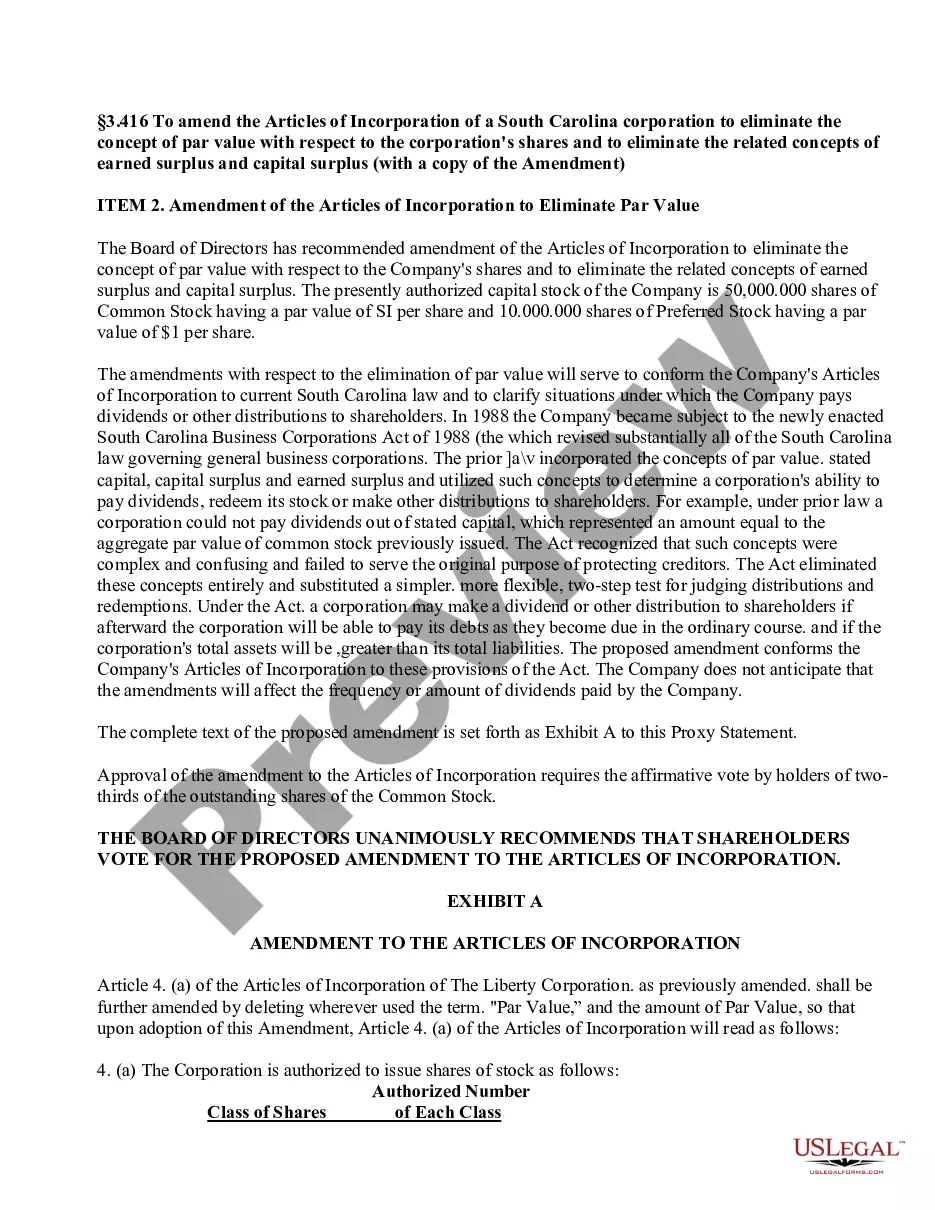

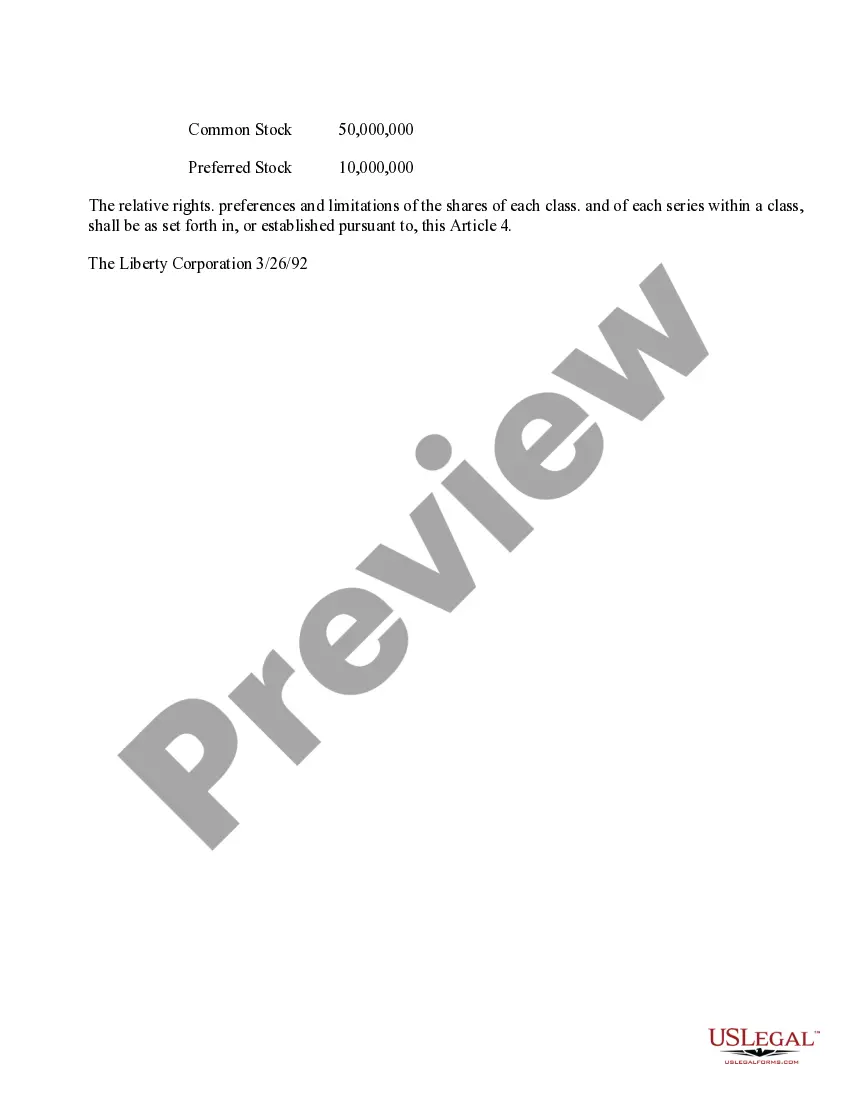

New York Amendment to the Articles of Incorporation to Eliminate Par Value In the state of New York, businesses have the option to amend their articles of incorporation to eliminate the par value of their shares. This modification allows the company to issue shares without any stated minimum value, granting them more flexibility in raising capital and conducting business transactions. Here, we will provide a detailed description of what this amendment entails, its benefits, the process of incorporation amendment, and its different types. The elimination of par value in the articles of incorporation is designed to remove the predetermined minimum price at which shares can be issued by a company. In traditional terms, par value represents the minimum value of each share set by the company. However, it is essential to note that par value does not reflect the actual market value of the shares and often has no relevance in modern business scenarios. By eliminating par value, businesses allow for shares to be issued at any price agreed upon by the company and the investors, usually reflecting the current market conditions. One of the primary benefits of eliminating par value is increased flexibility. This amendment enables companies to adapt better to the demands of potential investors or the capital market. By removing the constraints of par value, companies can offer shares at a more suitable price in relation to their actual value, thereby attracting more investors and potentially raising more capital. Moreover, the absence of par value simplifies accounting and financial reporting procedures by removing the need to allocate amounts to stated capital based on par value. The process of amending the articles of incorporation in New York to eliminate par value involves several steps. Firstly, the company's board of directors must propose the amendment and provide a detailed explanation of the rationale behind the change. This proposal is then presented to the shareholders, who must vote and approve the amendment. The exact requirements for approval may vary based on the company's bylaws, but typically a majority vote is sufficient to pass the amendment. Subsequently, the amended articles of incorporation, which reflect the elimination of par value, must be filed with the New York Department of State, Division of Corporations. While there aren't different types of New York amendments to eliminate par value, it is worth noting that companies may choose to replace par value with a "no par value" statement or establish a "stated value" for their shares. A "no par value" provision indicates that there is no minimum price associated with the shares, offering maximum flexibility. On the other hand, a "stated value" provision assigns an arbitrary value to shares, which may still impose some constraints but allows for a greater degree of