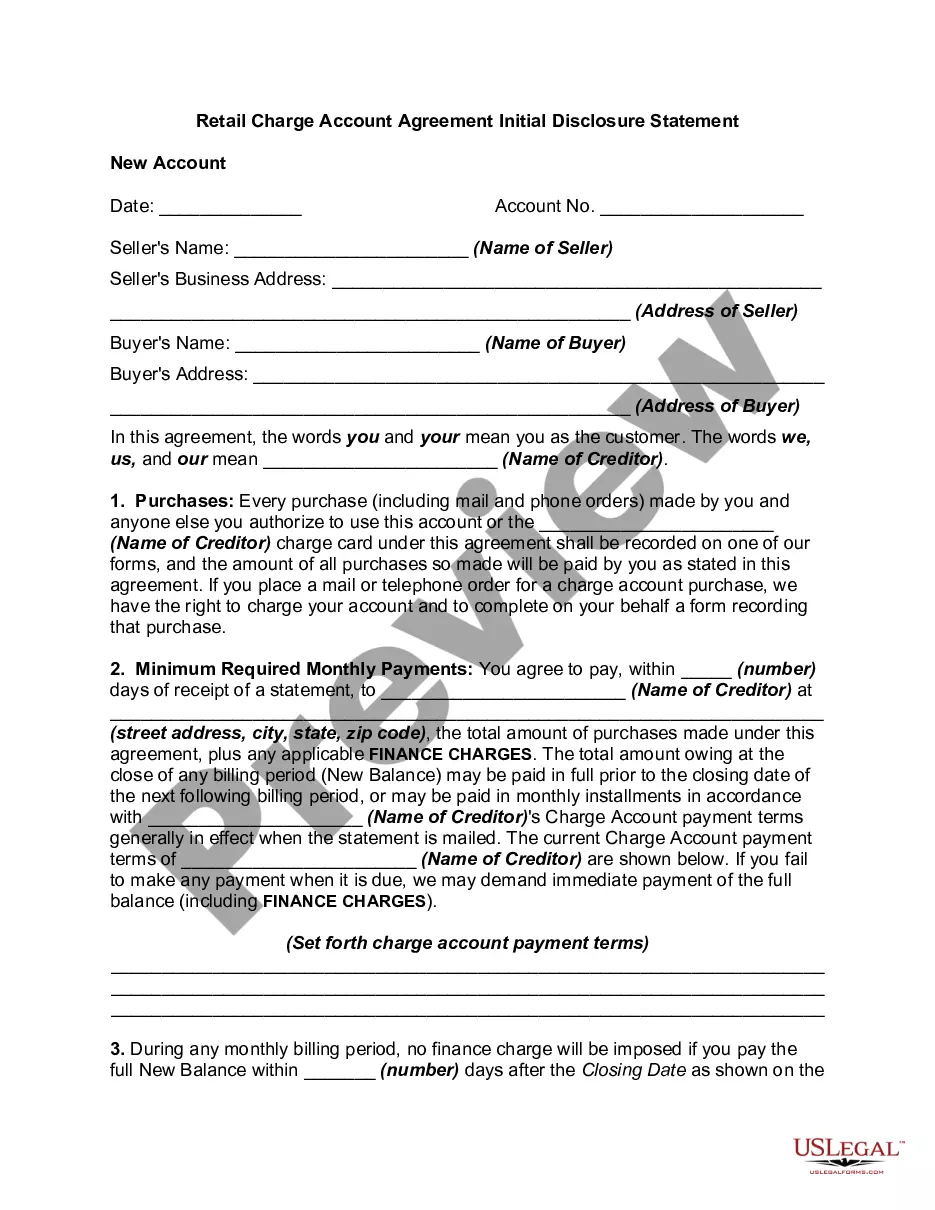

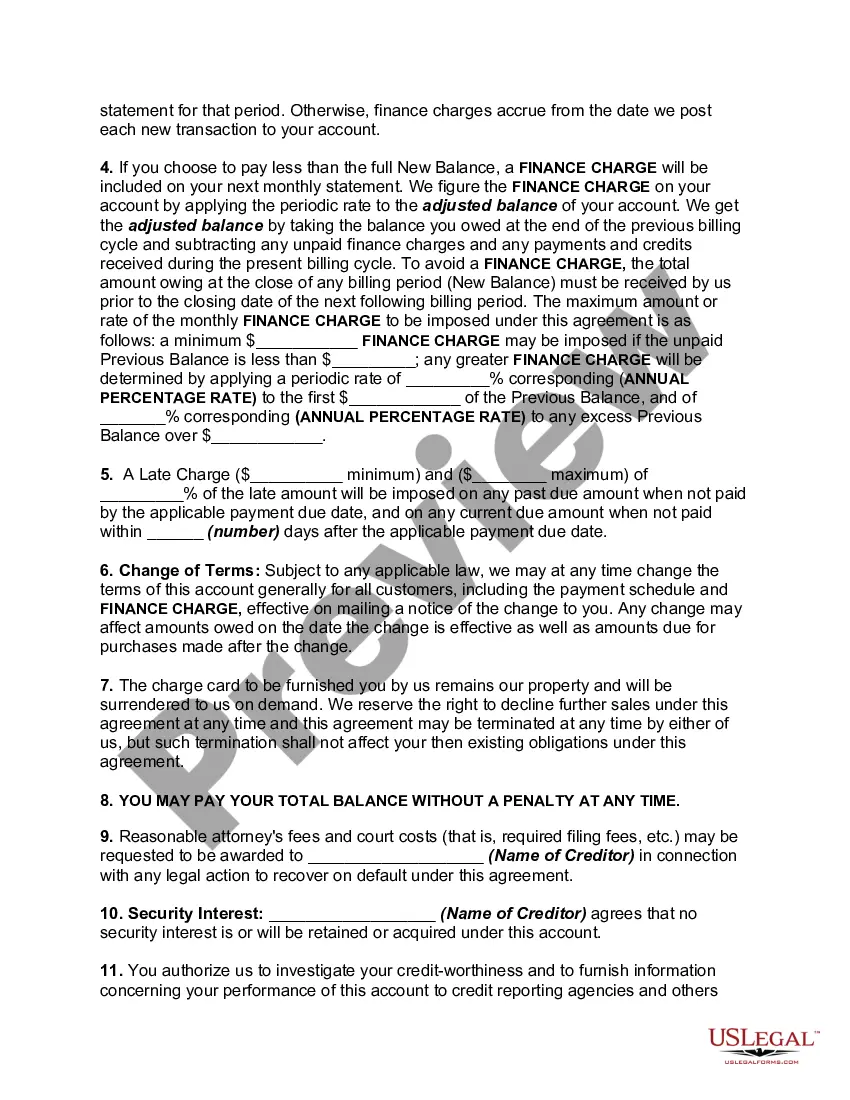

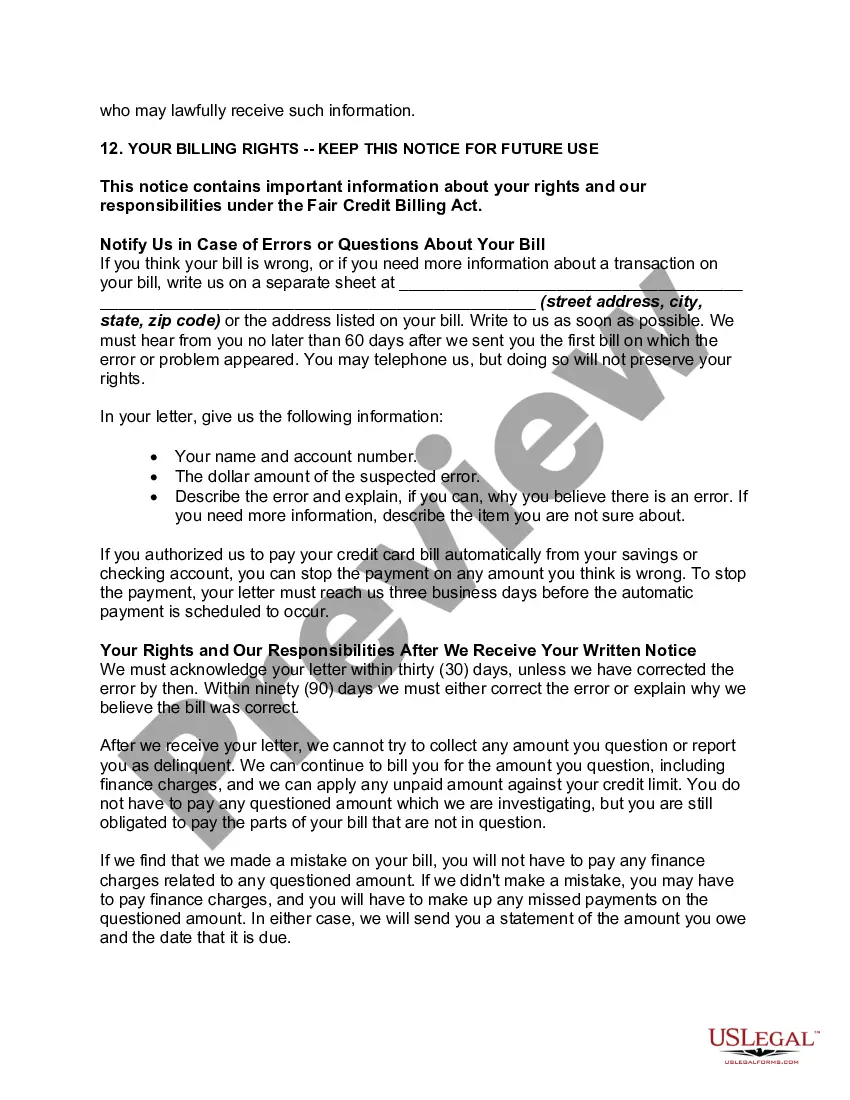

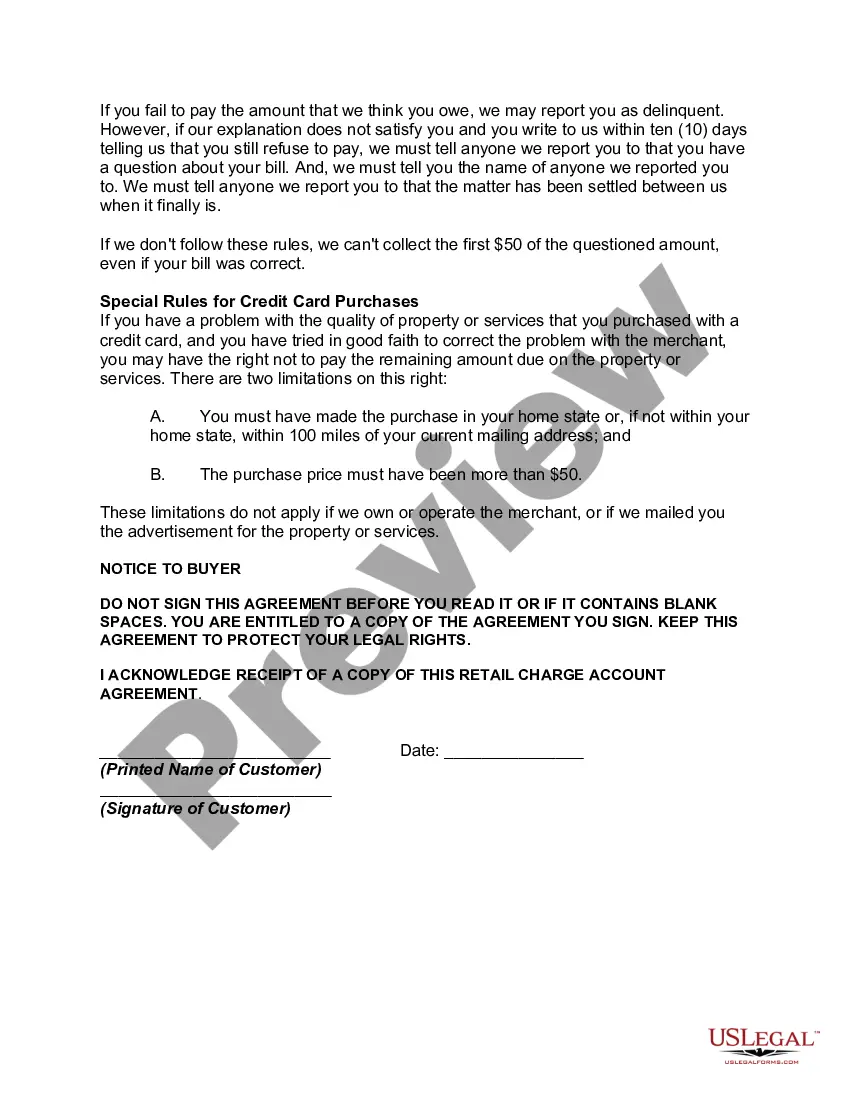

The New York Retail Charge Account Agreement Initial Disclosure Statement is a comprehensive document that outlines important terms and conditions involved in establishing a retail charge account in the state of New York. By providing this disclosure statement, retailers ensure transparency and clarity for their customers, allowing them to fully understand the obligations and rights associated with their charge account. Key elements covered in the New York Retail Charge Account Agreement Initial Disclosure Statement include: 1. Account Opening: The document specifies the process and requirements for opening a retail charge account with the merchant. This includes providing personal and contact information, as well as any necessary identification documents. 2. Account Usage: The disclosure statement details how the charge account can be used, including guidelines on making purchases, returning merchandise, and obtaining credit. 3. Billing and Payments: This section outlines the billing cycles, due dates, and methods of payment accepted by the retailer. It also includes information about late payment fees, interest charges, and any penalties for defaulting on payments. 