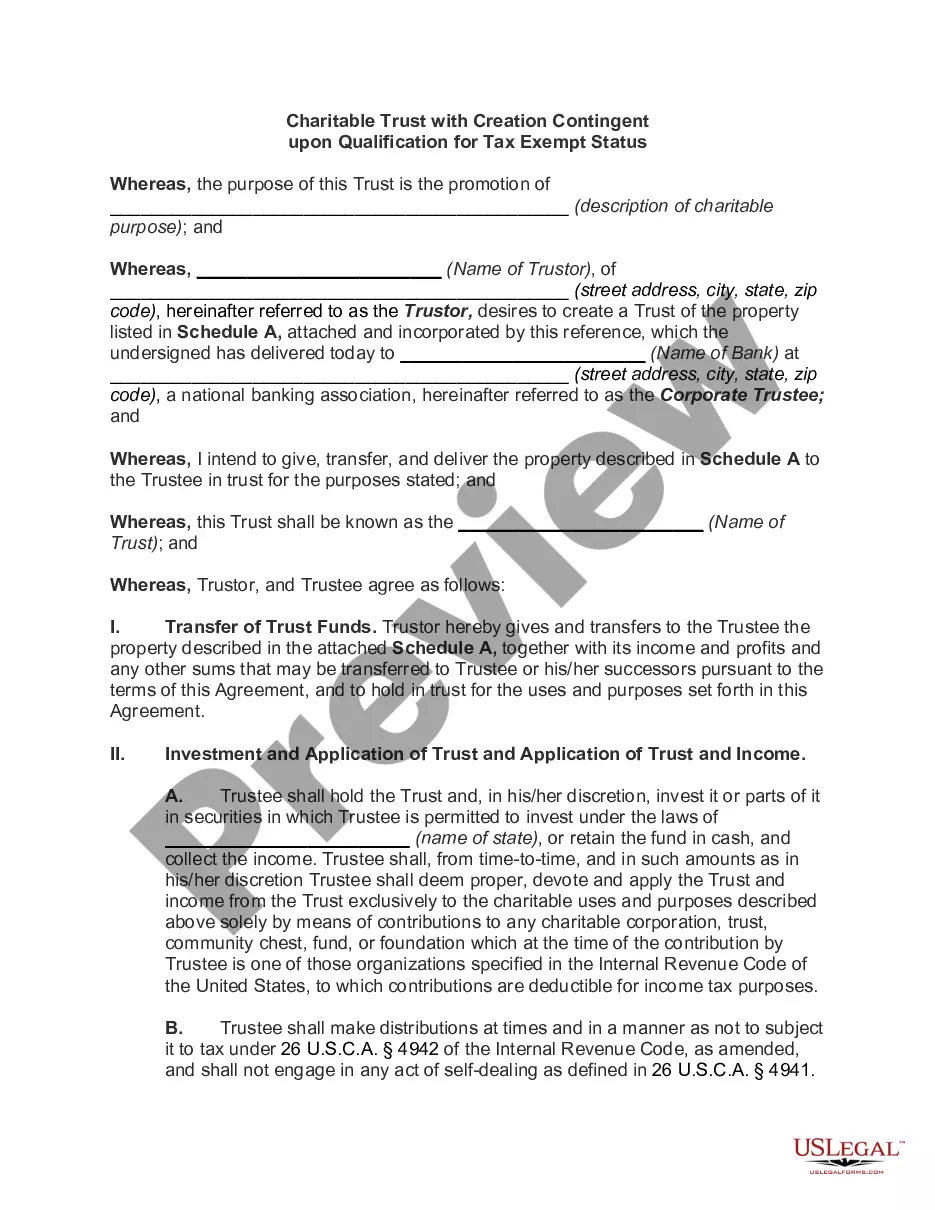

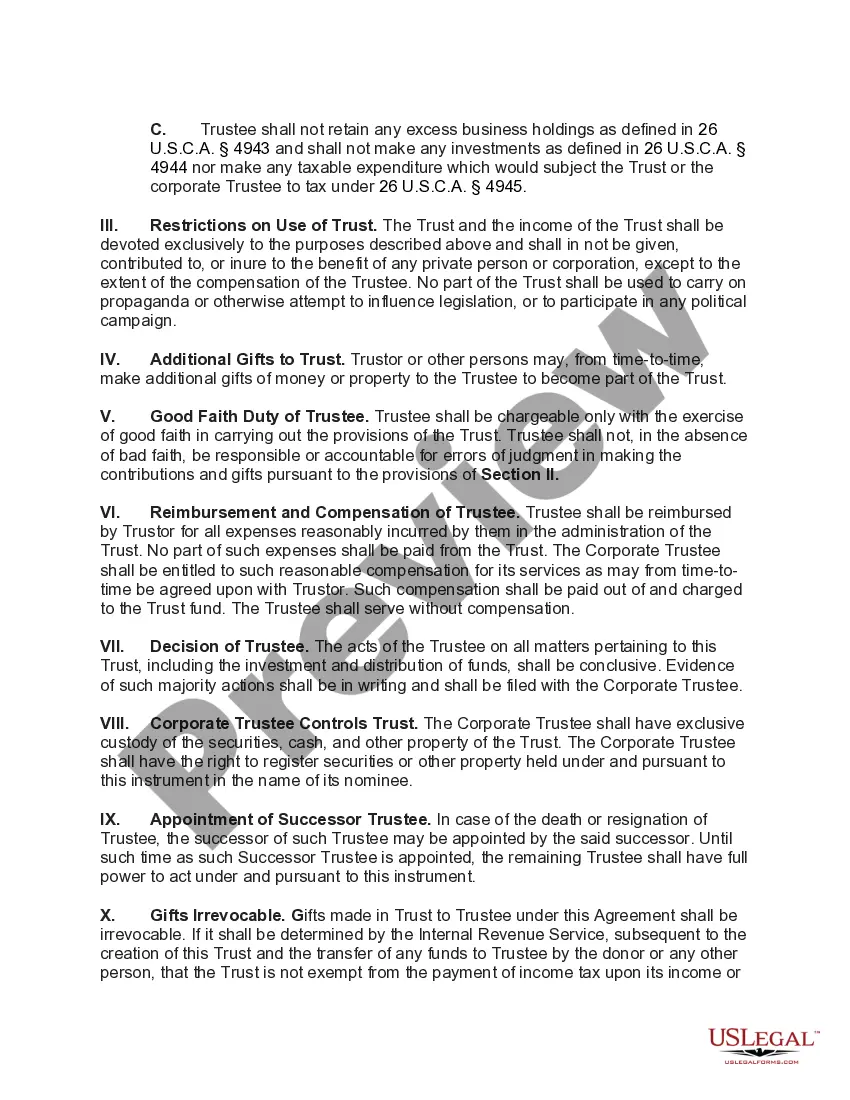

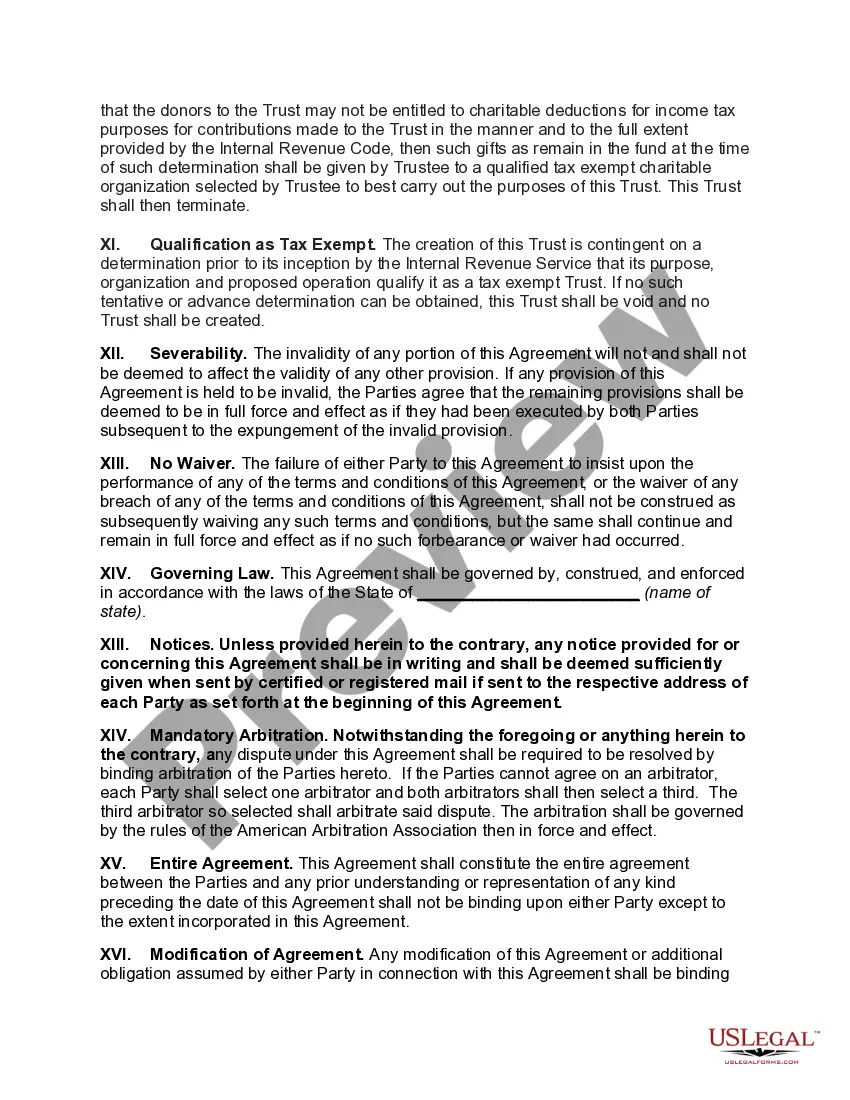

A New York Charitable Trust with creation contingent upon qualification for tax-exempt status refers to a specific type of trust established in the state of New York that is created solely for charitable purposes. This type of trust structure is subject to certain requirements and regulations to obtain tax-exempt status at both the state and federal levels. In order to qualify for tax-exempt status, a New York Charitable Trust must meet the criteria set by the Internal Revenue Service (IRS) and the New York State Department of Taxation and Finance. This includes demonstrating that the trust’s activities and operations are exclusively charitable in nature, providing public benefit, and are not conducted for the benefit of private individuals or organizations. There are different types of New York Charitable Trusts with creation contingent upon qualification for tax-exempt status, namely: 1. New York Charitable Remainder Trust (CRT) with Creation Contingent upon Qualification for Tax Exempt Status: This type of trust allows a donor to transfer assets into a trust while retaining an income stream for a period of time or for life. After this period, the remaining assets are distributed to one or more charitable beneficiaries. The CRT must qualify for tax-exempt status to provide the donor with certain tax advantages. 2. New York Charitable Lead Trust (CLT) with Creation Contingent upon Qualification for Tax Exempt Status: In this trust, income or assets are provided to one or more charitable beneficiaries for a specific period. After this period, the remaining assets are passed on to non-charitable beneficiaries, such as family members or heirs. The CLT must qualify for tax-exempt status to ensure the charitable portion of the trust is eligible for tax benefits. 