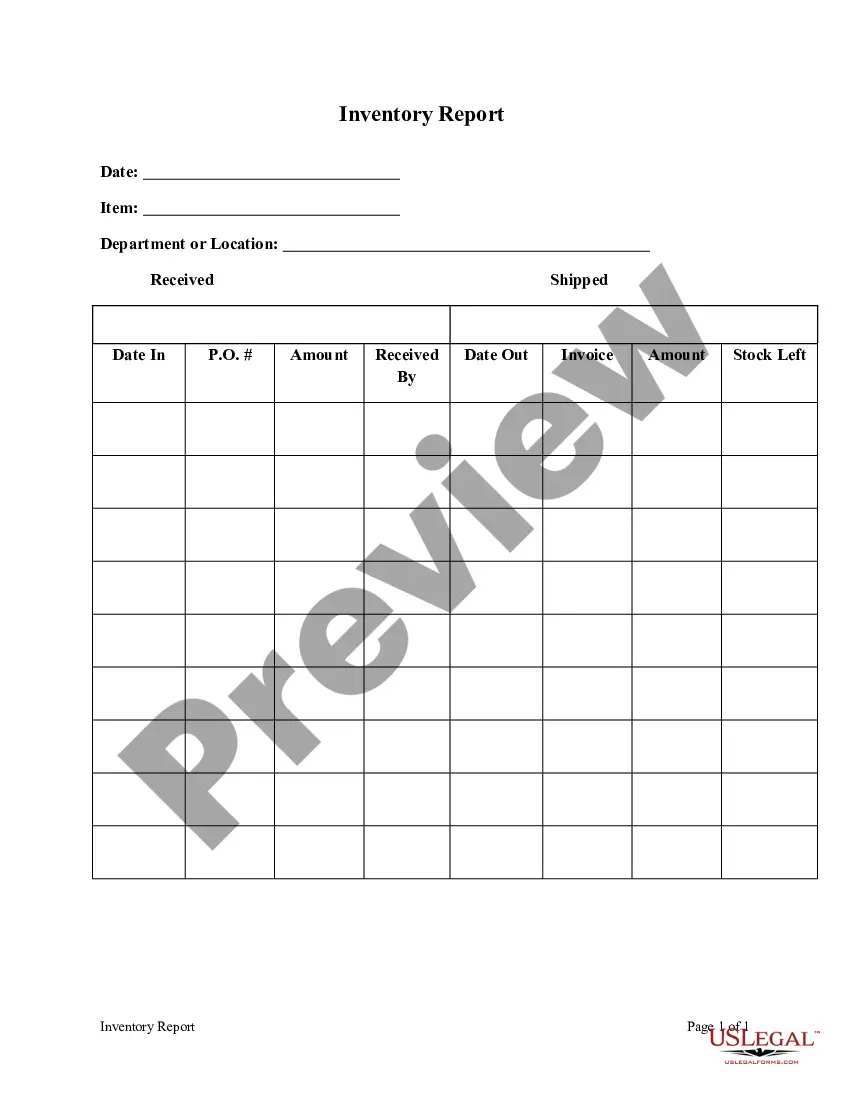

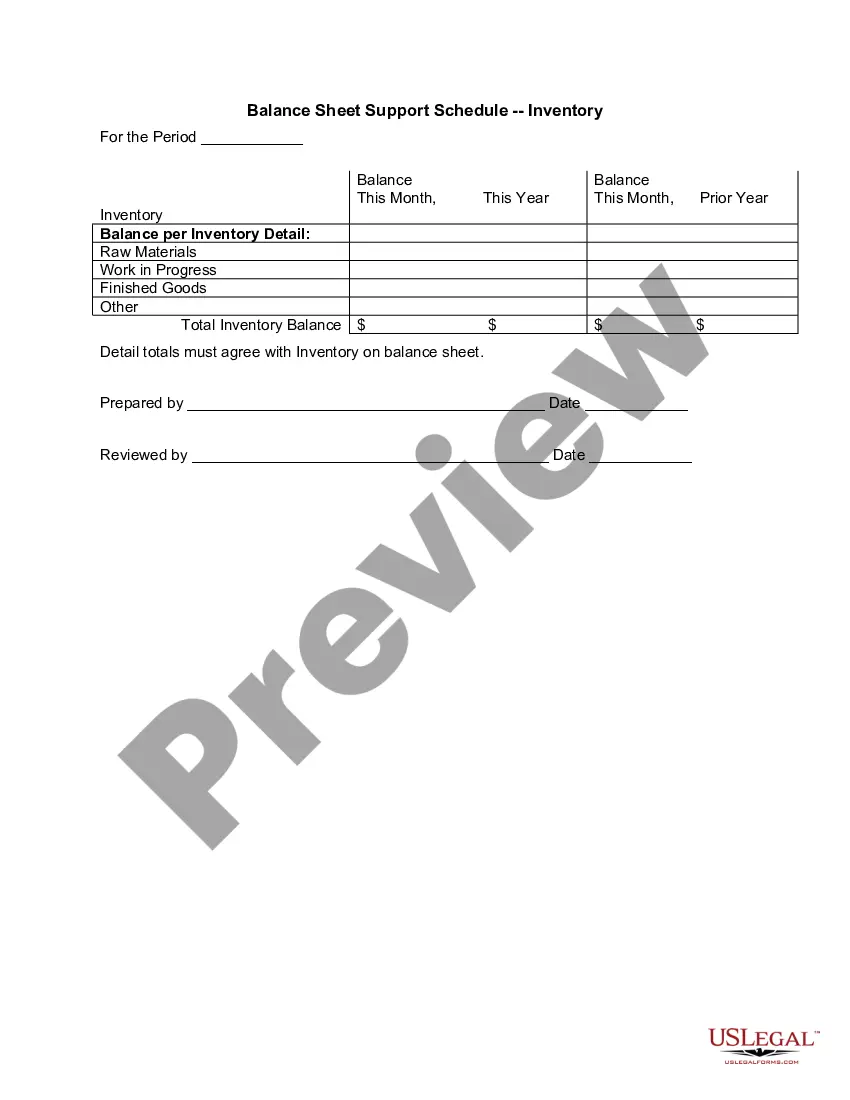

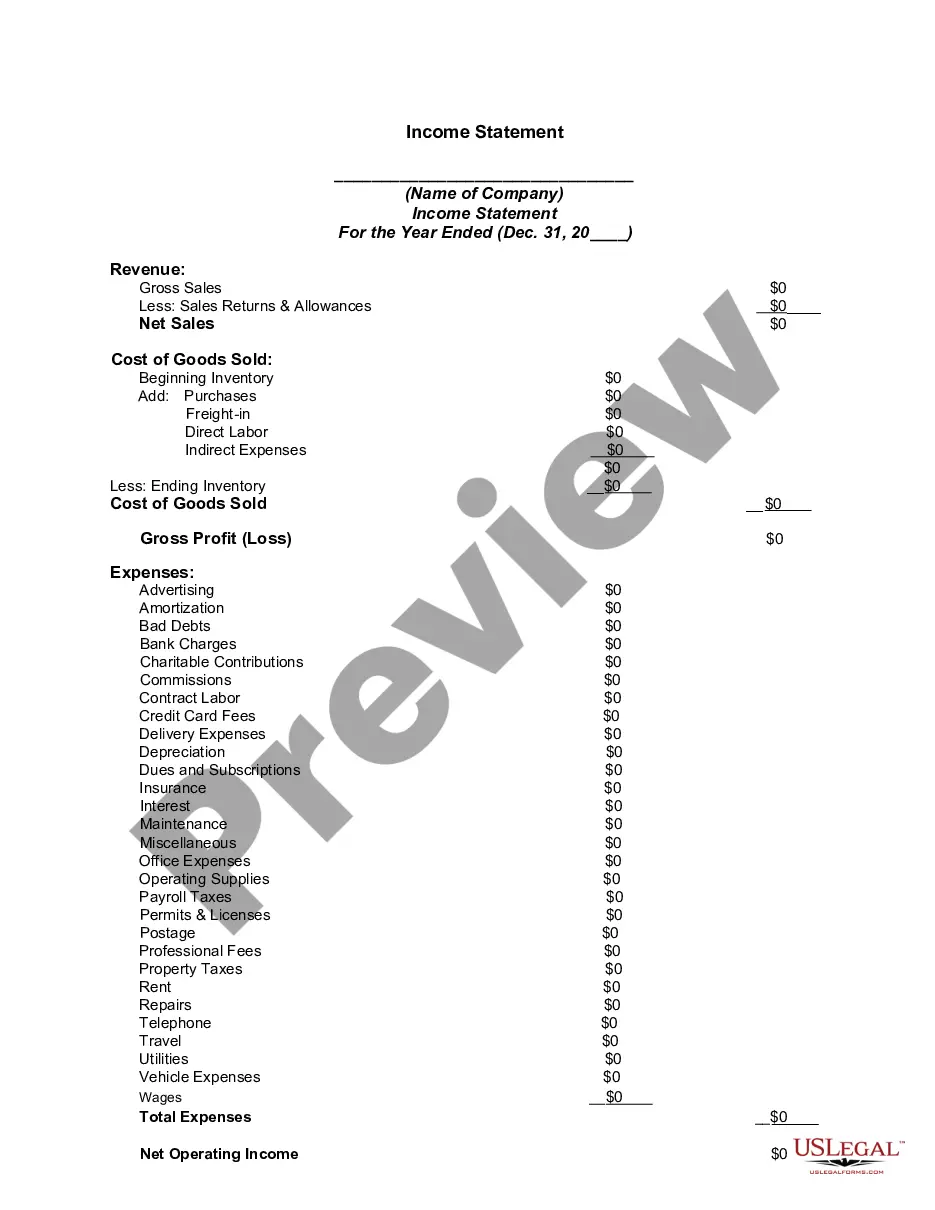

New York Summary of Account for Inventory of Business

Description

How to fill out Summary Of Account For Inventory Of Business?

Choosing the right authorized record web template could be a battle. Naturally, there are plenty of layouts available on the net, but how do you discover the authorized develop you require? Make use of the US Legal Forms internet site. The service gives a huge number of layouts, for example the New York Summary of Account for Inventory of Business, which can be used for enterprise and private needs. Every one of the varieties are checked by professionals and meet federal and state needs.

When you are already listed, log in to your accounts and click on the Download key to get the New York Summary of Account for Inventory of Business. Utilize your accounts to search with the authorized varieties you may have ordered in the past. Visit the My Forms tab of the accounts and have one more version of your record you require.

When you are a brand new user of US Legal Forms, allow me to share basic guidelines for you to stick to:

