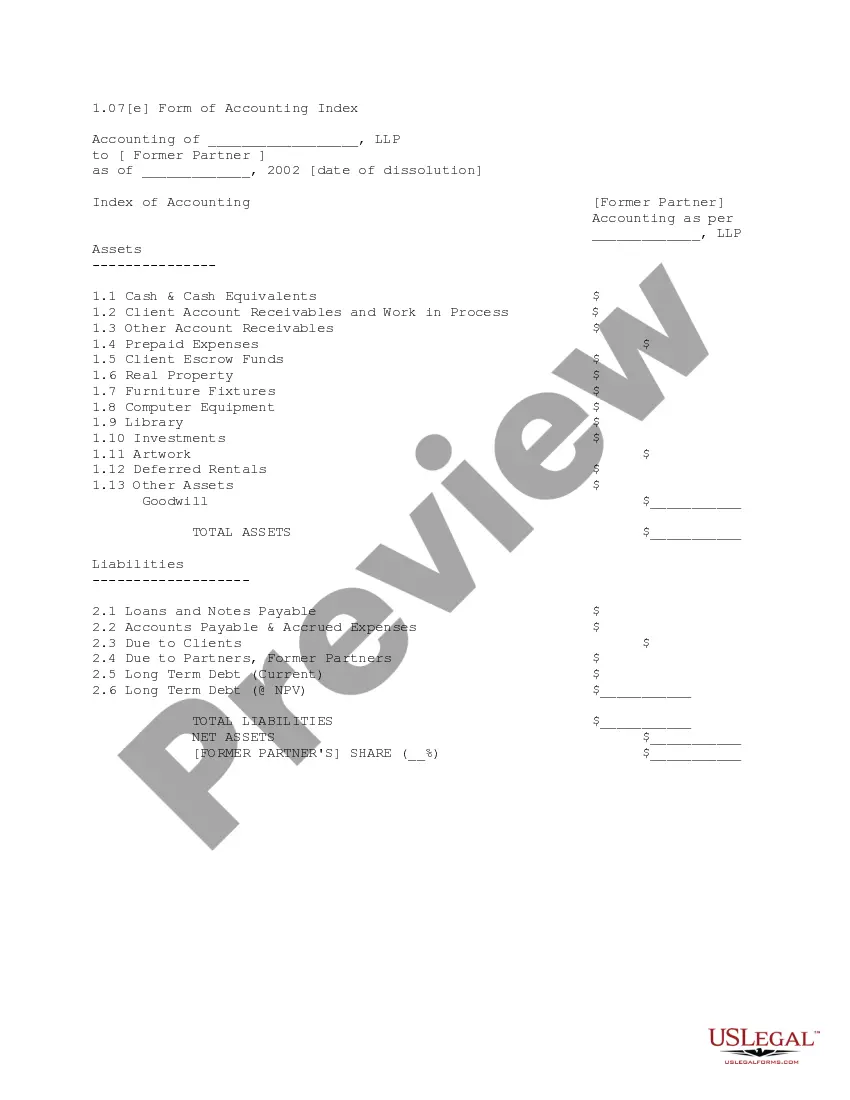

This is the accounting form used in an accounting of a law firm on the complaint of a former partner. It includes assets, liabilities, total liabilities, net assets, and a computation of the former partner's share.

New York Form of Accounting Index

Category:

State:

Multi-State

Control #:

US-L0107E

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out New York Form Of Accounting Index?

You can devote hrs on-line trying to find the authorized file web template that meets the federal and state requirements you want. US Legal Forms provides a huge number of authorized kinds that happen to be reviewed by specialists. It is simple to download or print out the New York Form of Accounting Index from my assistance.

If you already have a US Legal Forms account, you are able to log in and click on the Acquire key. Afterward, you are able to complete, edit, print out, or indicator the New York Form of Accounting Index. Each and every authorized file web template you acquire is the one you have eternally. To have another version for any bought develop, proceed to the My Forms tab and click on the corresponding key.

