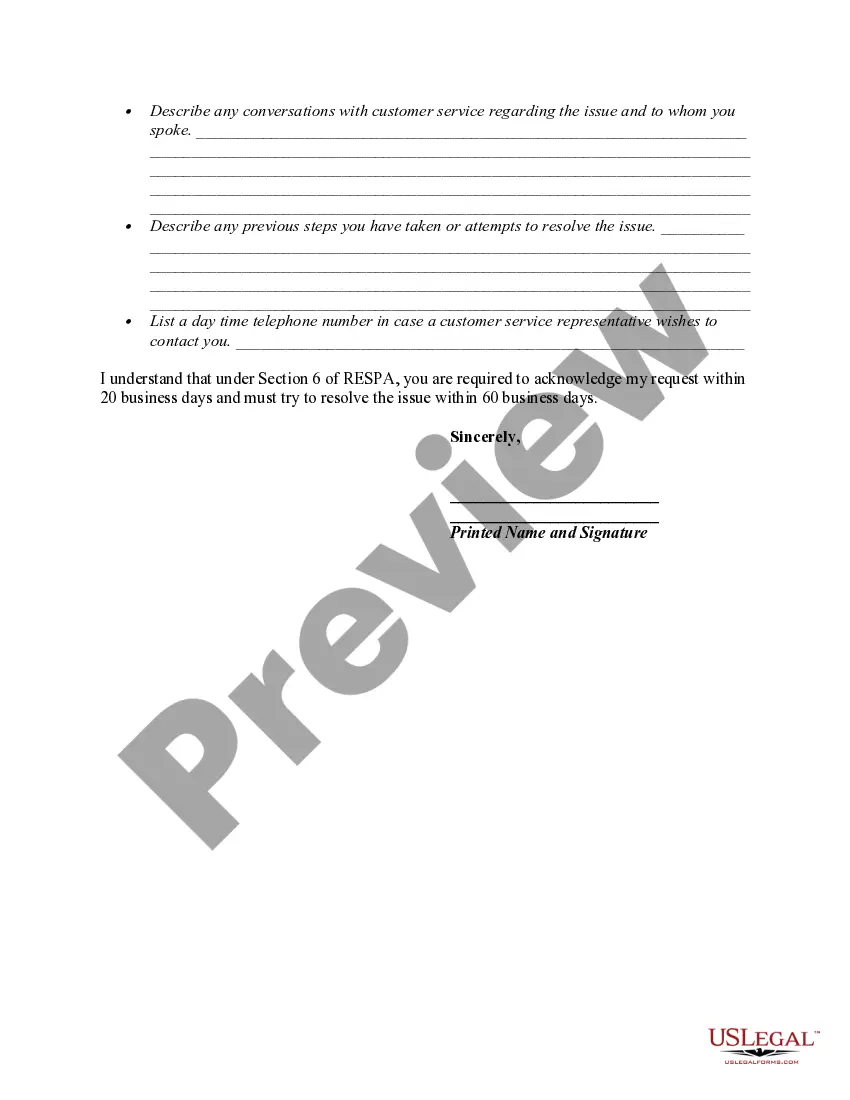

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

A New York Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) pertains to a specific type of written request that homeowners in New York can submit to their mortgage services or lenders. This legal provision, established by the Consumer Financial Protection Bureau (CFPB), grants homeowners the right to seek information and dispute issues related to their mortgage loans, ensuring transparency and fairness in the real estate market. A New York BWR, also known as a Section 6 BWR, holds significance for homeowners facing difficulties or concerns regarding their mortgages. By submitting a BWR, individuals can obtain detailed information about their loans, including payment histories, account balances, interest rates, escrow accounts, and any other relevant documents or disclosures. It is important to note that although the BWR provision applies nationwide under RESP, New York has enacted certain additional regulations and requirements for its residents. These state-specific rules aim to provide additional protection for homeowners navigating the intricate mortgage landscape. Given these added layers, it is crucial for individuals in New York to understand the nuances of the New York BWR process. There are different types of New York Was under Section 6 of RESP, namely: 1. Loan Information Request: This type of BWR allows borrowers to request comprehensive information about their loan, including specific details about the principal balance, interest rates, and terms of the mortgage. By acquiring this information, homeowners can more effectively manage their finances and assess the accuracy of the service's records. 2. Escrow Account Inquiry: Homeowners who have escrow accounts established by their mortgage services can utilize this type of BWR to gain a deeper understanding of how the service manages and allocates funds in the escrow account. This includes details about the funds held, disbursements made for property taxes, insurance premiums, and any interest accrued. 3. Error Resolution and Dispute: In case homeowners identify errors in their mortgage statements, charges, or other aspects of their loans, they can submit a BWR to resolve these issues. This type of BWR serves as a formal notice to the mortgage service, highlighting the error and demanding prompt correction or clarification. 4. Foreclosure Prevention Inquiry: Homeowners who are at risk of foreclosure or facing financial hardships can utilize this type of BWR to seek assistance and explore available foreclosure prevention options. By requesting relevant information regarding loss mitigation programs, loan modification options, or foreclosure timelines, borrowers can make informed decisions and potentially mitigate the risk of losing their homes. When submitting a New York BWR under Section 6 of RESP, homeowners should ensure compliance with specific state requirements, such as providing their loan number, contact information, a clear description of the issue, and any supporting documentation. By doing so, borrowers can effectively exercise their rights and secure necessary information