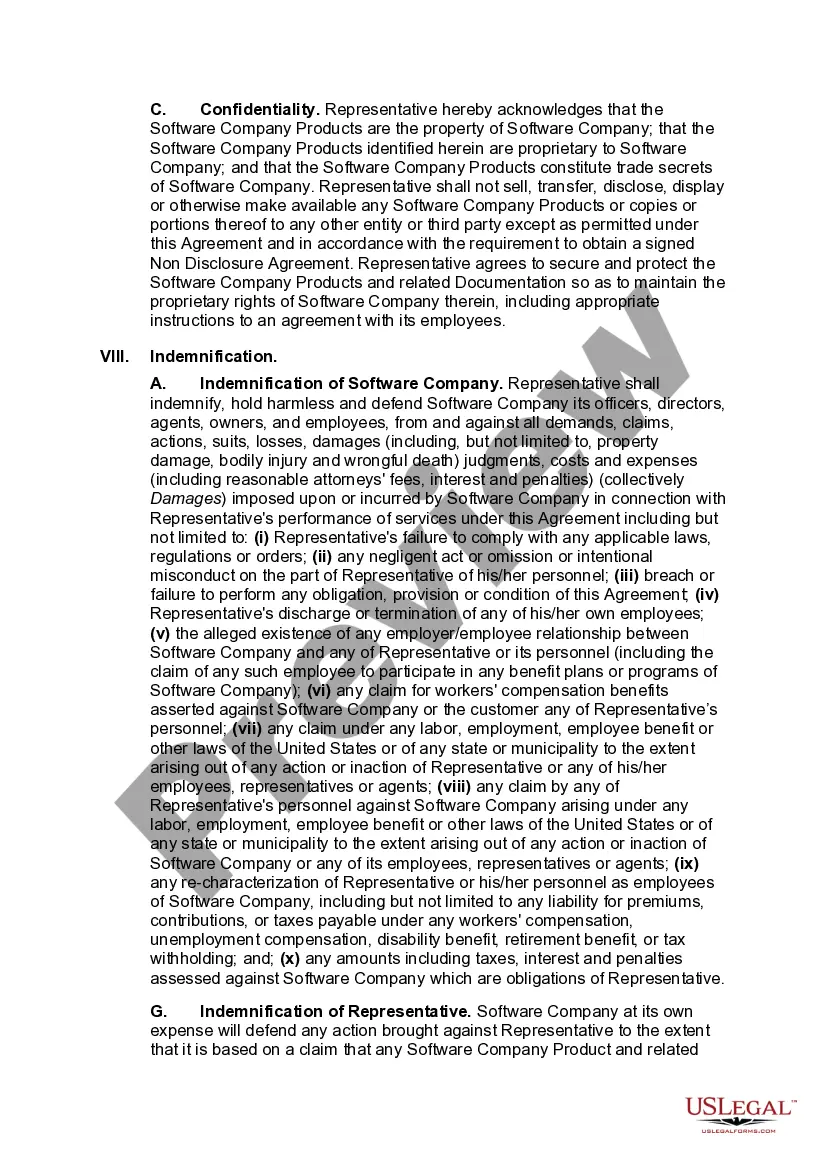

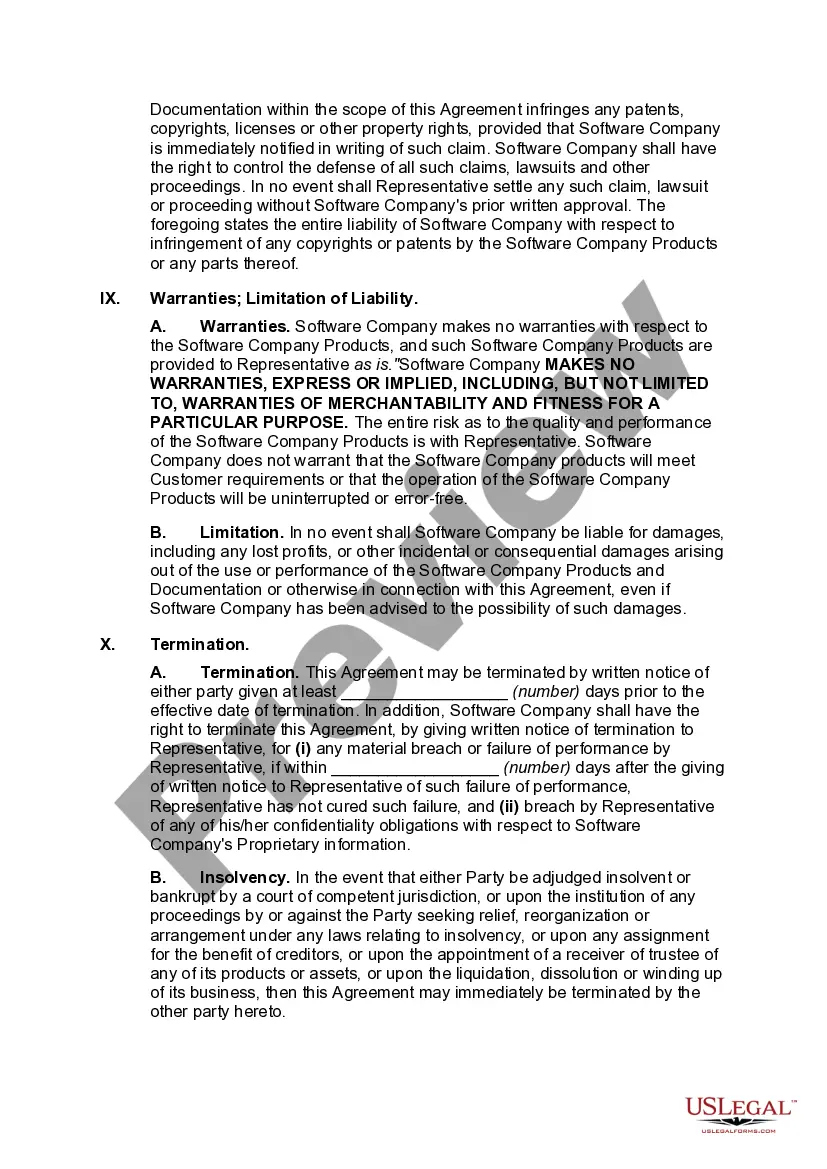

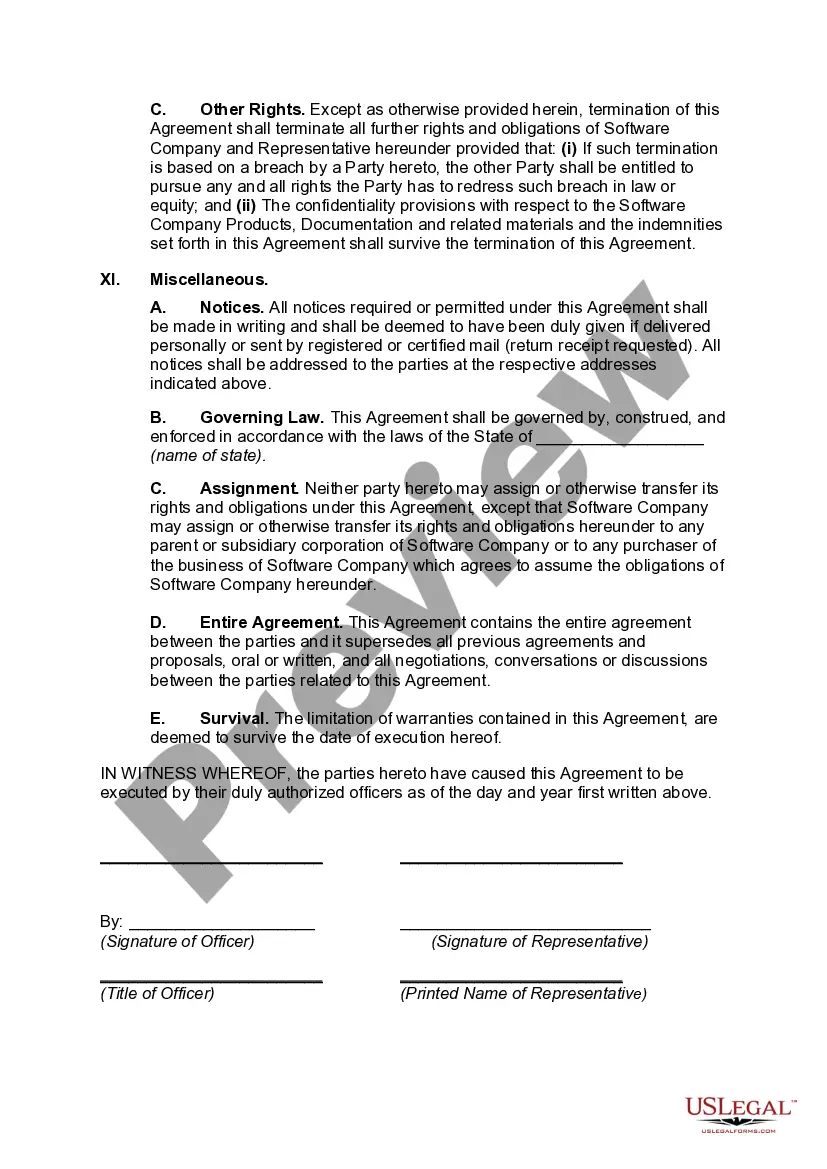

Title: Understanding the New York Independent Sales Representative Agreement with Developer of Computer Software in Compliance with IRS 20-Part Test Keywords: New York, independent sales representative agreement, computer software, developer, Internal Revenue Service, 20-part test, determining independent contractor status Introduction: In the state of New York, when entering into an agreement between an independent sales representative and a computer software developer, it is crucial to ensure compliance with the Internal Revenue Service's 20-part test for determining independent contractor status. This article aims to provide a detailed description of the agreement and its provisions to satisfy the IRS requirements while protecting the interests of both parties involved. 1. General Overview: The New York Independent Sales Representative Agreement with Developer of Computer Software is a legally binding contract that outlines the relationship and rights of both the independent sales representative and the software developer. This agreement establishes the terms and conditions under which the sales representative will promote and sell the developer's computer software products. 2. Purpose: The primary purpose of this agreement is to achieve compliance with the Internal Revenue Service's 20-part test. The 20-part test helps determine whether the sales representative is classified as an independent contractor or an employee. By satisfying these criteria, both parties can ensure they are meeting their tax obligations and avoiding potential legal disputes. 3. Provisions to Satisfy the 20-Part Test: To meet the requirements of the IRS's 20-part test, certain provisions should be included in the agreement. These provisions may include: a. Independent Contractor Status: Explicitly state that the sales representative is an independent contractor, highlighting their autonomy and control over their work. b. Exclusivity: Specify that the sales representative may represent other software developers or sell other products or services concurrently, thus affirming their independence. c. Payment Structure: Define the commission-based payment arrangement, ensuring it is solely based on results achieved by the sales representative rather than hours worked or specific work requirements, further solidifying independent contractor status. d. Expenses: Clarify that the sales representative is responsible for their