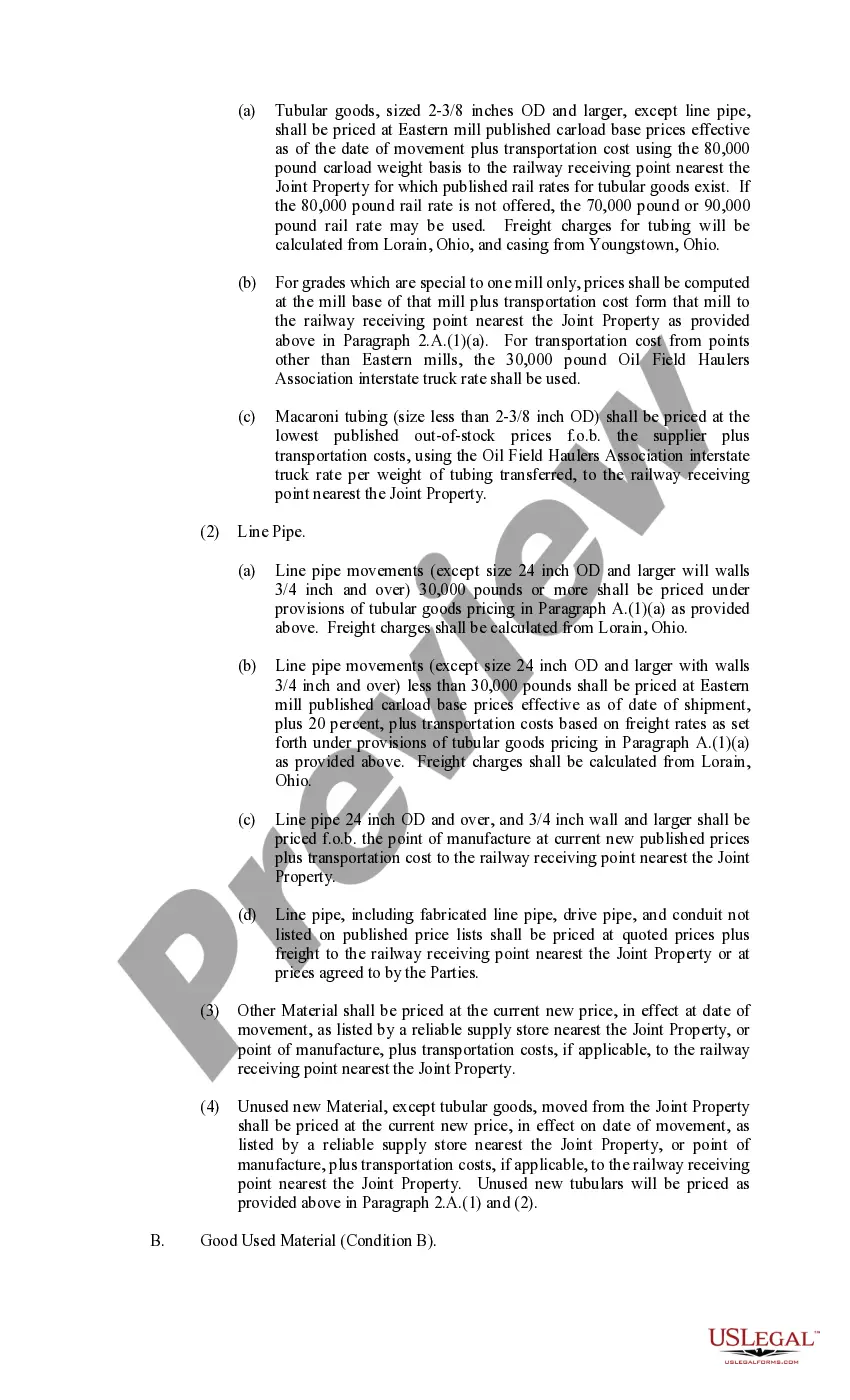

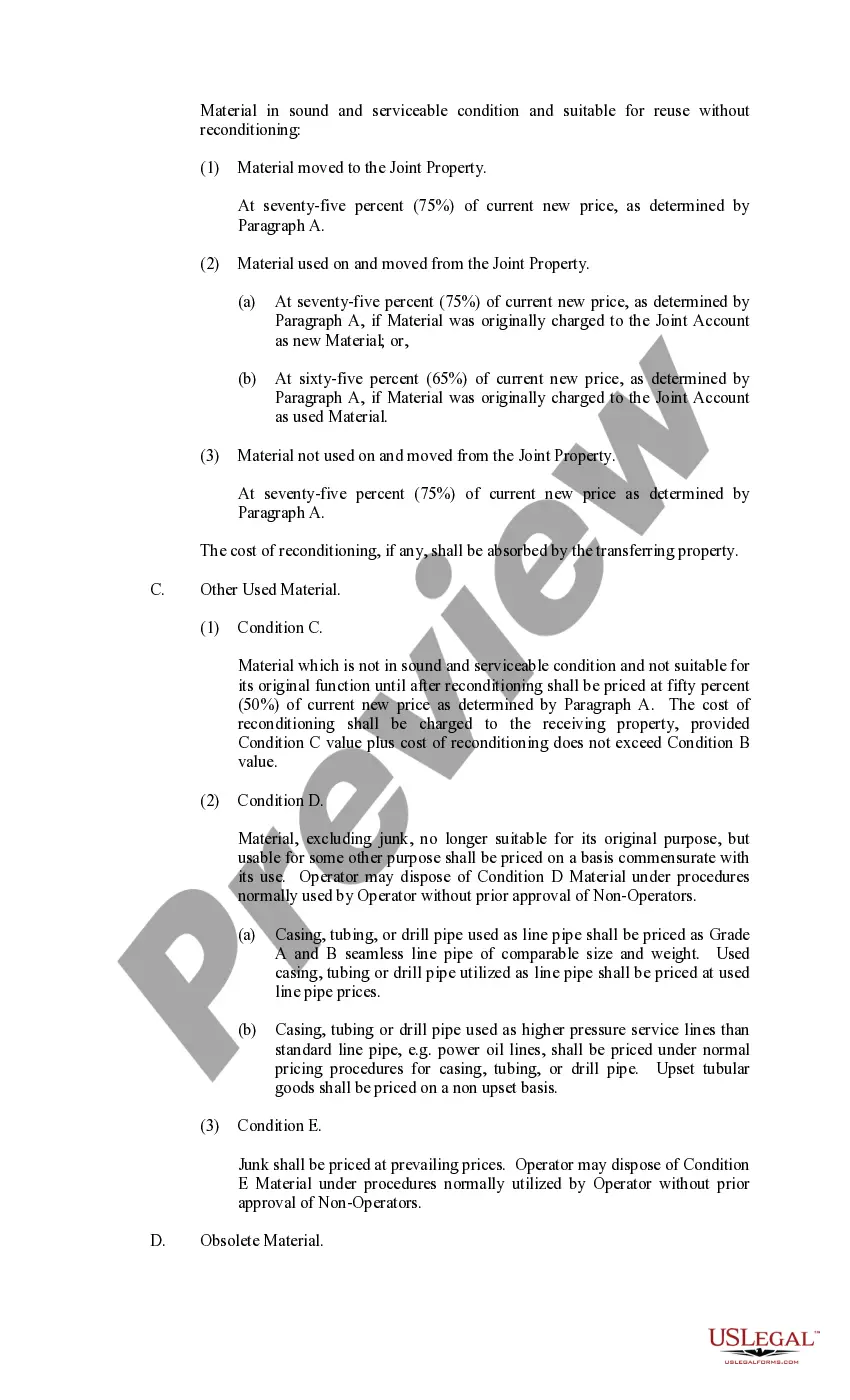

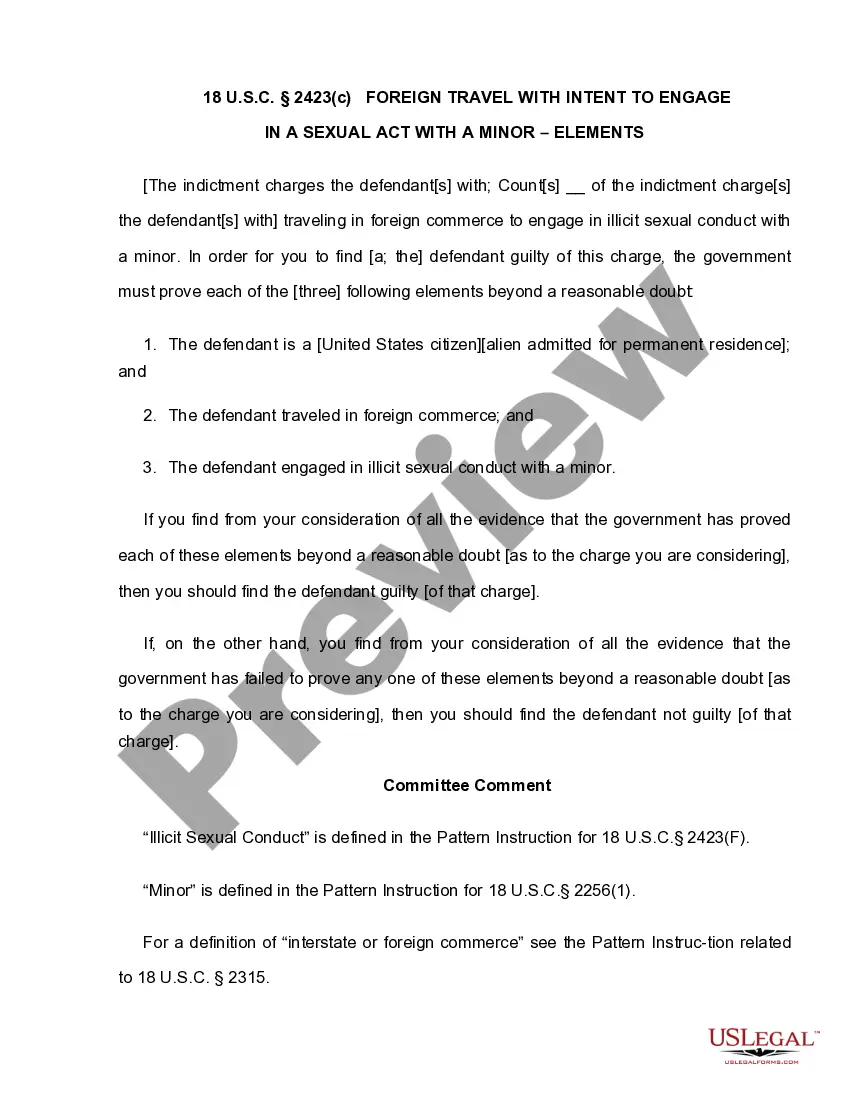

New York Exhibit C Accounting Procedure Joint Operations is a comprehensive guideline that outlines the accounting procedures applicable to joint operations taking place in New York. These procedures ensure accurate financial reporting, efficient cost allocation, and seamless collaboration between multiple parties involved in joint operations. Key components of the New York Exhibit C Accounting Procedure Joint Operations include: 1. Cost Allocation: This section elaborates on the methods and principles used to allocate costs incurred during joint operations among the participating entities. It covers various factors such as working interest percentages, drilling and exploration costs, production costs, and administrative expenses. 2. Revenue Recognition: The New York Exhibit C Accounting Procedure Joint Operations provides guidelines on the recognition and distribution of revenues generated from joint operations. It specifies how revenue should be allocated based on the participating entities' working interests and outlines any special considerations for different types of revenue streams such as sales, royalties, or licensing fees. 3. Financial Reporting: This section highlights the reporting requirements for joint operations and the financial statements that need to be prepared by the participating entities. It includes guidelines on preparing balance sheets, income statements, statement of cash flows, and other relevant financial reports. Additionally, it may touch upon disclosure requirements for commitments, contingent liabilities, and significant accounting policies. 