or remedies related to their mortgage loans.A New York Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) pertains to a specific type of written request that homeowners in New York can submit to their mortgage services or lenders. This legal provision, established by the Consumer Financial Protection Bureau (CFPB), grants homeowners the right to seek information and dispute issues related to their mortgage loans, ensuring transparency and fairness in the real estate market. A New York BWR, also known as a Section 6 BWR, holds significance for homeowners facing difficulties or concerns regarding their mortgages. By submitting a BWR, individuals can obtain detailed information about their loans, including payment histories, account balances, interest rates, escrow accounts, and any other relevant documents or disclosures. It is important to note that although the BWR provision applies nationwide under RESP, New York has enacted certain additional regulations and requirements for its residents. These state-specific rules aim to provide additional protection for homeowners navigating the intricate mortgage landscape. Given these added layers, it is crucial for individuals in New York to understand the nuances of the New York BWR process. There are different types of New York Was under Section 6 of RESP, namely: 1. Loan Information Request: This type of BWR allows borrowers to request comprehensive information about their loan, including specific details about the principal balance, interest rates, and terms of the mortgage. By acquiring this information, homeowners can more effectively manage their finances and assess the accuracy of the service's records. 2. Escrow Account Inquiry: Homeowners who have escrow accounts established by their mortgage services can utilize this type of BWR to gain a deeper understanding of how the service manages and allocates funds in the escrow account. This includes details about the funds held, disbursements made for property taxes, insurance premiums, and any interest accrued. 3. Error Resolution and Dispute: In case homeowners identify errors in their mortgage statements, charges, or other aspects of their loans, they can submit a BWR to resolve these issues. This type of BWR serves as a formal notice to the mortgage service, highlighting the error and demanding prompt correction or clarification. 4. Foreclosure Prevention Inquiry: Homeowners who are at risk of foreclosure or facing financial hardships can utilize this type of BWR to seek assistance and explore available foreclosure prevention options. By requesting relevant information regarding loss mitigation programs, loan modification options, or foreclosure timelines, borrowers can make informed decisions and potentially mitigate the risk of losing their homes. When submitting a New York BWR under Section 6 of RESP, homeowners should ensure compliance with specific state requirements, such as providing their loan number, contact information, a clear description of the issue, and any supporting documentation. By doing so, borrowers can effectively exercise their rights and secure necessary information or remedies related to their mortgage loans.