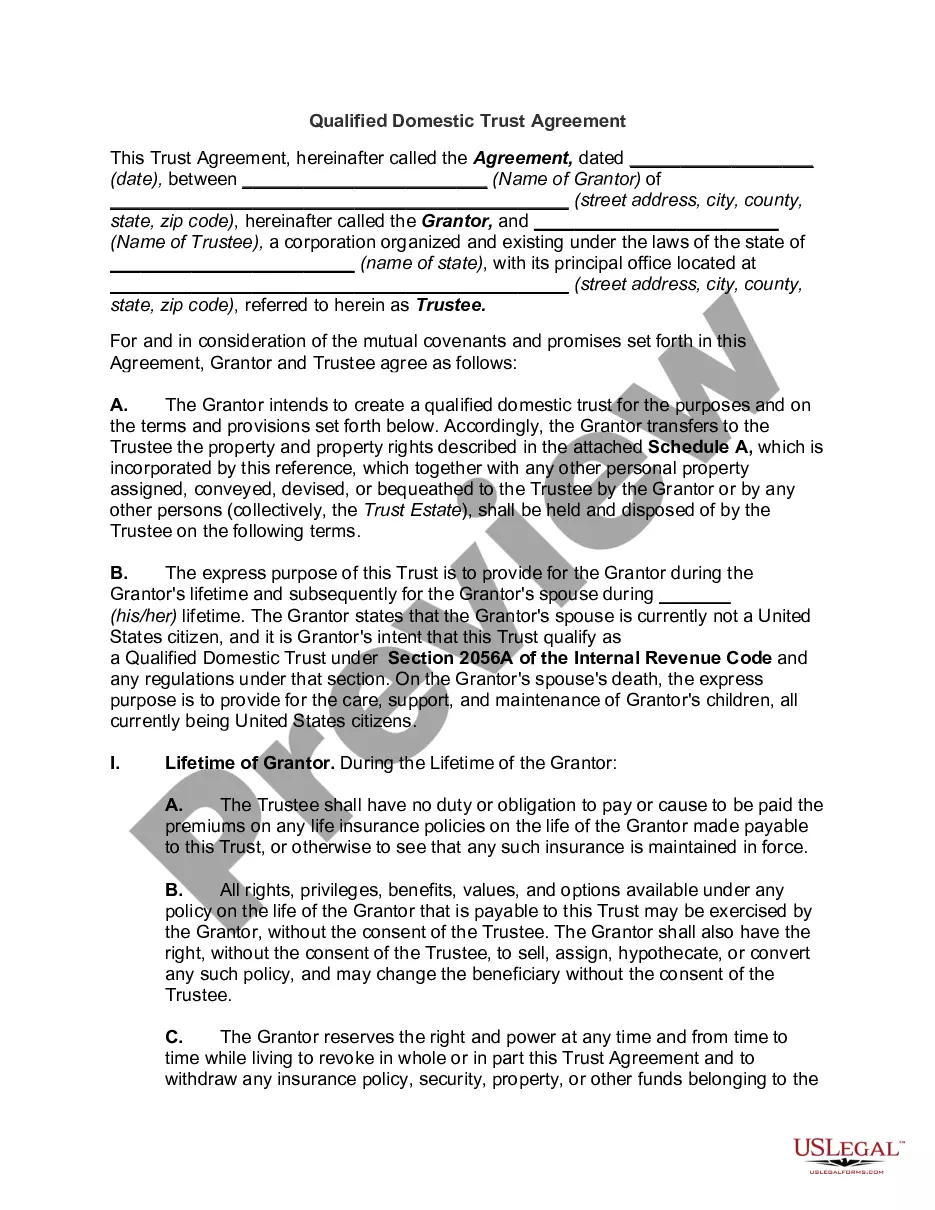

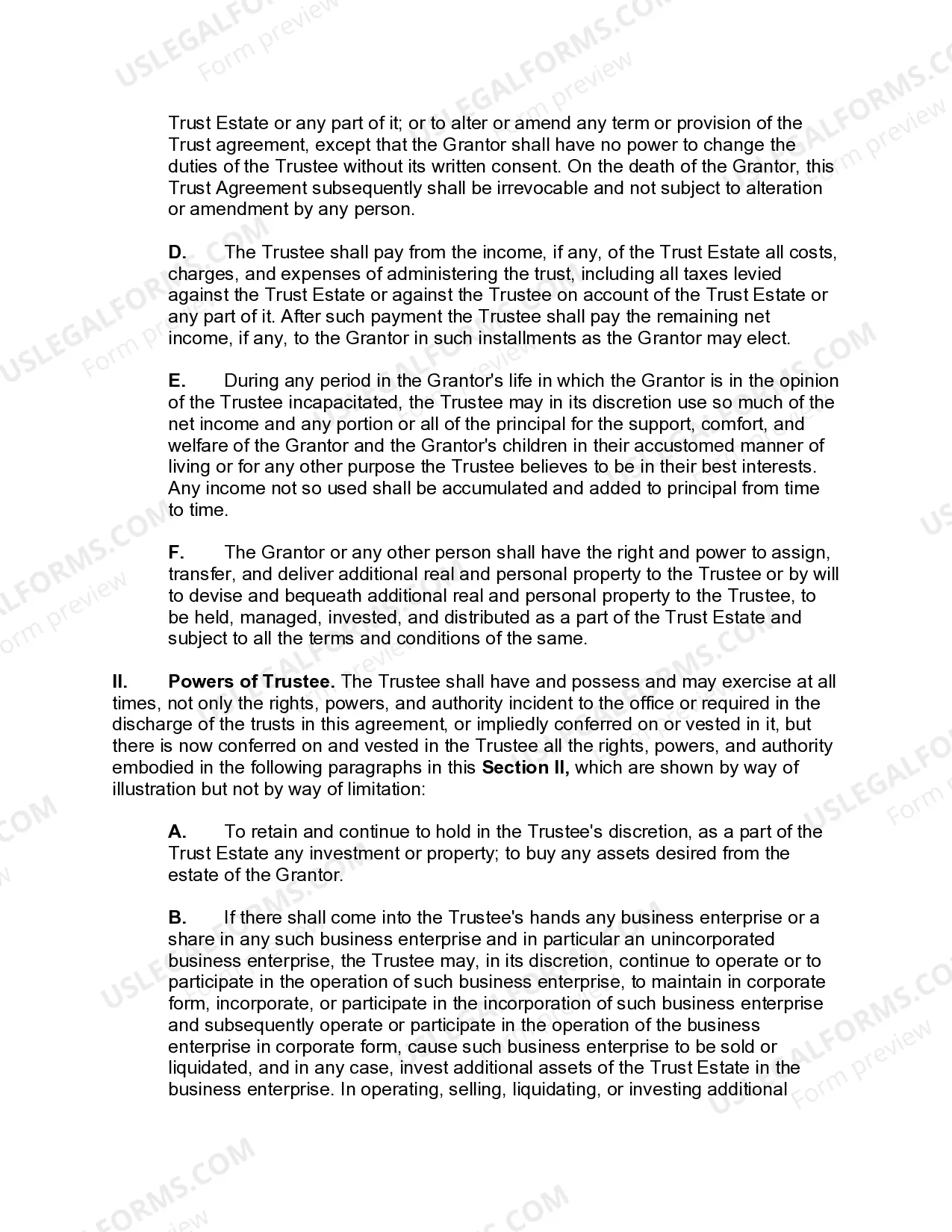

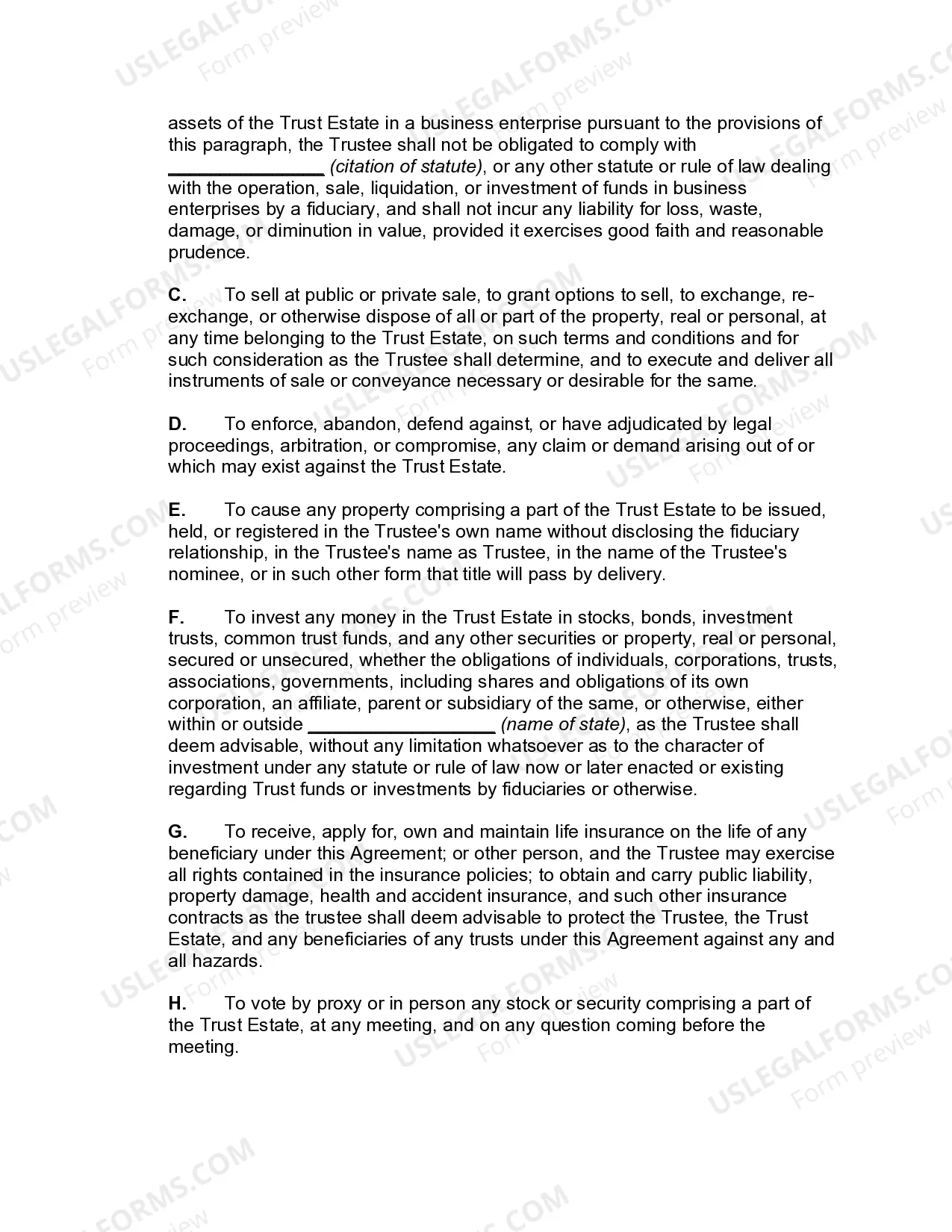

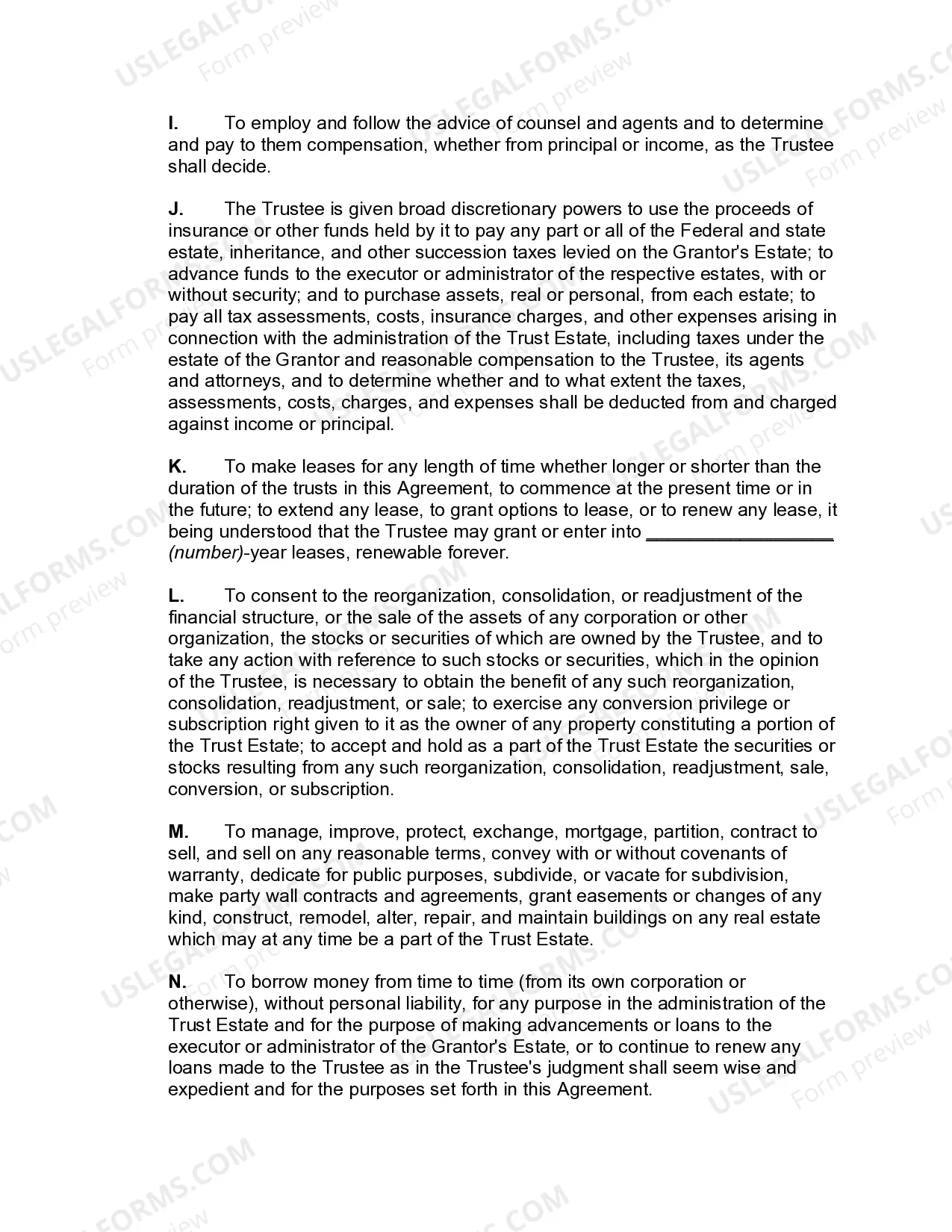

New York Qualified Domestic Trust Agreement (DOT) is a legal arrangement designed to provide estate tax benefits for non-U.S. citizen spouses who inherit property from a U.S. citizen spouse. This special trust allows the non-U.S. citizen spouse to postpone the payment of estate taxes until they receive distributions from the trust. The main purpose of a New York DOT Agreement is to prevent the immediate imposition of estate taxes upon the death of a U.S. citizen spouse. Generally, when a U.S. citizen passes away, their estate may be subject to estate taxes. However, if the surviving spouse is not a U.S. citizen, their inheritance may not qualify for the unlimited estate tax marital deduction. The DOT Agreement bridges this gap, making it possible for the non-U.S. citizen spouse to enjoy the marital deduction benefits. In New York, there are no specific types of DOT Agreements that differ from the general DOT rules. However, it is essential to note that DOT rules and requirements can vary