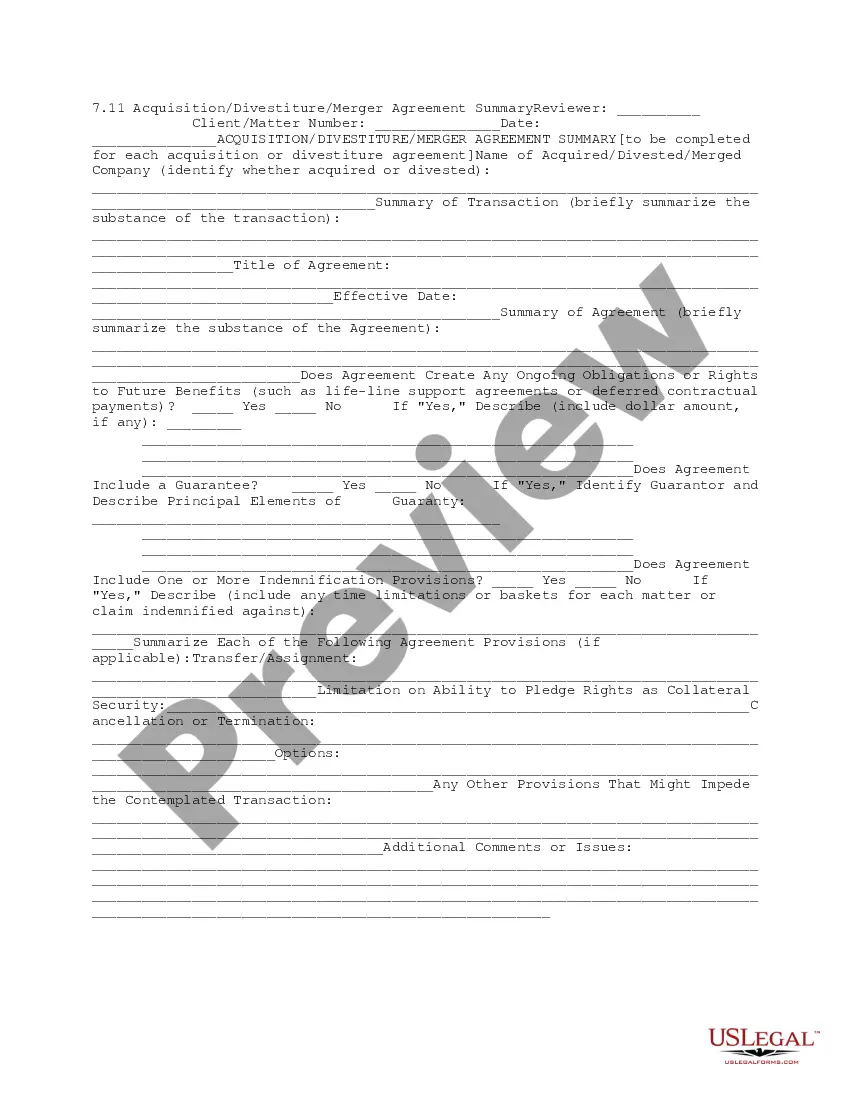

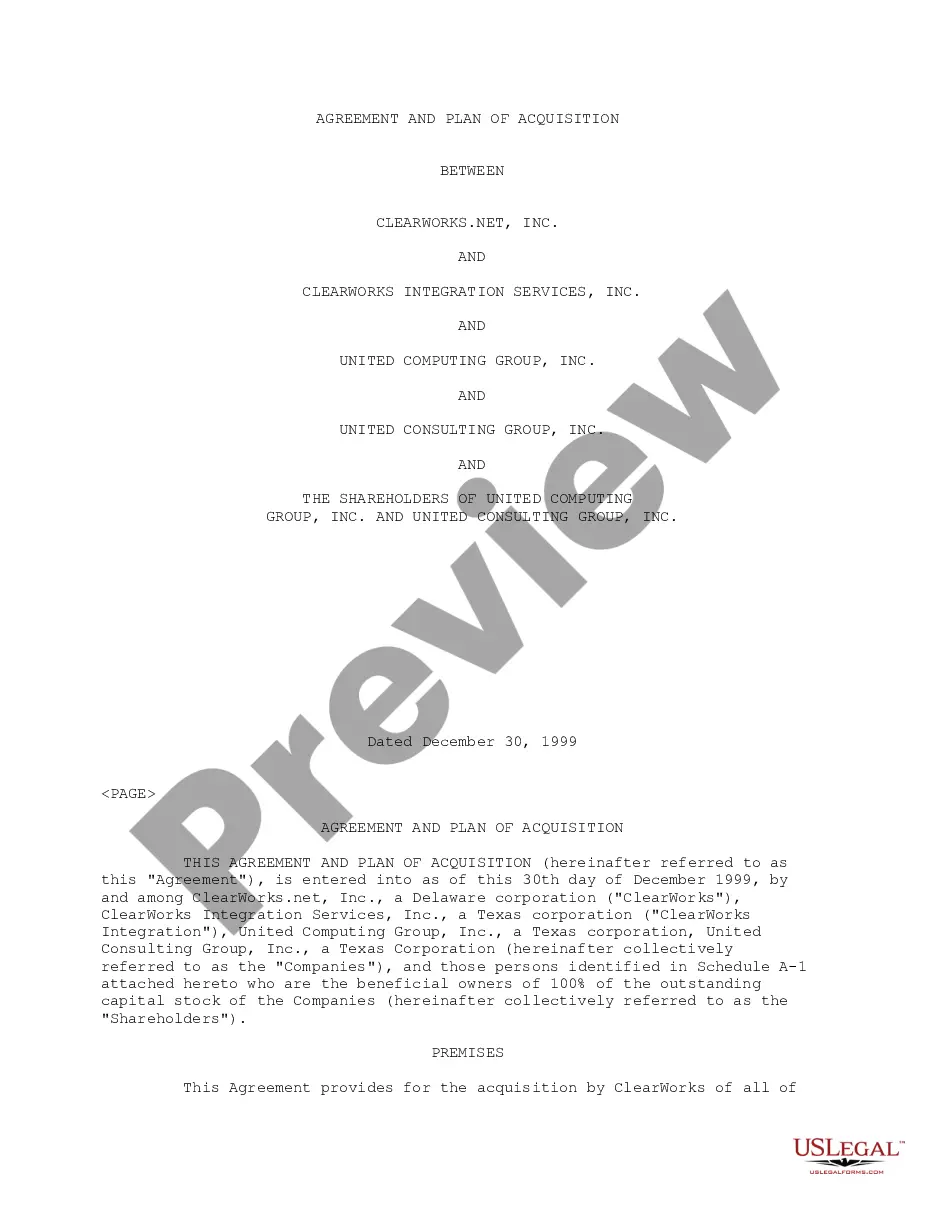

New York Acquisition, Merger, or Liquidation

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acquisition, Merger, Or Liquidation?

If you need to complete, down load, or produce lawful papers web templates, use US Legal Forms, the most important variety of lawful types, which can be found on the Internet. Utilize the site`s basic and handy look for to get the documents you want. A variety of web templates for organization and specific uses are categorized by classes and claims, or key phrases. Use US Legal Forms to get the New York Acquisition, Merger, or Liquidation with a handful of clicks.

If you are previously a US Legal Forms consumer, log in for your account and click the Obtain key to have the New York Acquisition, Merger, or Liquidation. You may also access types you earlier saved inside the My Forms tab of your own account.

If you are using US Legal Forms initially, follow the instructions listed below:

- Step 1. Be sure you have chosen the shape for the appropriate town/land.

- Step 2. Take advantage of the Review choice to examine the form`s content. Don`t forget about to read through the information.

- Step 3. If you are not satisfied with the type, make use of the Look for field at the top of the monitor to get other versions from the lawful type web template.

- Step 4. Upon having located the shape you want, click the Acquire now key. Choose the costs program you prefer and put your accreditations to register for the account.

- Step 5. Approach the transaction. You should use your charge card or PayPal account to complete the transaction.

- Step 6. Find the format from the lawful type and down load it in your product.

- Step 7. Comprehensive, edit and produce or indicator the New York Acquisition, Merger, or Liquidation.

Each lawful papers web template you purchase is your own property forever. You might have acces to each and every type you saved inside your acccount. Click the My Forms portion and decide on a type to produce or down load yet again.

