Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

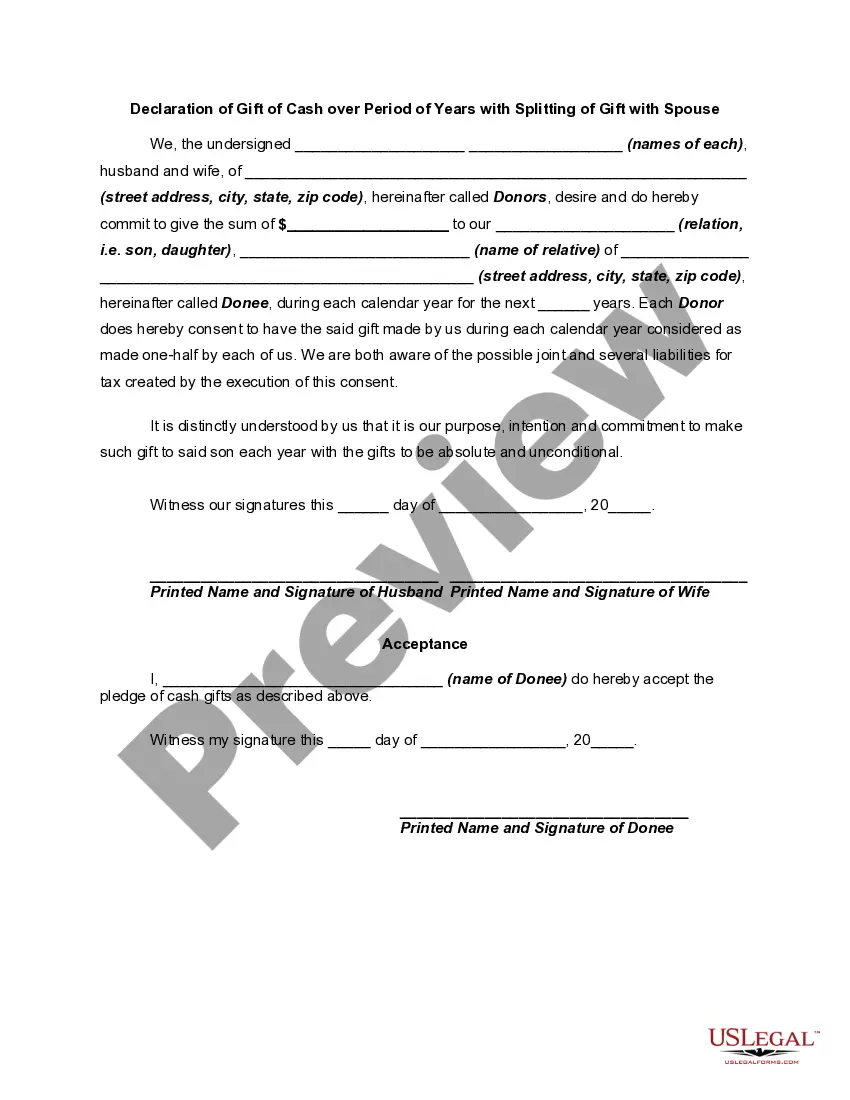

The New York Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse is a legal document in the state of New York that allows individuals to gift a certain amount of cash to another person or entity over a specific period of time, while also involving their spouse in the gift splitting process. This declaration follows the guidelines set by the Internal Revenue Service (IRS) and ensures that the gift is made in a lawful and organized manner. When creating a New York Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, it is important to consider the different types that exist, each serving a specific purpose. Some of these types include: 1. Annual Gift: This type of gift declaration involves the gifting of a specific amount of cash each year for a set period of time. The total amount of the gift is divided equally among the years, allowing individuals to take advantage of the annual gift tax exclusion limit. 2. Charitable Giving: If the gift is intended for a charitable organization or foundation, the New York Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse can be tailored to reflect this purpose. It ensures that the donations are made within the legal framework and that both spouses are actively involved in the process. 3. Educational Funding: This type of declaration is commonly used for gifting cash over a period of years to fund a loved one's education. By splitting the gift with a spouse, both individuals can contribute equally and take advantage of any applicable tax benefits. 4. Estate Planning: The declaration can also be used as part of an overall estate planning strategy. By gifting cash over a period of years, individuals can gradually reduce the size of their estate, potentially resulting in fewer estate taxes in the long run. 5. Family Gifting: This type of declaration allows for the gifting of cash to family members over a specified period. By splitting the gift with a spouse, both individuals can contribute to the financial well-being of their loved ones while minimizing any potential tax implications. When preparing a New York Declaration of Gift of Cash over Period of Years with Splitting of Gift with Spouse, it is crucial to consult with a qualified attorney or financial advisor who specializes in estate planning and gift tax matters. They will ensure that all the legal requirements are met and help individuals navigate through the complexities of the declaration while optimizing the tax benefits.