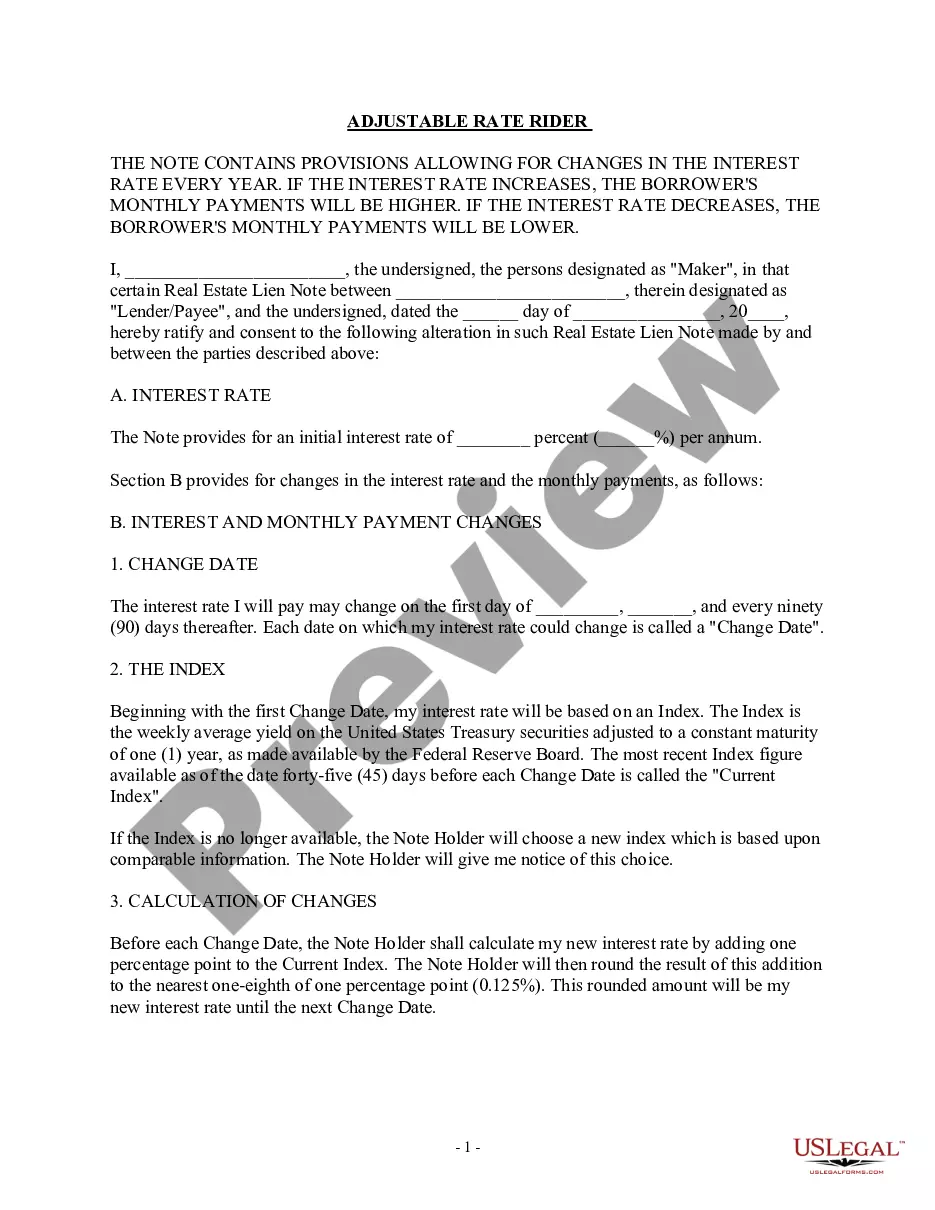

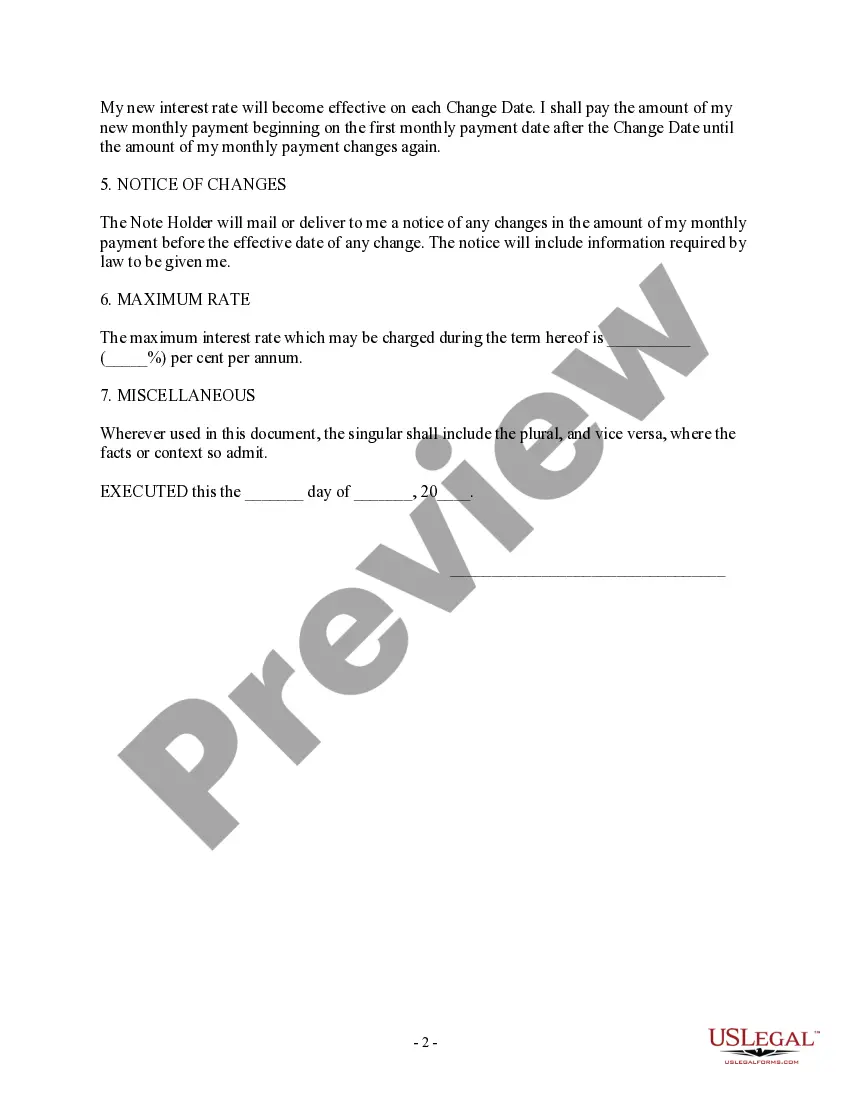

The New York Adjustable Rate Rider — Variable Rate Note, also known as the NY ARR, is a legal document that serves as an addendum to a mortgage agreement. It offers borrowers in New York the option to secure a mortgage with an adjustable interest rate, providing both flexibility and potential savings. This type of rider allows borrowers to take advantage of changing market conditions and interest rates. Unlike a fixed-rate mortgage, where the interest rate remains constant throughout the loan term, the NY ARR features a variable interest rate that can fluctuate over time. However, it typically starts with an initial fixed rate period, offering stability in the early years. The New York Adjustable Rate Rider — Variable Rate Note enables lenders to adjust the interest rate periodically, based on changes in an agreed-upon index, such as the US Treasury bill rate or the London Interbank Offered Rate (LIBOR). These adjustments usually occur annually, semi-annually, or even monthly, depending on the terms agreed upon by the lender and the borrower. It's important to note that the NY ARR includes various terms and conditions that borrowers should fully understand before signing. Some of these key components include the interest rate adjustment frequency, the index chosen to determine the rate changes, and any interest rate caps or floors that limit how much the rate can increase or decrease in each adjustment period. Additionally, the rider discloses the margin, which is a fixed percentage added to the index value to calculate the applicable interest rate. New York presents different types of Adjustable Rate Riders — Variable Rate Note designs that cater to the diverse needs of borrowers. Some common variations include: 1. Initial fixed-rate period ARM: This type of NY ARR allows borrowers to secure a mortgage with a fixed interest rate for an agreed-upon period (e.g., 5, 7, or 10 years) before the rate starts adjusting annually. 2. Hybrid ARM: The hybrid ARM combines the benefits of both fixed and adjustable interest rates. It begins with an initial fixed-rate period, typically lasting 3, 5, 7, or 10 years, followed by adjustable rate adjustments afterward. 3. Option ARM: This type of NY ARR offers borrowers various payment options each month, including a minimum payment (usually less than the interest-only payment), an interest-only payment, or a fully amortizing payment. However, it is crucial to thoroughly understand the terms and potential risks associated with this type of loan. 4. Interest-only ARM: With an interest-only ARM, borrowers have the option to pay only the interest accruing on the loan for a specific period, typically ranging from 3 to 10 years. After this initial period, principal payments are added, increasing the monthly payment. 