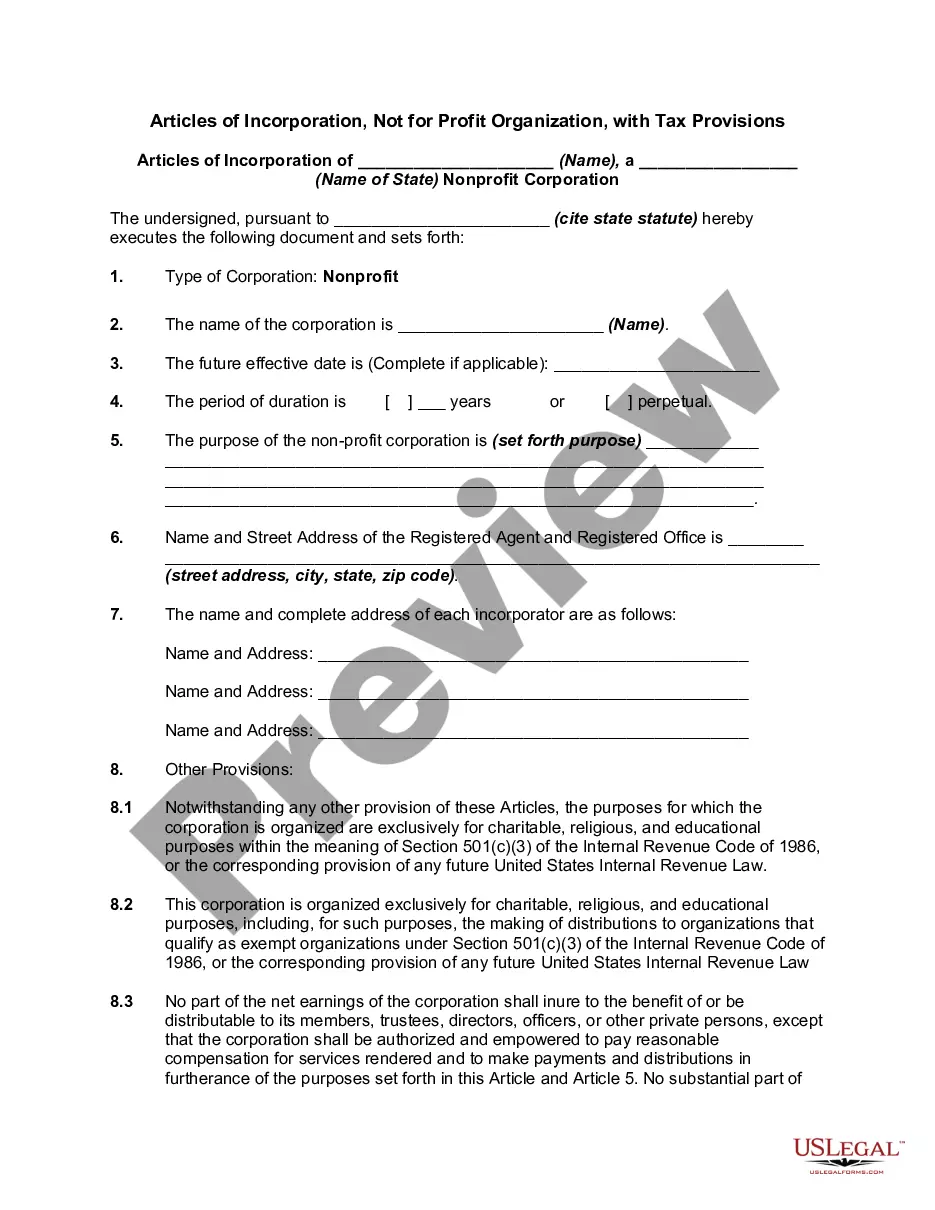

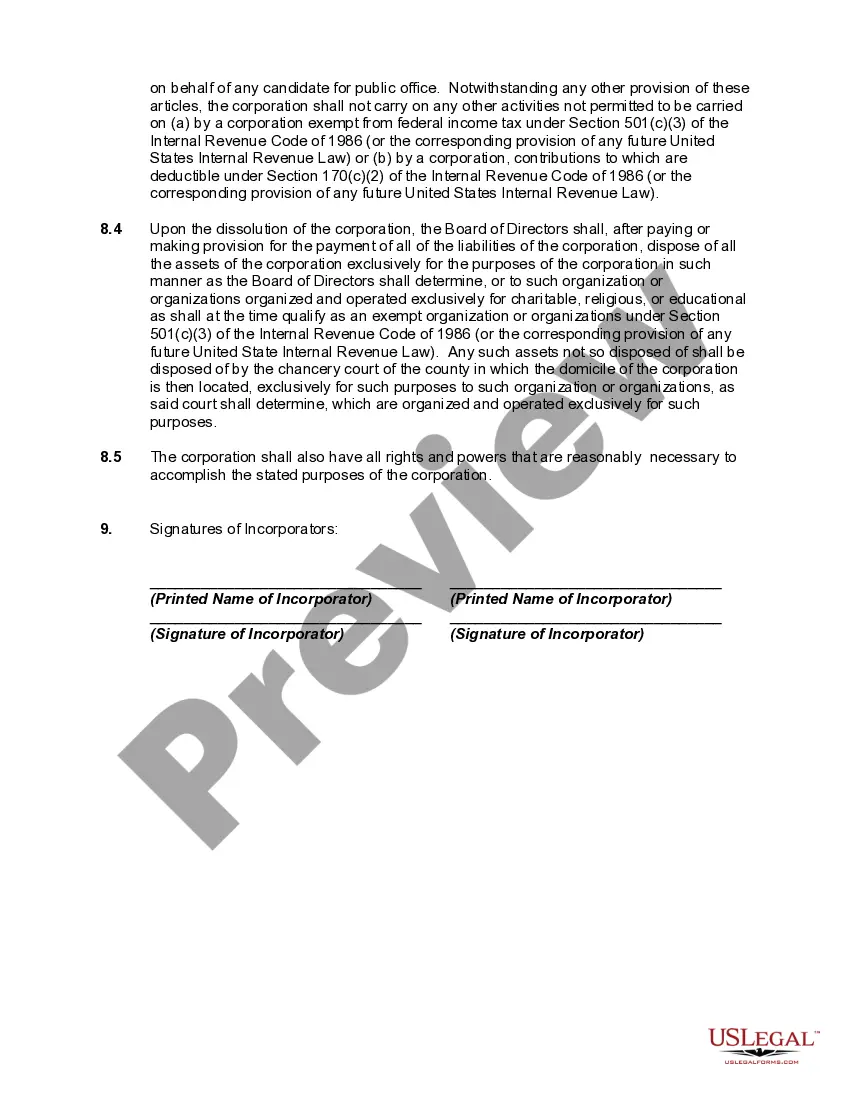

The proper form and necessary content of articles or certificates of incorporation for a nonprofit corporation depend largely on the requirements of the state nonprofit corporation act in the state of incorporation. Typically nonprofit corporations have no capital stock and therefore have members, not stockholders. Because federal tax-exempt status will be sought for most nonprofit corporations, the articles or certificate of incorporation must be carefully drafted to include specific language designed to ensure qualification for tax-exempt status.

New York Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions In the state of New York, organizations seeking to establish themselves as not-for-profit entities must file Articles of Incorporation with the New York Department of State. These articles serve as legal documentation that formally create the organization and outline its structure and purpose. Additionally, if the organization wishes to obtain tax-exempt status, specific tax provisions must be included in the Articles of Incorporation. The following keywords provide a comprehensive overview of New York Articles of Incorporation for Not-for-Profit Organizations with Tax Provisions: 1. Incorporation: The process of forming a legal entity that separates the organization from its founders and members, establishing it as a separate legal entity. Incorporation provides liability protection to its members, directors, and officers. 2. Not-for-Profit Organization: Refers to an entity established for purposes other than generating profits for individuals or shareholders. Not-for-profit organizations aim to serve the public interest, such as charities, religious organizations, social clubs, or educational institutions. 3. Tax Provisions: These provisions refer to the specific requirements and provisions that need to be included in the Articles of Incorporation to obtain tax-exempt status. This status enables the organization to be exempted from federal and state income taxes, allowing for the solicitation of tax-deductible donations. 