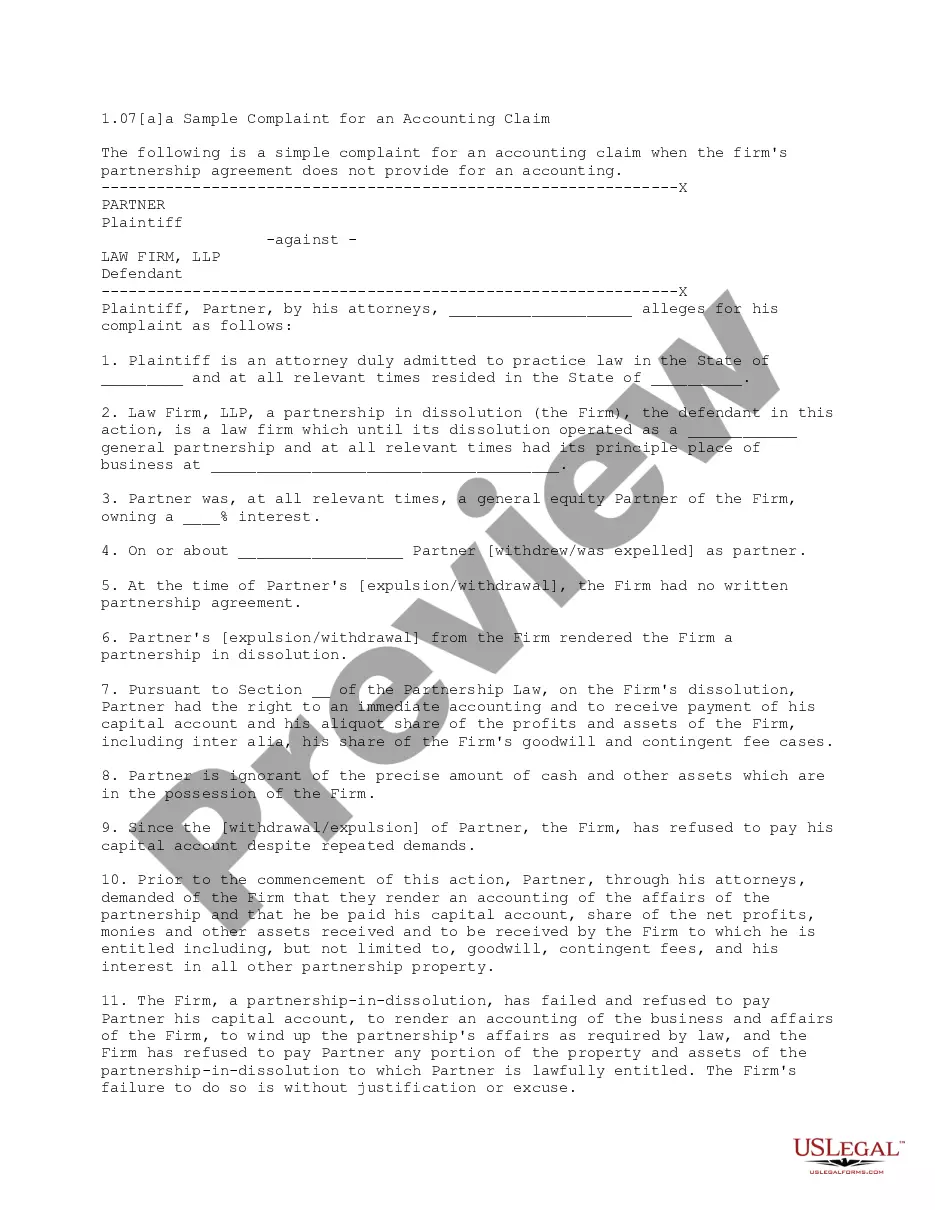

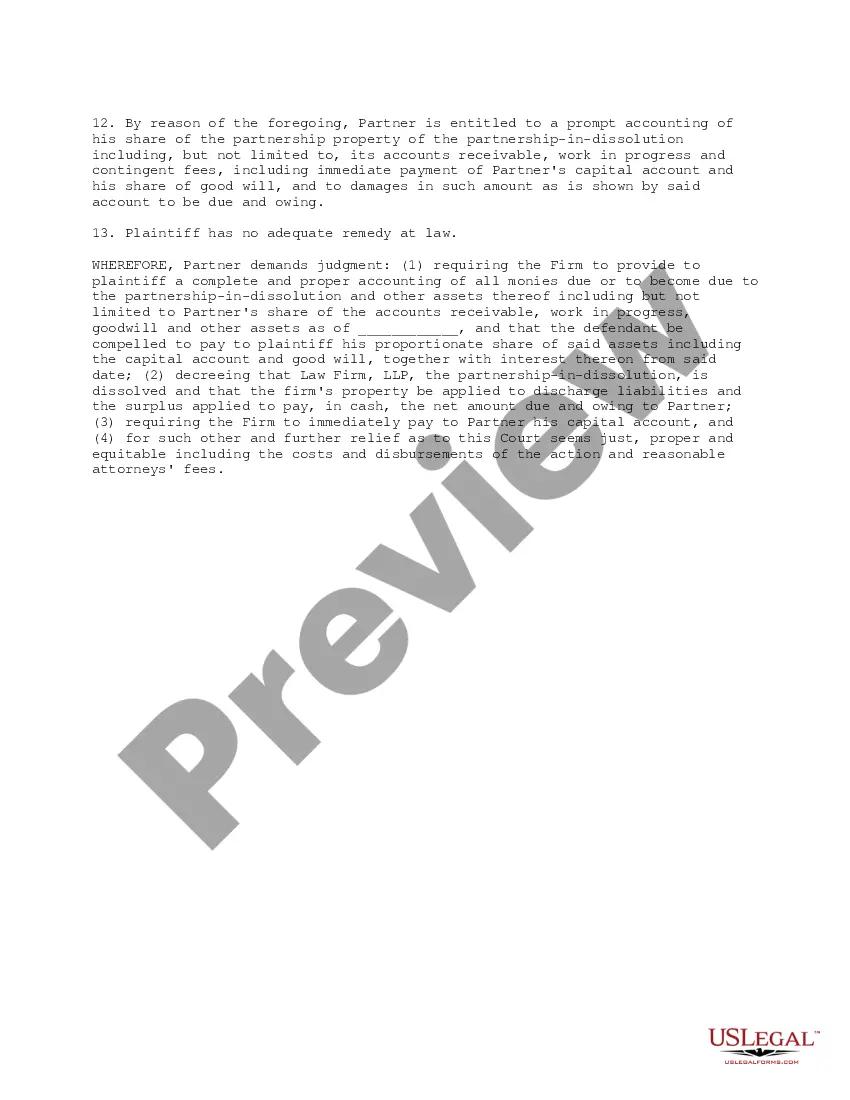

This is a complaint to be filed by a former law partner who has been expelled from his law firm. It calls for an accounting of the firm, where the firm's partnership agreement did not provide for an accounting. The former partner alleges that the partnership has failed to pay him what was rightfully due, and asks for an accounting to calculate damages owing.