across different states within the United States. Each state might have additional requirements or modifications to the federal DOT rules. To create a DOT in New York, certain conditions must be met. The trust must have at least one U.S. trustee who is responsible for managing the trust's assets, ensuring compliance with tax regulations, and making decisions regarding distributions. Additionally, the trustee must possess the authority to withhold estate taxes on distributions made to the non-U.S. citizen spouse. The DOT Agreement must stipulate that principal distributions made from the trust to the non-U.S. citizen spouse will be subject to estate taxes. Only the income generated by the trust assets is generally available for the non-U.S. citizen spouse's use without triggering immediate estate taxes. It is important to carefully consider the terms and conditions of a New York DOT Agreement to ensure that it complies with both federal and state tax laws. Seeking professional legal advice is highly recommended when creating a DOT to ensure all requirements are met and potential tax benefits are maximized. In conclusion, a New York Qualified Domestic Trust Agreement is a specific legal mechanism that facilitates the deferral of estate taxes for non-U.S. citizen spouses inheriting property from U.S. citizen spouses. While there are no specific types of New York DOT Agreements, it is crucial to understand the state and federal requirements and seek legal counsel to ensure compliance and maximize tax benefits.

New York Qualified Domestic Trust Agreement

Description

How to fill out New York Qualified Domestic Trust Agreement?

Finding the right lawful papers web template could be a battle. Naturally, there are a variety of themes available online, but how will you get the lawful kind you need? Take advantage of the US Legal Forms site. The assistance offers thousands of themes, like the New York Qualified Domestic Trust Agreement, which can be used for company and private needs. All the forms are checked by pros and meet up with state and federal needs.

If you are already listed, log in in your account and click the Down load option to have the New York Qualified Domestic Trust Agreement. Use your account to look from the lawful forms you possess acquired in the past. Check out the My Forms tab of the account and get one more version of the papers you need.

If you are a brand new consumer of US Legal Forms, allow me to share straightforward instructions that you can adhere to:

- Very first, make sure you have chosen the right kind for your town/county. You may look through the form making use of the Preview option and browse the form description to guarantee it is the right one for you.

- When the kind does not meet up with your needs, take advantage of the Seach industry to discover the proper kind.

- Once you are certain that the form is proper, select the Buy now option to have the kind.

- Choose the prices plan you desire and enter in the required information. Make your account and buy an order making use of your PayPal account or bank card.

- Opt for the document formatting and acquire the lawful papers web template in your system.

- Total, revise and printing and signal the acquired New York Qualified Domestic Trust Agreement.

US Legal Forms may be the most significant library of lawful forms in which you can discover numerous papers themes. Take advantage of the service to acquire appropriately-produced files that adhere to express needs.