Remain competitive and down load, and produce the New York Acquisition, Merger, or Liquidation with US Legal Forms. There are many skilled and express-certain types you may use for your organization or specific requirements.

Form popularity

FAQ

While other consideration besides stock can be paid under a type A reorganization, the price paid under a type B reorganization must be solely in stock. And while the target is dissolved in a type A reorganization, it can be retained in a type B reorganization.

A liquidation or administration can happen during or after an acquisition. An acquisition is a process that occurs when one company decides to take over the operations of another company.

A transferor in a Section 351 transfer does not recognize gain or loss when it transfers property to the controlled corporation in exchange for its stock. A transferor may recognize gain (but not loss) to the extent of any money or other property (boot) received in addition to the corporation's stock.

Section 351(a) provides that no gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control (as defined in § 368(c)) of the corporation.

Overview. In a D reorganization, one corporation transfers all or part of its assets to another corporation. Immediately after the transfer, the transferring corporation or one or more of its shareholders must be in control of the corporation that acquired the assets.

In a B reorganization, the Acquirer transfers its stock in exchange for the stock of the Target. In a Code Section 351 transaction, a transferor (which can be a corporation) transfers property and receives stock in the transferee corporation.

A Type "B" reorganization is a stock-for-stock transaction in which one corporation (the acquiring corporation) acquires the stock of another corporation (the target corporation). Only voting stock of the acquiring corporation or its parent may be used in the acquisition.

To avoid dual convictions, the courts have created the merger doctrine. Under it, the court may vacate a false imprisonment or kidnapping conviction where the period of abduction is brief and there is no kidnapping flavor to the case. Under these circumstances, the charges are said to merge together.