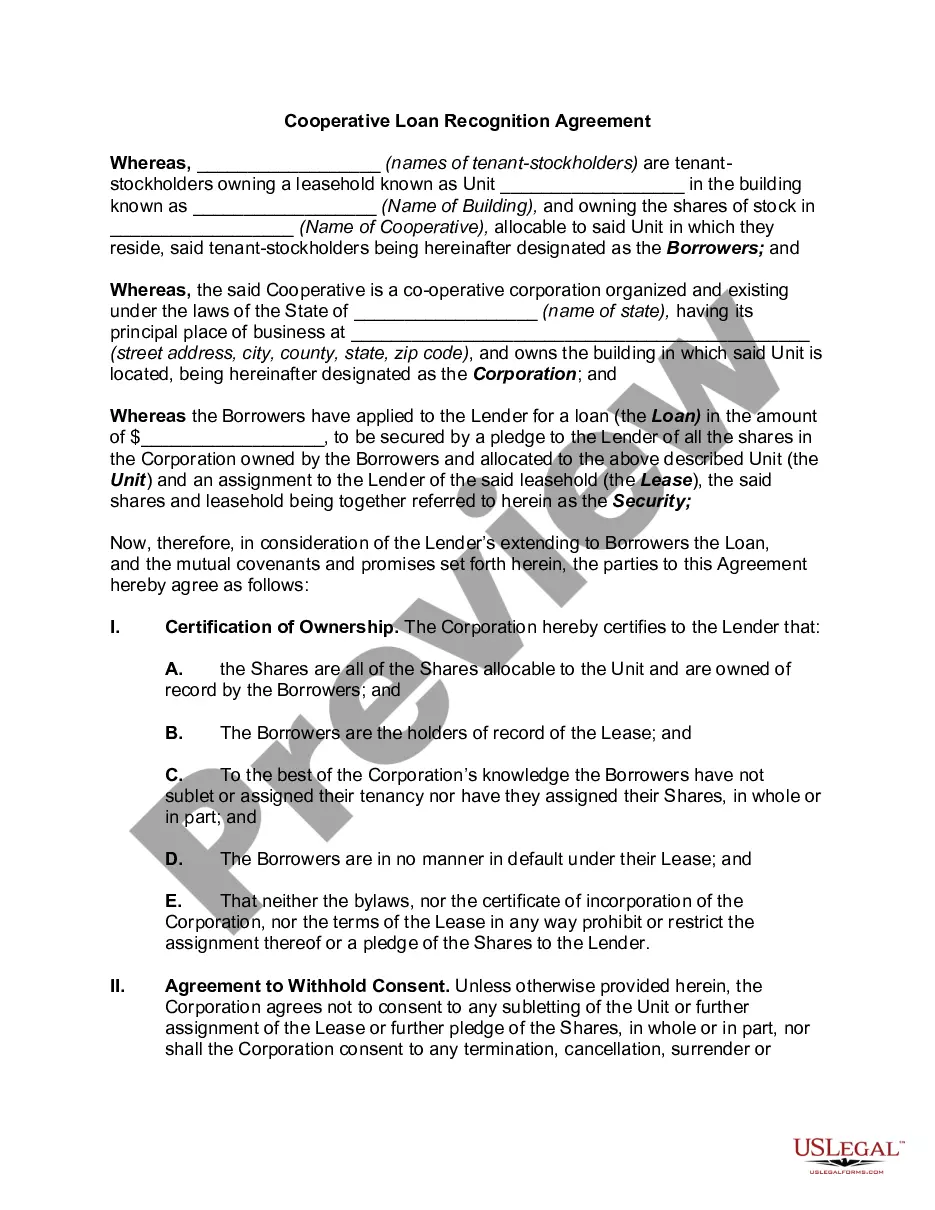

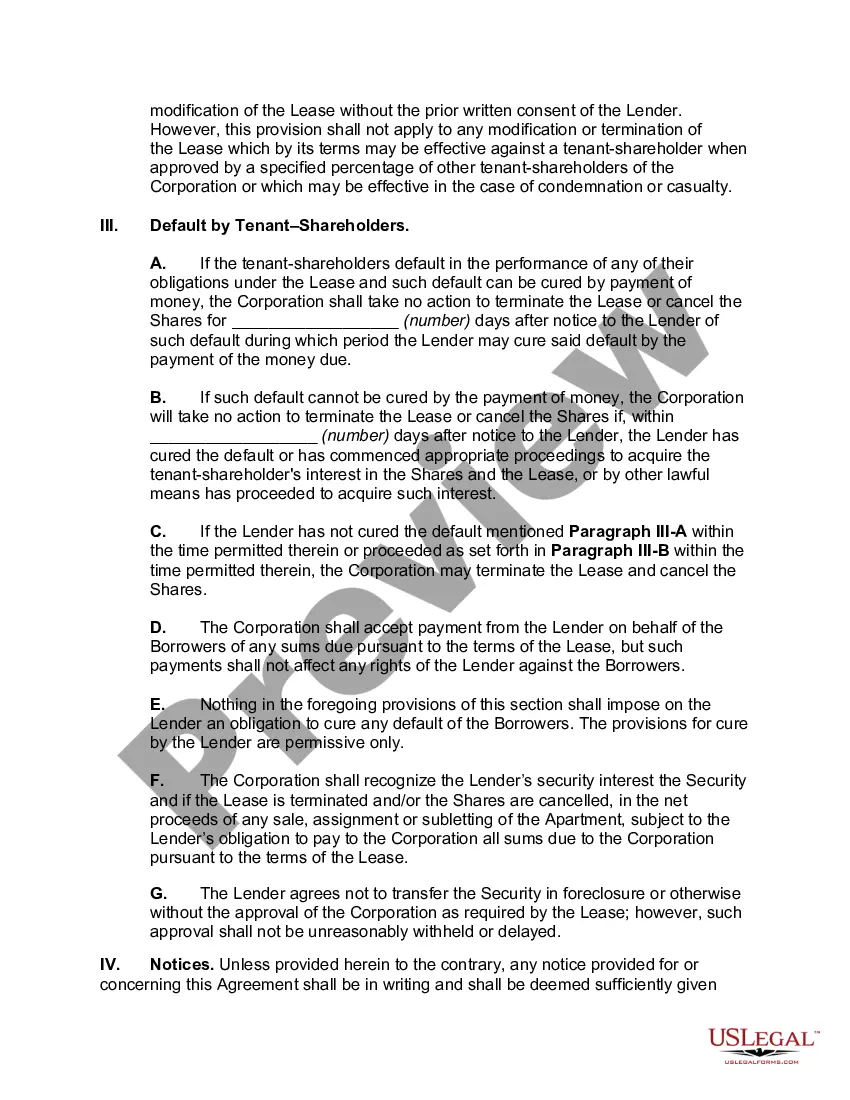

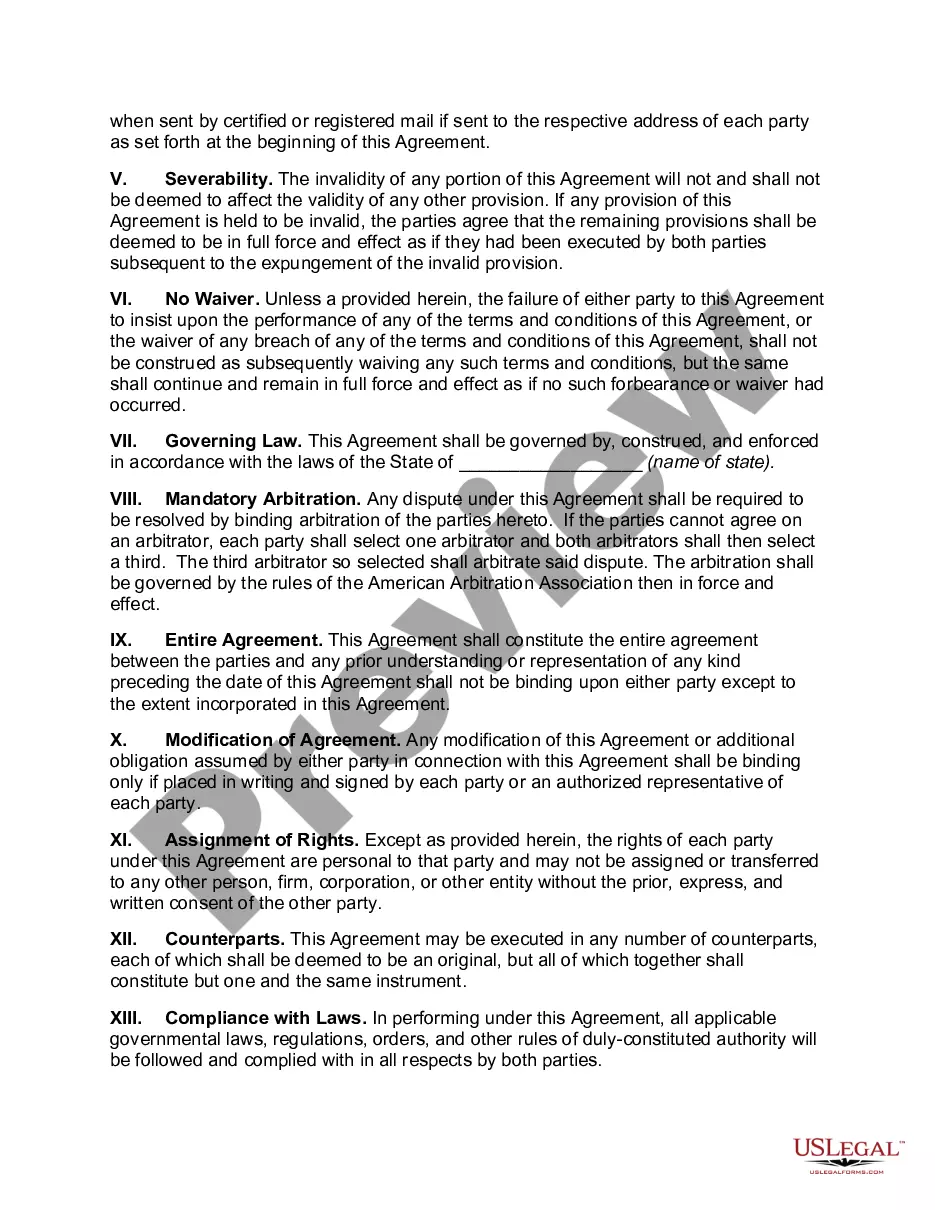

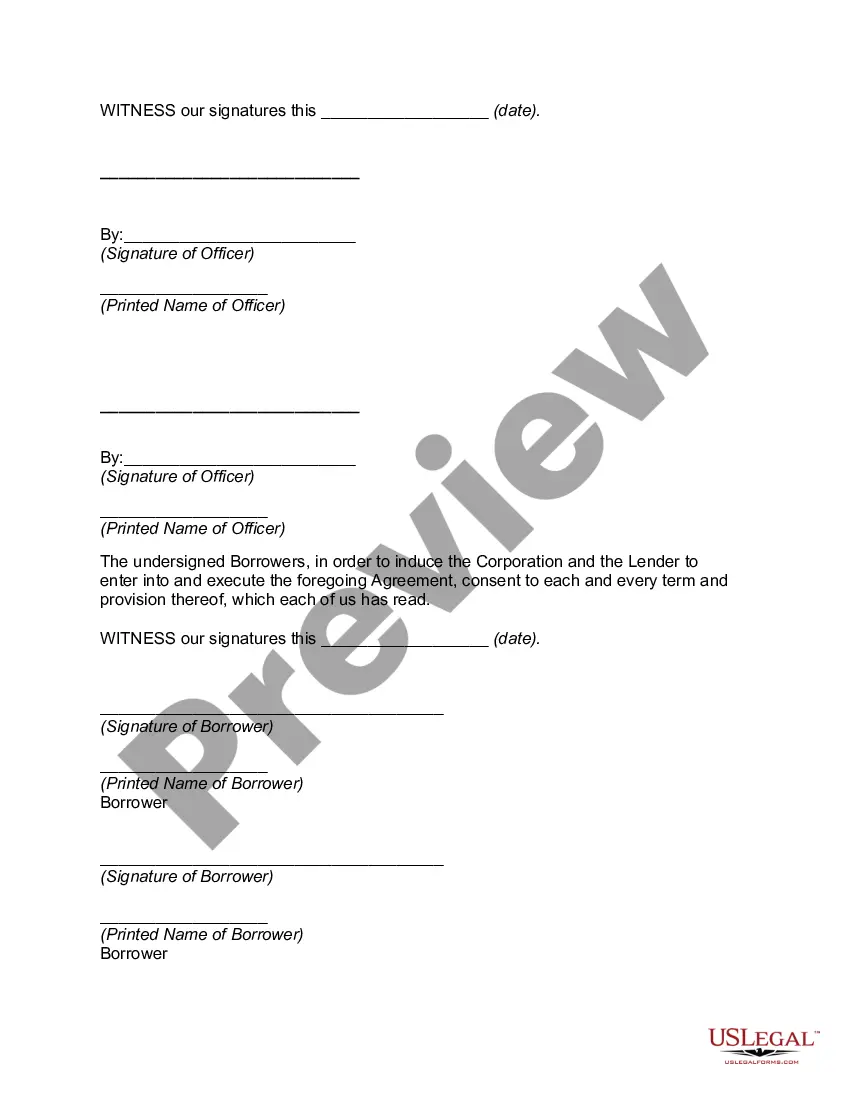

The New York Cooperative Loan Recognition Agreement is a legal document that establishes the terms and conditions between a cooperative corporation and a lender in the state of New York. This agreement solidifies the cooperative's obligations and responsibilities towards the lender in relation to a loan or a mortgage. In essence, the New York Cooperative Loan Recognition Agreement serves as a contractual arrangement that recognizes the existence and priority of the lender's lien against the cooperative's shares and the underlying proprietary lease. This agreement provides a framework for addressing various aspects of the loan, such as repayment, interest rates, and additional security measures. There are a few different types of New York Cooperative Loan Recognition Agreement, each designed to suit specific loan arrangements and circumstances. These agreements can include: 1. Term Loan Recognition Agreement: This type of agreement outlines the terms and conditions for a loan with a specified repayment period. It determines the loan amount, interest rate, and repayment schedule, offering a clear plan for the cooperative and lender to follow. 