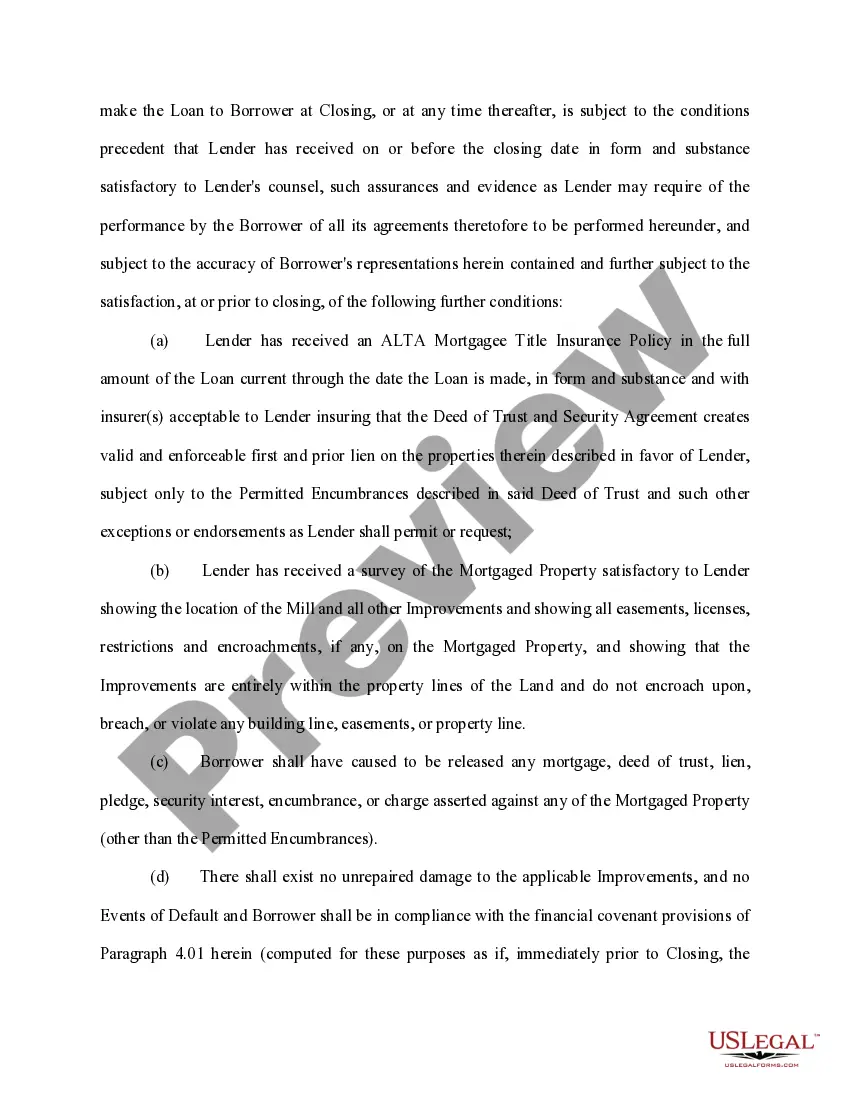

A New York Loan Agreement for Vehicle is a legally binding contract entered into by a lender and borrower for financing the purchase or lease of a vehicle in the state of New York. This agreement outlines the terms and conditions under which the borrower obtains a loan from the lender to finance the purchase of a vehicle, including the repayment terms, interest rates, and any collateral or security interest involved. In New York, there are different types of loan agreements for vehicles that cater to various financing needs and circumstances. Some common types include: 1. New Vehicle Loan Agreement: This type of agreement is used when a borrower seeks financing to purchase a brand-new vehicle. The terms and conditions in this agreement may differ from those for used vehicles due to factors like depreciation, loan-to-value ratios, or manufacturer warranties. 2. Used Vehicle Loan Agreement: When a borrower intends to finance the purchase of a pre-owned vehicle, a used vehicle loan agreement is employed. These agreements may have specific clauses to address the condition of the vehicle, mileage limitations, and valuation methods for determining the loan amount. 3. Lease Agreement: In certain cases, borrowers opt for vehicle leasing instead of outright purchasing. A lease agreement is used to document the terms of the lease, including monthly payments, lease period, mileage restrictions, and potential penalties for excess wear and tear. 4. Refinancing Agreement: Existing vehicle owners in New York may also enter into a loan agreement to refinance their current car loans. This agreement allows borrowers to change the terms of their original loan, such as interest rates, monthly payments, or loan duration, with the objective of achieving more favorable terms. Regardless of the specific type, a New York Loan Agreement for Vehicle will typically include essential details such as the names of the lender and borrower, vehicle information (make, model, VIN), loan amount, repayment schedule, interest rate, late payment fees, and any applicable warranties or guarantees. The agreement will also specify the consequences for defaulting on the loan, potential remedies for the lender, and the obligations of both parties throughout the duration of the loan. It is important to note that the content provided here is for informational purposes only and should not be considered legal advice. If you require assistance with a New York Loan Agreement for Vehicle, it is recommended to consult with a qualified attorney or legal professional specializing in vehicle financing.

New York Loan Agreement for Vehicle

Description

How to fill out New York Loan Agreement For Vehicle?

Are you in a place the place you need to have papers for possibly enterprise or personal uses just about every day? There are a variety of authorized record themes accessible on the Internet, but discovering ones you can depend on is not straightforward. US Legal Forms provides 1000s of type themes, like the New York Loan Agreement for Vehicle, that happen to be composed to fulfill state and federal specifications.

If you are already familiar with US Legal Forms web site and have an account, just log in. Next, it is possible to download the New York Loan Agreement for Vehicle design.

Unless you offer an bank account and need to begin to use US Legal Forms, abide by these steps:

- Get the type you want and make sure it is for the appropriate town/state.

- Make use of the Review key to check the form.

- Browse the explanation to actually have selected the right type.

- When the type is not what you`re searching for, take advantage of the Look for area to get the type that fits your needs and specifications.

- When you obtain the appropriate type, click on Purchase now.

- Choose the costs prepare you would like, submit the desired info to create your account, and pay money for the order using your PayPal or bank card.

- Select a convenient document formatting and download your version.

Get each of the record themes you have bought in the My Forms food selection. You may get a further version of New York Loan Agreement for Vehicle whenever, if necessary. Just go through the required type to download or print the record design.

Use US Legal Forms, one of the most substantial variety of authorized types, to save efforts and avoid errors. The support provides skillfully created authorized record themes that you can use for an array of uses. Make an account on US Legal Forms and commence making your way of life a little easier.