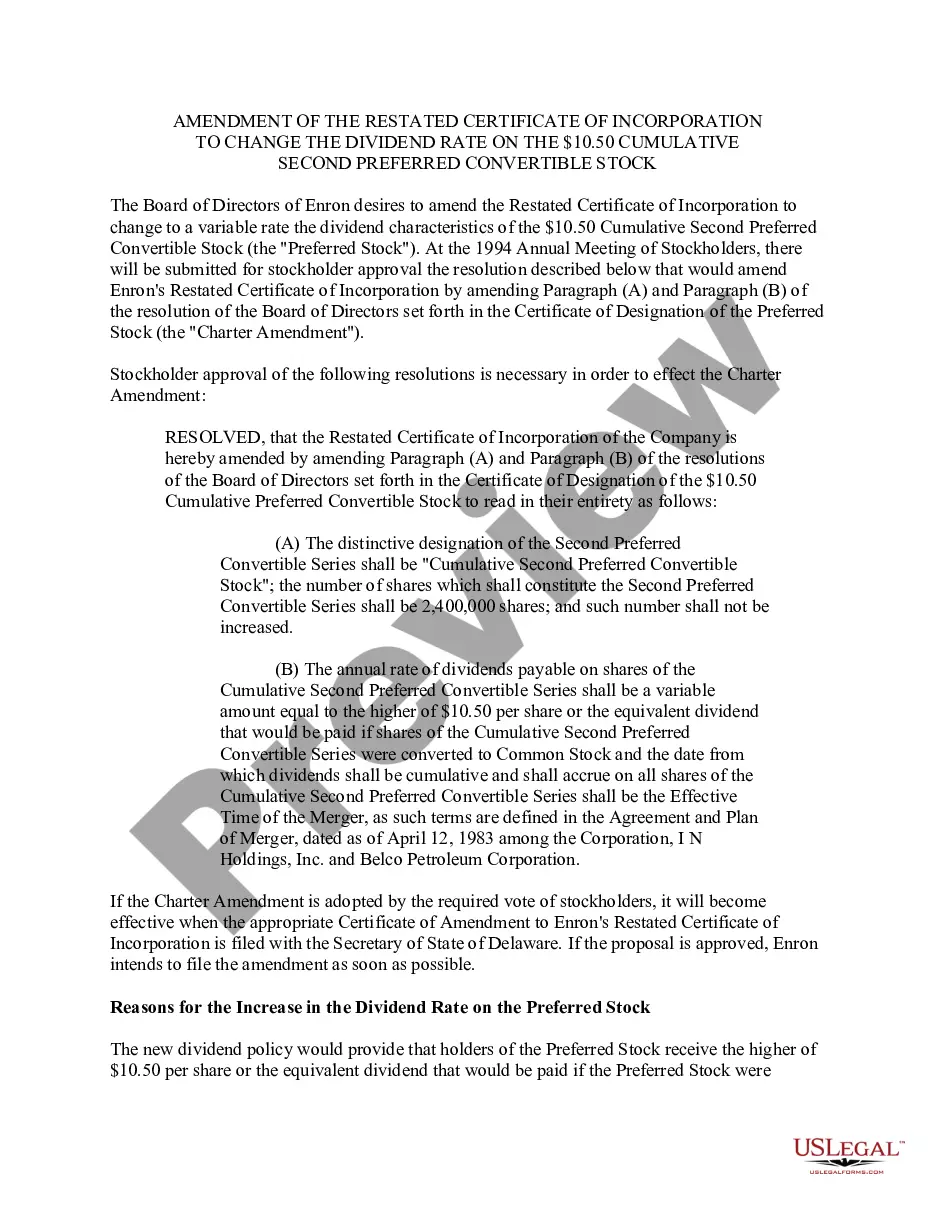

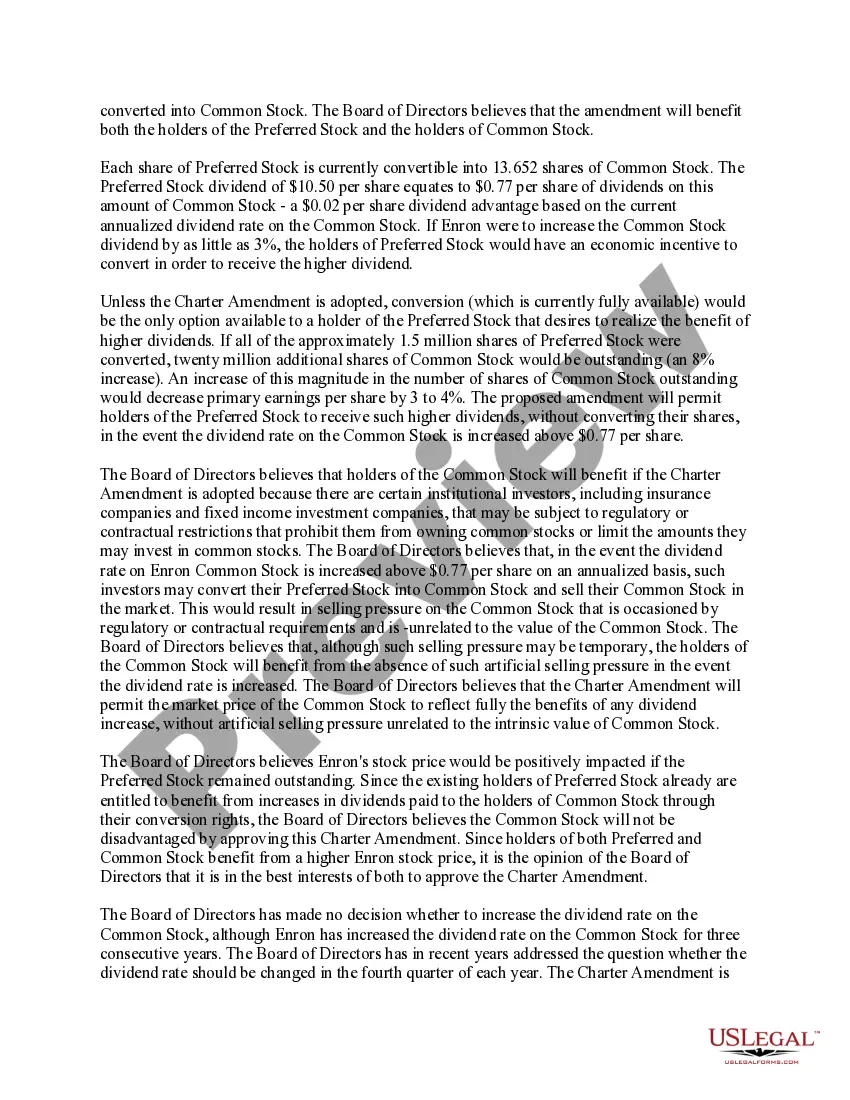

The New York Amendment of Restated Certificate of Incorporation allows for the adjustment of the dividend rate on the $10.50 cumulative second preferred convertible stock for companies incorporated in New York. This amendment is particularly relevant for companies seeking to modify the terms of their preferred stock and align it with their financial goals. By changing the dividend rate, companies can adjust the payment amount on their $10.50 cumulative second preferred convertible stock to either increase or decrease the income flow to shareholders. The New York Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock offers flexibility for companies in varying industries and financial situations. It enables businesses to adapt their dividend policies to reflect changing market conditions, financial performance, and shareholder requirements. By utilizing this amendment, companies can respond promptly to market fluctuations while ensuring the stability and growth of their capital structure. Types of New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock include: 1. Increase in Dividend Rate: Companies may opt to increase the dividend rate on their $10.50 cumulative second preferred convertible stock through this amendment. This adjustment could be driven by factors such as improved financial performance, higher profitability, or the need to attract more investors. 2. Decrease in Dividend Rate: In some cases, companies may choose to lower the dividend rate on their $10.50 cumulative second preferred convertible stock. This action could be triggered by a desire to retain more earnings for reinvestment, reduce financial obligations, or adjust the stock's competitiveness compared to other investment options. 3. Temporary Suspension of Dividends: In certain circumstances, companies may find it necessary to temporarily suspend dividends on their $10.50 cumulative second preferred convertible stock. This may occur during periods of financial constraints or economic uncertainties, aiming to preserve cash flow and ensure overall business stability. 4. Conditional Dividend Mechanisms: The New York Amendment of Restated Certificate of Incorporation also allows for the introduction of conditional dividend mechanisms on the $10.50 cumulative second preferred convertible stock. This can be implemented to link dividend payments to specific financial benchmarks, performance targets, or other predetermined criteria, offering greater flexibility to adapt to changing business circumstances. By utilizing the New York Amendment of Restated Certificate of Incorporation to change the dividend rate on $10.50 cumulative second preferred convertible stock, companies can effectively manage their capital structure and adapt to evolving financial conditions while meeting the needs of their shareholders.

