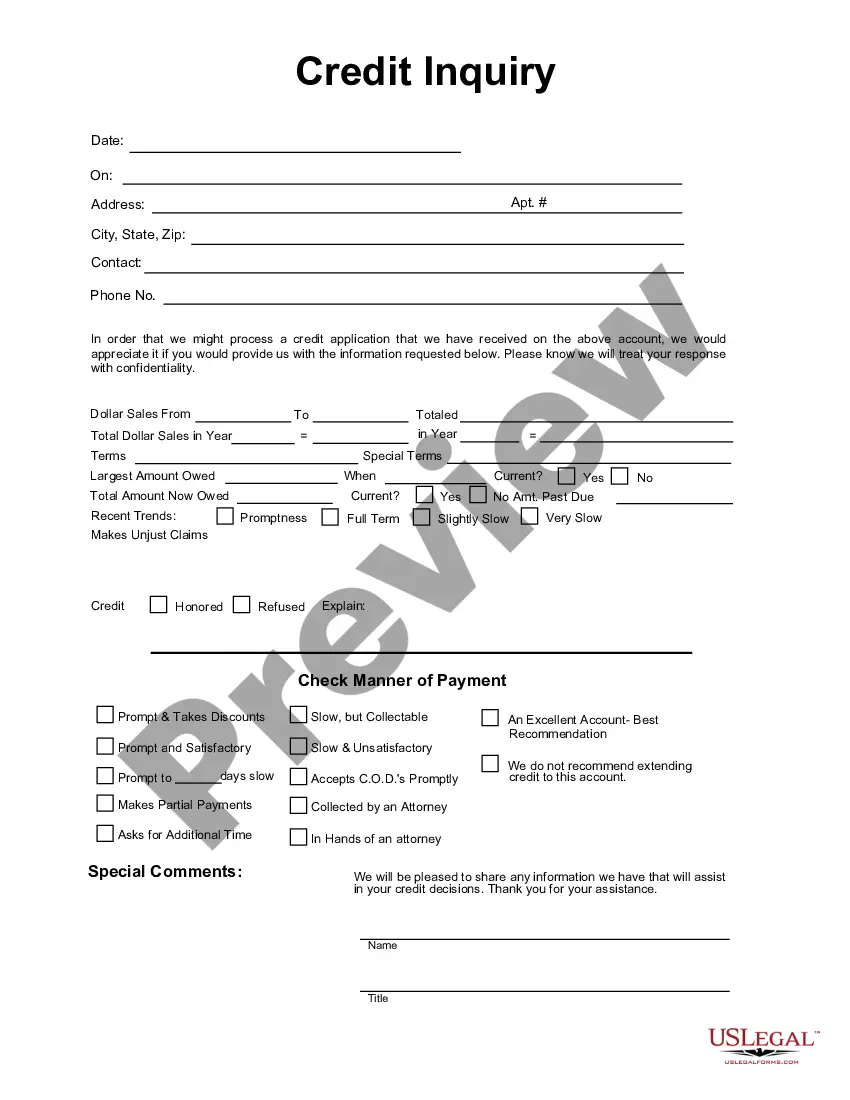

New York Credit Inquiry: A Comprehensive Overview of Types and Benefits Introduction: New York Credit Inquiry refers to the process conducted by financial institutions, lenders, or creditors to collect data on an individual's credit history and evaluate their creditworthiness. This inquiry helps lenders assess the level of risk involved in extending credit to an applicant in the state of New York. The credit inquiry process provides valuable information about a person's financial situation, including outstanding debts, past payment history, and current credit accounts. This detailed description will explore various types of credit inquiries in New York and explain their significance. Types of New York Credit Inquiries: 1. Hard Credit Inquiry: Often initiated by lenders when considering lending decisions, a hard credit inquiry involves a comprehensive review of an individual's credit report. This inquiry impacts the credit score and remains on the credit report for up to two years. Multiple hard inquiries within a short period can negatively impact a credit score, as it may imply increased credit risk. 2. Soft Credit Inquiry: A soft credit inquiry occurs when an individual checks their own credit report or when lenders conduct a pre-approval check. Unlike hard inquiries, soft inquiries do not affect the credit score and are not visible to other creditors. These inquiries are typically conducted for informational purposes or to determine eligibility for promotional offers. 3. Employment Credit Inquiry: Employers in New York may also obtain credit reports of prospective employees as part of their hiring process. These inquiries are conducted with the applicant's permission and help employers assess the candidate's financial responsibility and trustworthiness. 4. Account Monitoring Inquiry: In order to protect consumers from identity theft and fraudulent activities, individuals and credit monitoring services may conduct periodic credit inquiries. These inquiries provide alerts in case of any suspicious activities on the credit report, ensuring immediate action can be taken to alleviate potential harm. 5. Tenant Background Credit Inquiry: Landlords or property management companies in New York often request credit reports from potential tenants to evaluate their ability to pay rent on time. These inquiries help landlords assess an applicant's financial reliability and determine whether they are a suitable candidate for a lease agreement. Benefits of New York Credit Inquiry: 1. Helps Assess Creditworthiness: Credit inquiries allow lenders, employers, and landlords to evaluate an individual's creditworthiness and financial history. This assessment assists in making informed decisions regarding loans, employment, housing, and other credit-related matters. 2. Reduces Default Risk: By conducting credit inquiries, lenders can gauge the likelihood of applicants defaulting on loans. This helps minimize the risk of extending credit to individuals with problematic credit histories, ultimately safeguarding the lenders' financial interests. 