own business-related expenses, such as travel, marketing materials, and other costs. e. Termination and Non-Compete: Outline the terms of termination and any applicable non-compete clauses. These provisions may restrict the sales representative from engaging in a similar business within a specified geographical area for a certain time period after the agreement ends. f. Taxes and Benefits: Clearly state that the sales representative is responsible for their own taxes and benefits, affirming their independent contractor status. g. Indemnification and Liability: Define the responsibilities and liabilities of both parties, protecting each from potential legal actions arising from the representative's actions or negligence. Types of New York Independent Sales Representative Agreements with Developer of Computer Software: While the core provisions in an independent sales representative agreement are usually consistent, variations may occur based on the specific circumstances and requirements of the parties involved. Some possible types of agreements could include: 1. Exclusive Sales Representative Agreement: This type of agreement grants the sales representative exclusivity within a designated territory or market, prohibiting the developer from appointing other representatives or competing within that area. 2. Non-Exclusive Sales Representative Agreement: Here, the sales representative is not granted exclusive rights to sell the developer's software products, allowing the developer to engage multiple representatives or sell the products directly. 3. Duration-Specific Sales Representative Agreement: This agreement sets a specific timeframe during which the sales representative is authorized to promote and sell the developer's software products. It may be renewable upon mutual agreement. Conclusion: By understanding the intricacies of the New York Independent Sales Representative Agreement with a Developer of Computer Software, and incorporating provisions that align with the IRS's 20-part test, both the independent sales representative and the software developer can form a mutually beneficial partnership while ensuring compliance with tax laws and minimizing potential legal risks. It is advisable for parties to seek legal counsel or professional advice to tailor the agreement to their specific needs and circumstances.

New York Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status

Description

How to fill out New York Independent Sales Representative Agreement With Developer Of Computer Software With Provisions Intended To Satisfy The Internal Revenue Service's 20 Part Test For Determining Independent Contractor Status?