3. New York Charitable Unit rust with Creation Contingent upon Qualification for Tax Exempt Status: This type of trust provides income to one or more beneficiaries, typically for life or a specific term, after which the remaining assets are distributed to charitable organizations. The unit rust must meet the necessary requirements and qualify for tax-exempt status to ensure tax advantages for both the trust and the beneficiaries. 4. New York Charitable Pooled Income Fund with Creation Contingent upon Qualification for Tax Exempt Status: A pooled income fund is a trust managed by a charitable organization that combines contributions from multiple donors into a single investment pool. Donors receive income from their contributions during their lifetime, and upon their death, the remaining assets are distributed to the designated charitable organizations. For this type of trust to qualify for tax-exempt status, it must adhere to the regulations outlined by the IRS and New York tax authorities. It is important to consult with legal and tax professionals knowledgeable in the creation and administration of New York Charitable Trusts with creation contingent upon qualification for tax-exempt status to ensure compliance with the specific regulations and to maximize the potential tax benefits associated with these trusts.

New York Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status

Description

How to fill out New York Charitable Trust With Creation Contingent Upon Qualification For Tax Exempt Status?

Choosing the best legal papers web template could be a battle. Of course, there are plenty of themes available on the Internet, but how can you get the legal kind you need? Take advantage of the US Legal Forms internet site. The support gives a large number of themes, including the New York Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status, which you can use for business and private needs. All the kinds are examined by professionals and satisfy state and federal specifications.

When you are currently listed, log in to your profile and click the Obtain option to have the New York Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status. Make use of profile to appear through the legal kinds you possess purchased formerly. Check out the My Forms tab of your profile and obtain an additional copy in the papers you need.

When you are a fresh customer of US Legal Forms, here are simple guidelines for you to adhere to:

- Very first, make certain you have selected the correct kind for your personal city/state. You are able to look through the shape using the Review option and read the shape description to guarantee this is basically the best for you.

- When the kind is not going to satisfy your expectations, make use of the Seach discipline to discover the right kind.

- Once you are sure that the shape is proper, click on the Get now option to have the kind.

- Opt for the costs prepare you want and type in the needed details. Design your profile and purchase the order making use of your PayPal profile or charge card.

- Opt for the submit file format and down load the legal papers web template to your product.

- Full, change and printing and signal the acquired New York Charitable Trust with Creation Contingent upon Qualification for Tax Exempt Status.

US Legal Forms will be the largest local library of legal kinds for which you can find different papers themes. Take advantage of the company to down load professionally-created files that adhere to status specifications.