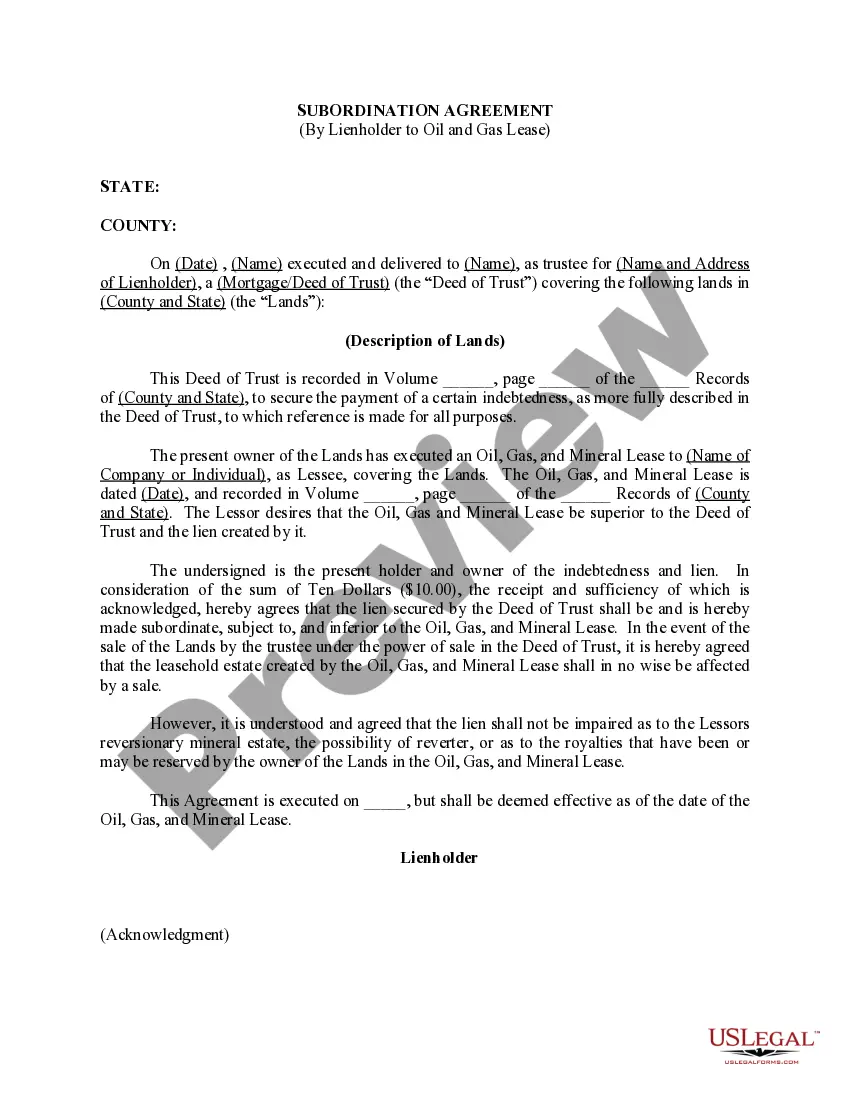

New York Subordination Agreement (Deed of Trust)

Description

How to fill out Subordination Agreement (Deed Of Trust)?

If you want to complete, down load, or printing lawful document templates, use US Legal Forms, the most important variety of lawful varieties, which can be found on the web. Use the site`s basic and practical search to discover the files you need. Numerous templates for enterprise and personal functions are sorted by types and states, or search phrases. Use US Legal Forms to discover the New York Subordination Agreement (Deed of Trust) within a handful of clicks.

Should you be presently a US Legal Forms client, log in to the bank account and then click the Acquire option to get the New York Subordination Agreement (Deed of Trust). You can also accessibility varieties you earlier saved inside the My Forms tab of your respective bank account.

Should you use US Legal Forms for the first time, refer to the instructions below:

- Step 1. Ensure you have selected the shape for the correct metropolis/region.

- Step 2. Use the Preview method to look over the form`s articles. Never forget to read through the description.

- Step 3. Should you be not satisfied using the develop, make use of the Lookup area towards the top of the screen to get other types of your lawful develop design.

- Step 4. When you have found the shape you need, click on the Acquire now option. Opt for the prices plan you choose and put your credentials to sign up for an bank account.

- Step 5. Procedure the financial transaction. You should use your credit card or PayPal bank account to finish the financial transaction.

- Step 6. Choose the structure of your lawful develop and down load it on your gadget.

- Step 7. Complete, change and printing or signal the New York Subordination Agreement (Deed of Trust).

Each lawful document design you get is your own property forever. You have acces to each develop you saved within your acccount. Click on the My Forms portion and select a develop to printing or down load once again.

Compete and down load, and printing the New York Subordination Agreement (Deed of Trust) with US Legal Forms. There are thousands of professional and status-distinct varieties you may use for your enterprise or personal requires.

Form popularity

FAQ

A subordination clause is a clause in an agreement that states that the current claim on any debts will take priority over any other claims formed in other agreements made in the future.

Since it's recorded after any HELOCs or second mortgages you already have in place, the first mortgage would naturally take a lower lien position. Most lenders won't allow this, so this could cause you to lose your loan approval if the second mortgage holder won't agree to subordinate.

A subordinate clause is a clause that cannot stand alone as a complete sentence; it merely complements a sentence's main clause, thereby adding to the whole unit of meaning. Because a subordinate clause is dependent upon a main clause to be meaningful, it is also referred to as a dependent clause.

Definition and Example of a Subordination Clause For instance, say you buy a home with a mortgage. Later, you add a home equity line of credit (HELOC). Due to a subordination clause likely located in your original mortgage contract, your first mortgage ranks as the first priority or lien.

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.

The Subordinated Lender hereby agrees that all Subordinated Obligations (as defined below) and all of his right, title and interest in and to the Subordinated Obligations shall be subordinate and junior in right of payment to the Senior Lender Loan and all rights of Senior Lender in respect of the Senior Lender Loan, ...

Understanding Subordination Clauses When you get a mortgage loan, the lender will likely include a subordination clause essentially stating that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender if a homeowner defaults.

The creditor usually will require the debtor to sign a subordination agreement which ensures they get paid before other creditors, ensuring they are not taking on high risks.

")