4. Audit and Compliance: The New York Exhibit C Accounting Procedure Joint Operations emphasizes the importance of audits to ensure accuracy and adherence to accounting principles. It may outline the steps and procedures to be followed during audits and provide recommendations for maintaining compliance with applicable regulations. Different types of New York Exhibit C Accounting Procedure Joint Operations may exist depending on the specific industry or sector. Here are a few examples: 1. Oil and Gas Joint Operations: This type of joint operation covers activities related to oil and gas exploration, drilling, production, and revenue distribution. The New York Exhibit C Accounting Procedure for Oil and Gas Joint Operations would provide specific guidelines tailored to this industry's unique characteristics. 2. Mining Joint Operations: In the mining sector, joint operations involve multiple entities collaborating in the extraction and processing of minerals. The New York Exhibit C Accounting Procedure for Mining Joint Operations would address cost allocation methods, mineral reserve accounting, and revenue recognition principles specific to the mining industry. 3. Real Estate Joint Ventures: Real estate joint operations typically involve multiple parties pooling resources to acquire, develop, or manage properties. The New York Exhibit C Accounting Procedure for Real Estate Joint Ventures would focus on aspects such as acquisition costs, construction costs, property valuation, and revenue distribution. It is important to note that the specific names and types of New York Exhibit C Accounting Procedure Joint Operations may vary depending on the governing body or organization responsible for issuing such guidelines.

New York Exhibit C Accounting Procedure Joint Operations

Description

How to fill out New York Exhibit C Accounting Procedure Joint Operations?

US Legal Forms - one of the biggest libraries of authorized varieties in the USA - provides an array of authorized document layouts you can down load or printing. Using the web site, you will get a large number of varieties for business and individual reasons, categorized by types, states, or key phrases.You can get the most recent models of varieties much like the New York Exhibit C Accounting Procedure Joint Operations in seconds.