New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out New York Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

If you want to complete, acquire, or produce legitimate file themes, use US Legal Forms, the most important assortment of legitimate varieties, that can be found on the web. Take advantage of the site`s simple and handy look for to get the documents you will need. Various themes for company and specific functions are categorized by types and says, or keywords. Use US Legal Forms to get the New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock with a couple of mouse clicks.

When you are already a US Legal Forms consumer, log in to your account and click on the Download key to obtain the New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. You can also access varieties you earlier acquired within the My Forms tab of your respective account.

Should you use US Legal Forms the first time, follow the instructions under:

- Step 1. Be sure you have chosen the form for your right city/nation.

- Step 2. Utilize the Preview choice to look through the form`s information. Never forget to read through the information.

- Step 3. When you are not happy with all the form, utilize the Look for area at the top of the display screen to get other versions of your legitimate form format.

- Step 4. After you have located the form you will need, select the Purchase now key. Opt for the costs strategy you like and put your qualifications to register on an account.

- Step 5. Process the transaction. You can utilize your bank card or PayPal account to complete the transaction.

- Step 6. Find the formatting of your legitimate form and acquire it in your product.

- Step 7. Complete, edit and produce or indicator the New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

Every legitimate file format you acquire is your own property permanently. You might have acces to every form you acquired in your acccount. Go through the My Forms segment and pick a form to produce or acquire yet again.

Be competitive and acquire, and produce the New York Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock with US Legal Forms. There are many professional and condition-particular varieties you may use to your company or specific requirements.