A New York Complaint for an Accounting Claim is a legal document that outlines the allegations and demands made by an individual or business entity against an accounting professional or firm based in New York. This complaint is filed with the court system to seek redress for the alleged misconduct, negligence, or breach of duty by the accounting professional or firm. It is important to note that New York has specific rules and regulations governing complaints related to accounting claims. In this Complaint, the plaintiff (the party filing the complaint) must provide a detailed account of the facts supporting their claim. This can include instances of fraudulent activity, misrepresentation of financial information, improper accounting practices, conflicts of interest, or other professional misconduct. The plaintiff must also present evidence establishing the damages suffered as a result of the accounting professional's or firm's actions or inaction. The New York Complaint for an Accounting Claim should contain precise language, clearly stating the legal grounds upon which the claim is based. Common legal grounds for accounting claims in New York can include breach of contract, negligence, professional malpractice, violation of accounting standards, breach of fiduciary duty, or fraudulent misrepresentation, among others. It is important to note that there may be different types of New York Complaints for an Accounting Claim, depending on the specific circumstances and legal claims involved. Some common types of accounting claims in New York include: 1. Breach of Contract: This type of complaint arises when an accounting professional or firm fails to fulfill the terms and conditions specified in a written or oral contract. For example, if an accounting firm fails to deliver financial statements within the agreed-upon timeframe. 2. Negligence: In cases of negligence, a plaintiff alleges that the accounting professional or firm acted in a careless or substandard manner, resulting in financial harm. It can involve situations where the accountant makes errors or mistakes in preparing financial statements or provides incorrect advice. 3. Professional Malpractice: This claim suggests that the accounting professional's conduct fell below the accepted professional standards, resulting in financial losses for the plaintiff. It usually requires demonstrating that the accountant deviated from the standard of care expected within the industry. 4. Fraudulent Misrepresentation: This complaint arises when an accounting professional or firm deliberately provides false information or conceals material facts that induce the plaintiff to rely on inaccurate financial statements or advice, resulting in financial harm. 5. Breach of Fiduciary Duty: This claim alleges that the accounting professional or firm failed to act in the best interest of the plaintiff, breaching their fiduciary duty to provide accurate and transparent financial information. It is crucial to consult with an experienced attorney specializing in accounting claims in New York to ensure compliance with specific legal requirements and to properly draft a Complaint that effectively represents the plaintiff's case.A New York Complaint for an Accounting Claim is a legal document that outlines the allegations and demands made by an individual or business entity against an accounting professional or firm based in New York. This complaint is filed with the court system to seek redress for the alleged misconduct, negligence, or breach of duty by the accounting professional or firm. It is important to note that New York has specific rules and regulations governing complaints related to accounting claims. In this Complaint, the plaintiff (the party filing the complaint) must provide a detailed account of the facts supporting their claim. This can include instances of fraudulent activity, misrepresentation of financial information, improper accounting practices, conflicts of interest, or other professional misconduct. The plaintiff must also present evidence establishing the damages suffered as a result of the accounting professional's or firm's actions or inaction. The New York Complaint for an Accounting Claim should contain precise language, clearly stating the legal grounds upon which the claim is based. Common legal grounds for accounting claims in New York can include breach of contract, negligence, professional malpractice, violation of accounting standards, breach of fiduciary duty, or fraudulent misrepresentation, among others. It is important to note that there may be different types of New York Complaints for an Accounting Claim, depending on the specific circumstances and legal claims involved. Some common types of accounting claims in New York include: 1. Breach of Contract: This type of complaint arises when an accounting professional or firm fails to fulfill the terms and conditions specified in a written or oral contract. For example, if an accounting firm fails to deliver financial statements within the agreed-upon timeframe. 2. Negligence: In cases of negligence, a plaintiff alleges that the accounting professional or firm acted in a careless or substandard manner, resulting in financial harm. It can involve situations where the accountant makes errors or mistakes in preparing financial statements or provides incorrect advice. 3. Professional Malpractice: This claim suggests that the accounting professional's conduct fell below the accepted professional standards, resulting in financial losses for the plaintiff. It usually requires demonstrating that the accountant deviated from the standard of care expected within the industry. 4. Fraudulent Misrepresentation: This complaint arises when an accounting professional or firm deliberately provides false information or conceals material facts that induce the plaintiff to rely on inaccurate financial statements or advice, resulting in financial harm. 5. Breach of Fiduciary Duty: This claim alleges that the accounting professional or firm failed to act in the best interest of the plaintiff, breaching their fiduciary duty to provide accurate and transparent financial information. It is crucial to consult with an experienced attorney specializing in accounting claims in New York to ensure compliance with specific legal requirements and to properly draft a Complaint that effectively represents the plaintiff's case.