If you already have a subscription, log in and down load New York Exhibit C Accounting Procedure Joint Operations from the US Legal Forms library. The Acquire option will appear on each develop you view. You have access to all formerly saved varieties from the My Forms tab of your respective accounts.

If you wish to use US Legal Forms the very first time, allow me to share straightforward directions to get you started out:

- Make sure you have selected the proper develop for your city/area. Select the Preview option to examine the form`s information. See the develop description to ensure that you have selected the correct develop.

- When the develop does not match your demands, take advantage of the Lookup area near the top of the display to find the one that does.

- If you are satisfied with the shape, affirm your decision by clicking the Acquire now option. Then, select the rates prepare you like and provide your accreditations to register for an accounts.

- Method the purchase. Make use of credit card or PayPal accounts to finish the purchase.

- Pick the file format and down load the shape on the system.

- Make adjustments. Load, edit and printing and indicator the saved New York Exhibit C Accounting Procedure Joint Operations.

Every web template you put into your money lacks an expiration date and is yours permanently. So, if you would like down load or printing another duplicate, just check out the My Forms segment and click around the develop you require.

Get access to the New York Exhibit C Accounting Procedure Joint Operations with US Legal Forms, one of the most substantial library of authorized document layouts. Use a large number of expert and condition-specific layouts that meet your organization or individual demands and demands.