If you work with the US Legal Forms internet site initially, stick to the easy guidelines under:

- Very first, make sure that you have selected the right file web template to the area/town that you pick. See the develop information to ensure you have selected the right develop. If available, use the Review key to appear with the file web template at the same time.

- If you want to discover another edition from the develop, use the Research field to discover the web template that meets your requirements and requirements.

- Upon having found the web template you desire, click Purchase now to move forward.

- Pick the pricing prepare you desire, type in your references, and sign up for an account on US Legal Forms.

- Complete the financial transaction. You should use your credit card or PayPal account to purchase the authorized develop.

- Pick the formatting from the file and download it to the system.

- Make alterations to the file if necessary. You can complete, edit and indicator and print out New York Form of Accounting Index.

Acquire and print out a huge number of file themes using the US Legal Forms site, that offers the largest variety of authorized kinds. Use professional and status-certain themes to deal with your company or individual requirements.

Form popularity

FAQ

BPC section 5079 permits minority ownership of a public accounting firm by individuals who are not licensed CPAs or PAs. The number of licensed partners as owners must be greater than the number of unlicensed persons. The only exception is that a firm with two owners may have one owner who is a non-licensee.

Legislation effective September 1, 2007 created a practice privilege for CPAs and CPA firms licensed in a substantially equivalent state to temporarily practice in Texas without a Texas license.

Many state accountancy laws provide for similar restrictions in that a firm must contain only partners or shareholders who are CPAs in order to hold itself out as a CPA firm. The AICPA has no similar restrictions on the formation of a partnership for the practice of public accounting with non-CPAs.

Non-CPA ownership could strain the perception and reality of independence in the attest function because of the pressures the non-CPA owner might place on the firm as a business unit to produce more profits.

Is there CPA reciprocity in New York? Yes. New York offers licensure by endorsement to CPA license-holders from substantially equivalent states. However, in the last 10 years, candidates must have 4 years of combined experience in accounting, financial advisory, financial management, or tax services.

Transfer CPA license to New YorkIf you are licensed in a different state, you can get licensure by endorsement. You are eligible for this if you have completed four years of accepted work experience within the last 10 years. People who have practiced as accountants internationally can apply for licensure in New York.

§7403.State board for public accountancy.

The CPA would theoretically submit a simple one-page notice form and automatically qualify for practice privileges in another state. A CPA with practice privileges in another state is not considered a licensee and is not required to comply with the CPE requirements of that state.

New Jersey, Pennsylvania, Connecticut, Massachusettsevery state in the Union except for New York and Hawaiiallow non-CPAs to hold a minority ownership stake in a CPA firm. The sky hasn't fallen. CPA firms are still CPA firms, even with non-CPAs contributing to their growth.

Firms with non-CPA ownership will not be allowed to register. New York State law does not permit firms that have unlicensed ownership to register or practice public accountancy in NYS.

More info

Please note, the Federal Reserve Banks of Dallas, New York, Richmond, and St. Louis do not accept requests for Discount Window Loan or Collateral information ... New York State InitiativesThe Department of Financial Services supervises many different types of institutions. Supervision by DFS may entail chartering, ...For a list of all industries with employment in Accountants and Auditors, see the Create CustomizedNew York, 111,660, 12.88, 1.38, $ 50.86, $ 105,790. Index Number Application (PDF) (Fillable PDF File) Index Number Application (DOC) (Doc File), This form is necessary to commence a civil court action. Be a part of one of the largest and most respected accounting programs in the nation. Our Masters of Science in Accounting program provides a generalist, hands- ... New York · California · New Jersey. The states in the bottom 10 tend to have a number of afflictions in common: complex, nonneutral taxes with comparatively ... Search for business topics like employer tax identification number (EIN) information, with the A-Z Index. Search by business type or subject. As an employer, you must record sums that are withheld from employee wages in a ledger account to clearly indicate the amount of state tax withheld. These funds ... The NYSSCPA has prepared a glossary of accounting terms for accountants andA taxpayer, whether business or individual, must file a request on a form. The School Fiscal Services Division hosted a webinar on August 3, 2021, to provide guidance on independent study attendance accounting and instructional ...