4. Credit Limits and Account Changes: The document explains how credit limits are determined and how they may be adjusted based on the customer's payment history and creditworthiness. It also describes the procedures for requesting changes to the account, such as increasing the credit limit or adding authorized users. 5. Account Statement: The disclosure statement specifies how and when the retailer provides account statements to the customer. It details the information included in these statements, such as transaction history, outstanding balances, and applicable charges. It's important to note that while the New York Retail Charge Account Agreement Initial Disclosure Statement establishes a uniform framework for charge accounts, there may be variations depending on the retailer or the type of account being offered. Some specific types of New York Retail Charge Account Agreement Initial Disclosure Statements that may exist include: 1. Store-specific Charge Account Agreement: Different retailers may have their own unique disclosure statements tailored to their specific policies and requirements. 2. General Retail Charge Account Agreement: This type of agreement applies to multiple retailers or a specific group of retailers, offering a standardized disclosure statement for customers. 3. Private Label Charge Account Agreement: Private label credit cards or charge accounts associated with specific brands or businesses would have their own tailored disclosure statement to reflect their particular terms and conditions. 4. Online Retail Charge Account Agreement: Retailers conducting business primarily through an online platform may have a separate disclosure statement addressing specific aspects of online account usage, such as account access, security measures, and online transaction processes. In conclusion, the New York Retail Charge Account Agreement Initial Disclosure Statement is an essential document that clearly explains the terms, rights, and responsibilities associated with opening and maintaining a retail charge account. Whether it is a store-specific, general, private-label, or online retail agreement, these disclosure statements are vital for ensuring transparency and fostering a fair and mutually beneficial relationship between retailers and their customers.

New York Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out New York Retail Charge Account Agreement Initial Disclosure Statement?

If you have to complete, obtain, or produce lawful record web templates, use US Legal Forms, the greatest assortment of lawful types, which can be found on-line. Take advantage of the site`s simple and convenient lookup to obtain the files you require. A variety of web templates for company and person uses are sorted by classes and suggests, or search phrases. Use US Legal Forms to obtain the New York Retail Charge Account Agreement Initial Disclosure Statement with a handful of click throughs.

In case you are currently a US Legal Forms buyer, log in in your profile and click on the Down load key to have the New York Retail Charge Account Agreement Initial Disclosure Statement. You may also accessibility types you previously acquired in the My Forms tab of your respective profile.

If you are using US Legal Forms the first time, follow the instructions below:

- Step 1. Ensure you have selected the form for the correct metropolis/land.

- Step 2. Take advantage of the Preview choice to examine the form`s information. Never neglect to learn the outline.

- Step 3. In case you are unsatisfied using the develop, take advantage of the Research area on top of the monitor to discover other versions in the lawful develop format.

- Step 4. Upon having found the form you require, select the Get now key. Select the costs prepare you like and put your accreditations to register on an profile.

- Step 5. Procedure the transaction. You should use your Мisa or Ьastercard or PayPal profile to accomplish the transaction.

- Step 6. Select the formatting in the lawful develop and obtain it in your system.

- Step 7. Full, edit and produce or indication the New York Retail Charge Account Agreement Initial Disclosure Statement.

Every single lawful record format you buy is your own eternally. You have acces to each and every develop you acquired within your acccount. Select the My Forms portion and pick a develop to produce or obtain once more.

Compete and obtain, and produce the New York Retail Charge Account Agreement Initial Disclosure Statement with US Legal Forms. There are many expert and state-certain types you can use for your personal company or person requires.