US Legal Forms - one of many greatest libraries of lawful forms in America - gives a wide range of lawful papers templates you are able to acquire or produce. While using web site, you may get thousands of forms for organization and specific functions, sorted by categories, says, or search phrases.You will find the most recent models of forms like the New York Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status within minutes.

If you have a monthly subscription, log in and acquire New York Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status through the US Legal Forms collection. The Obtain key can look on every single form you see. You gain access to all earlier delivered electronically forms in the My Forms tab of your own bank account.

If you would like use US Legal Forms for the first time, here are straightforward directions to help you get started off:

- Make sure you have picked out the correct form for your personal town/county. Click the Preview key to examine the form`s articles. Read the form outline to ensure that you have chosen the correct form.

- In the event the form does not suit your specifications, utilize the Look for discipline towards the top of the screen to find the one that does.

- In case you are content with the shape, confirm your selection by simply clicking the Buy now key. Then, opt for the pricing plan you prefer and supply your references to sign up on an bank account.

- Approach the deal. Use your Visa or Mastercard or PayPal bank account to perform the deal.

- Choose the format and acquire the shape on your system.

- Make adjustments. Fill out, revise and produce and indication the delivered electronically New York Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status.

Every design you added to your bank account lacks an expiry particular date and is also the one you have for a long time. So, if you wish to acquire or produce another version, just go to the My Forms area and click on about the form you will need.

Get access to the New York Independent Sales Representative Agreement with Developer of Computer Software with Provisions Intended to Satisfy the Internal Revenue Service's 20 Part Test for Determining Independent Contractor Status with US Legal Forms, probably the most substantial collection of lawful papers templates. Use thousands of professional and state-specific templates that fulfill your company or specific demands and specifications.