flexibility compared to traditional par value. In conclusion, the New York Amendment to the Articles of Incorporation to eliminate par value grants companies the freedom to issue shares at any agreed-upon price, removing unnecessary constraints and increasing flexibility in raising capital. This modification simplifies accounting procedures and makes the company more attractive to potential investors. Companies in New York considering this amendment must follow the prescribed process, gaining approval from shareholders and officially filing the amended articles with the appropriate authorities. Whether choosing a "no par value" provision or establishing a "stated value," companies can tailor their amendment to reflect their specific needs and goals.

New York Amendment to the articles of incorporation to eliminate par value

Description

How to fill out New York Amendment To The Articles Of Incorporation To Eliminate Par Value?

Have you been within a place the place you need papers for possibly business or individual uses almost every day time? There are a variety of legal papers layouts available online, but locating types you can depend on is not effortless. US Legal Forms offers a large number of kind layouts, like the New York Amendment to the articles of incorporation to eliminate par value, that happen to be created to satisfy federal and state demands.

When you are previously familiar with US Legal Forms web site and also have your account, basically log in. Next, you can obtain the New York Amendment to the articles of incorporation to eliminate par value format.

If you do not come with an accounts and want to begin using US Legal Forms, adopt these measures:

- Get the kind you require and ensure it is to the appropriate city/state.

- Take advantage of the Preview option to analyze the shape.

- See the description to actually have selected the right kind.

- In case the kind is not what you`re seeking, take advantage of the Research discipline to discover the kind that meets your requirements and demands.

- Once you discover the appropriate kind, click Acquire now.

- Select the costs plan you need, complete the necessary information and facts to create your bank account, and pay for your order making use of your PayPal or credit card.

- Select a convenient data file formatting and obtain your copy.

Find each of the papers layouts you might have bought in the My Forms menus. You can get a more copy of New York Amendment to the articles of incorporation to eliminate par value whenever, if required. Just select the necessary kind to obtain or produce the papers format.

Use US Legal Forms, by far the most considerable collection of legal varieties, to conserve efforts and steer clear of errors. The services offers professionally manufactured legal papers layouts that can be used for a range of uses. Create your account on US Legal Forms and commence creating your way of life a little easier.