- Initial, make sure you have selected the correct develop for your metropolis/area. It is possible to look over the form using the Preview key and browse the form information to ensure it is the right one for you.

- In the event the develop does not meet your expectations, utilize the Seach industry to discover the appropriate develop.

- Once you are sure that the form is acceptable, click on the Acquire now key to get the develop.

- Pick the prices strategy you desire and enter in the needed information. Build your accounts and pay money for your order utilizing your PayPal accounts or bank card.

- Select the data file formatting and down load the authorized record web template to your gadget.

- Total, revise and print out and sign the attained New York Summary of Account for Inventory of Business.

US Legal Forms may be the most significant local library of authorized varieties that you can find different record layouts. Make use of the service to down load expertly-manufactured paperwork that stick to condition needs.

Form popularity

FAQ

You begin by calculating the cost-to-retail ratio, which is the cost of goods available for sale divided by their retail value. Multiply this ratio by the difference between the retail value of goods available for sale and total sales for the period. The result is an estimate of the cost of ending inventory.

To clearly reflect income, businesses must take inventories at the beginning and end of each tax year in which the production, purchase or sale of merchandise is an income-producing factor.

Do I need to report inventory? Yes. Inventory tax is a ?taxpayer active? tax. That the taxpayer (business owner) must calculate it.

How do I value my inventory for tax purposes? Your inventory should be valued at your purchase cost. Items that cannot be sold or are "worthless" can be taken out of inventory, and the loss is reflected as a higher cost of goods sold on your tax return. (You have the cost of the item, but no revenue for the sale).

Writing off inventory that's damaged, stolen or unsellable can cut your tax bill. Federal tax law allows you to write off items you lose to theft or disaster, and there are steps you can take to claim a tax write-off for inventory you can't seem to sell.

Generally, if you produce, purchase, or sell merchandise in your business, you must keep an inventory and use the accrual method for purchases and sales of merchandise.

Do I need to report inventory? Yes. Inventory tax is a ?taxpayer active? tax. That the taxpayer (business owner) must calculate it.

A business is not required to use inventories if it meets a $25 million gross receipts test (adjusted annually for inflation).