4. Tax-Exempt Status: This status refers to the legal recognition given to not-for-profit organizations by the Internal Revenue Service (IRS) and state tax authorities, exempting them from certain tax obligations. This designation is crucial for organizations that heavily rely on donations and grants. Different types of New York Articles of Incorporation for Not-for-Profit Organizations may include the following variations regarding tax provisions: 1. 501(c)(3) Organizations: These refer to organizations that seek tax exemption under section 501(c)(3) of the Internal Revenue Code. It includes entities operating exclusively for religious, charitable, scientific, literary, or educational purposes. 2. 501(c)(4) Organizations: These organizations seek tax exemption under section 501(c)(4) of the Internal Revenue Code and are typically social welfare organizations. They engage in activities aimed at promoting the common good and general welfare of the community. 3. 501(c)(6) Organizations: Organizations aspiring for tax exemption under section 501(c)(6) of the Internal Revenue Code are business leagues, professional associations, or chambers of commerce. They primarily focus on advancing the interests and improving business conditions of a particular industry. 4. 501(c)(7) Organizations: These organizations seek tax exemption under section 501(c)(7) of the Internal Revenue Code and are social clubs primarily dedicated to recreation, pleasure, or other nonprofitable purposes. To ensure compliance, it is essential to consult legal counsel or tax professionals while drafting the Articles of Incorporation for a not-for-profit organization in New York. Properly incorporating and including the tax provisions relevant to the organization's mission and activities will enhance its chances of obtaining tax-exempt status and successfully operating for a public cause.