2. Construction Loan Recognition Agreement: When a cooperative corporation undertakes a construction project, this agreement comes into play. It defines the terms of a loan specifically designed for financing the construction or renovation of a cooperative building or property. 3. Lines of Credit Loan Recognition Agreement: This agreement establishes the terms and conditions for a revolving line of credit that a cooperative corporation can access as needed. It offers flexibility to borrow funds for various purposes, such as repairs, maintenance, or unforeseen expenses. 4. Refinance Loan Recognition Agreement: In the event a cooperative corporation decides to refinance its existing loan, this agreement governs the terms of the new loan. It details the loan amount, interest rate, repayment schedule, and any changes to the collateral or security measures. 5. Subordinated Loan Recognition Agreement: Sometimes, a lender may agree to provide secondary financing to a cooperative corporation. In such cases, this agreement outlines the subordination terms and conditions, specifying the priority of repayments between the primary and subordinated loans. Overall, the New York Cooperative Loan Recognition Agreement is a crucial legal document that provides clarity and protection for both the cooperative corporation and the lender. It ensures transparency, accountability, and a mutually beneficial relationship between the two parties, enabling efficient cooperation throughout the loan term.

New York Cooperative Loan Recognition Agreement

Description

How to fill out New York Cooperative Loan Recognition Agreement?

Have you been in a placement where you require papers for possibly organization or individual purposes virtually every day? There are tons of legal document themes available on the net, but locating types you can rely isn`t easy. US Legal Forms gives a large number of kind themes, just like the New York Cooperative Loan Recognition Agreement, that happen to be published to satisfy federal and state specifications.

If you are currently informed about US Legal Forms website and also have an account, simply log in. Next, it is possible to obtain the New York Cooperative Loan Recognition Agreement template.

If you do not provide an account and would like to start using US Legal Forms, follow these steps:

- Obtain the kind you will need and make sure it is to the proper town/area.

- Make use of the Review option to review the form.

- Read the description to actually have selected the appropriate kind.

- When the kind isn`t what you`re searching for, use the Look for discipline to get the kind that suits you and specifications.

- If you get the proper kind, simply click Buy now.

- Pick the pricing strategy you want, fill in the desired information to generate your money, and buy your order making use of your PayPal or charge card.

- Decide on a practical document file format and obtain your version.

Locate all of the document themes you have bought in the My Forms food selection. You can get a more version of New York Cooperative Loan Recognition Agreement any time, if required. Just click the needed kind to obtain or print the document template.

Use US Legal Forms, by far the most extensive assortment of legal varieties, to save time and prevent errors. The services gives appropriately created legal document themes which you can use for a selection of purposes. Create an account on US Legal Forms and start producing your daily life easier.