3. Protects Consumers: Credit inquiries empower individuals by enabling them to monitor their credit reports regularly. By staying informed about their credit status, consumers can identify and address any errors, discrepancies, or signs of identity theft promptly. Conclusion: New York Credit Inquiry plays a pivotal role in various aspects of personal and financial decision-making. Understanding the different types of credit inquiries, including hard inquiries, soft inquiries, employment inquiries, account monitoring inquiries, and tenant background inquiries, ensures individuals are well-informed about the nature and significance of credit evaluations. By harnessing the benefits of credit inquiries, individuals can actively manage their credit profiles, enhance their creditworthiness, and secure improved access to financial opportunities.

New York Credit Inquiry

Description

How to fill out New York Credit Inquiry?

If you have to complete, down load, or produce authorized record layouts, use US Legal Forms, the largest selection of authorized kinds, which can be found online. Take advantage of the site`s easy and handy search to obtain the documents you want. Various layouts for company and personal purposes are categorized by categories and states, or key phrases. Use US Legal Forms to obtain the New York Credit Inquiry within a couple of mouse clicks.

If you are presently a US Legal Forms consumer, log in for your account and then click the Down load switch to obtain the New York Credit Inquiry. Also you can gain access to kinds you previously acquired in the My Forms tab of your own account.

Should you use US Legal Forms for the first time, refer to the instructions under:

- Step 1. Be sure you have chosen the shape for your proper town/nation.

- Step 2. Make use of the Review choice to look through the form`s information. Do not forget to read through the information.

- Step 3. If you are unsatisfied with all the kind, take advantage of the Research industry near the top of the display screen to discover other versions in the authorized kind format.

- Step 4. After you have found the shape you want, click the Acquire now switch. Opt for the pricing program you favor and include your qualifications to register to have an account.

- Step 5. Procedure the financial transaction. You can use your Мisa or Ьastercard or PayPal account to finish the financial transaction.

- Step 6. Find the format in the authorized kind and down load it on your system.

- Step 7. Comprehensive, change and produce or signal the New York Credit Inquiry.

Each and every authorized record format you acquire is the one you have permanently. You possess acces to each and every kind you acquired in your acccount. Go through the My Forms segment and choose a kind to produce or down load again.

Remain competitive and down load, and produce the New York Credit Inquiry with US Legal Forms. There are many skilled and condition-distinct kinds you can utilize for the company or personal requires.