5. Cash-out refinance ARM: This NY ARR option allows borrowers to refinance their current mortgage and receive cash from the equity in their home while also benefiting from an adjustable interest rate. Overall, the New York Adjustable Rate Rider — Variable Rate Note provides borrowers with flexibility in their mortgage payments, potentially lower initial interest rates, and the ability to adjust to changing market conditions. However, it is important for borrowers to carefully review the terms, risks, and potential future payment adjustments associated with each specific type of NY ARR before making an informed decision.

New York Adjustable Rate Rider - Variable Rate Note

Description

How to fill out New York Adjustable Rate Rider - Variable Rate Note?

Are you presently in the situation where you require documents for sometimes enterprise or personal reasons just about every day time? There are plenty of legitimate papers themes available online, but finding types you can rely isn`t effortless. US Legal Forms offers a huge number of form themes, like the New York Adjustable Rate Rider - Variable Rate Note, that happen to be written to fulfill state and federal needs.

If you are presently informed about US Legal Forms web site and get a free account, simply log in. Next, you are able to download the New York Adjustable Rate Rider - Variable Rate Note format.

If you do not provide an accounts and need to begin using US Legal Forms, abide by these steps:

- Find the form you need and make sure it is for your right city/region.

- Utilize the Preview option to examine the form.

- Look at the outline to ensure that you have selected the proper form.

- In the event the form isn`t what you are trying to find, use the Search industry to get the form that suits you and needs.

- If you discover the right form, click on Purchase now.

- Pick the pricing prepare you want, complete the necessary details to produce your account, and pay for an order utilizing your PayPal or bank card.

- Choose a hassle-free file file format and download your copy.

Find every one of the papers themes you possess purchased in the My Forms food selection. You may get a more copy of New York Adjustable Rate Rider - Variable Rate Note whenever, if needed. Just click on the required form to download or produce the papers format.

Use US Legal Forms, the most substantial variety of legitimate varieties, to save lots of some time and prevent blunders. The service offers appropriately made legitimate papers themes that can be used for a variety of reasons. Produce a free account on US Legal Forms and initiate producing your lifestyle easier.