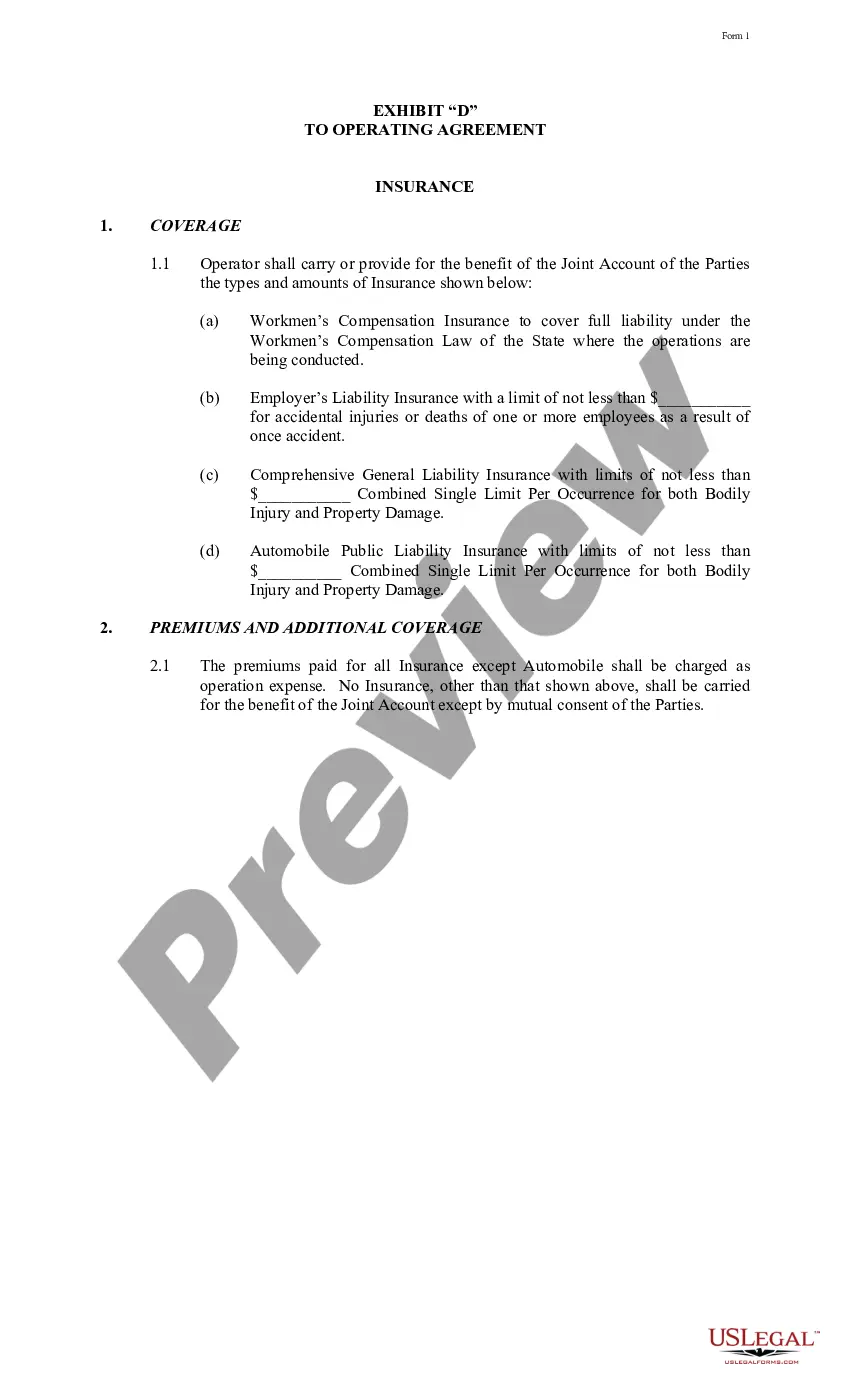

New York Exhibit D to Operating Agreement Insurance — Form 1 is a document that outlines the insurance requirements and provisions for a company operating in the state of New York. This exhibit is typically attached to the operating agreement of a business entity and serves as a comprehensive guide for insurance coverage and obligations. The New York Exhibit D to Operating Agreement Insurance — Form 1 specifies the types of insurance policies that a company must obtain to protect its assets, employees, stakeholders, and other parties involved. It sets forth the minimum coverage limits, terms, and conditions necessary to comply with the legal requirements and mitigate risks effectively. Furthermore, it may also include additional optional coverage types that can provide enhanced protection based on the specific needs of the business. There are several types of insurance that may be included in the New York Exhibit D to Operating Agreement Insurance — Form 1. These may include: 1. General Liability Insurance: This coverage protects the company against claims arising from bodily injury, property damage, or personal injury caused by the company's operations or products. 2. Property Insurance: This type of insurance is designed to cover damage or loss of the company's physical assets, such as buildings, equipment, inventory, and furniture, due to fire, theft, vandalism, or other covered perils. 3. Workers' Compensation Insurance: A crucial coverage required by New York state law, workers' compensation provides benefits to employees who suffer work-related injuries or illnesses. It covers medical expenses, rehabilitation costs, and lost wages during the recovery period. 4. Professional Liability Insurance: Also known as Errors and Omissions (E&O) insurance, this coverage safeguards the company against claims of negligence, errors, or omissions that result in financial losses for clients or third parties. It is particularly crucial for service-based businesses, such as consultants, lawyers, and accountants. 5. Commercial Auto Insurance: If the company owns or uses vehicles for business purposes, this insurance protects against liability for accidents, property damage, and injuries involving those vehicles. 6. Cyber Liability Insurance: In today's digital age, businesses face significant risks related to data breaches, cyberattacks, and privacy violations. Cyber liability insurance provides coverage for expenses incurred due to cyber incidents, including legal fees, customer notification, credit monitoring, and public relations efforts. These are just a few examples of the different types of insurance that might be included in the New York Exhibit D to Operating Agreement Insurance — Form 1. It's essential for businesses to carefully review this exhibit to ensure compliance with legal requirements and adequately protect themselves against potential risks. Additionally, specific industry-related risks may require additional insurance coverage not mentioned here, so it's important to consult with an experienced insurance professional or attorney to tailor the exhibit to the unique needs of the business.

New York Exhibit D to Operating Agreement Insurance - Form 1

Description

How to fill out New York Exhibit D To Operating Agreement Insurance - Form 1?

If you need to full, obtain, or print out authorized record themes, use US Legal Forms, the biggest collection of authorized kinds, that can be found on the Internet. Use the site`s easy and hassle-free research to find the paperwork you will need. Various themes for company and specific uses are categorized by groups and suggests, or search phrases. Use US Legal Forms to find the New York Exhibit D to Operating Agreement Insurance - Form 1 within a couple of clicks.

If you are presently a US Legal Forms client, log in to your bank account and click on the Download key to find the New York Exhibit D to Operating Agreement Insurance - Form 1. You can also entry kinds you in the past downloaded in the My Forms tab of the bank account.

If you use US Legal Forms initially, refer to the instructions below:

- Step 1. Ensure you have chosen the shape for that right town/land.

- Step 2. Utilize the Preview option to look over the form`s content. Don`t neglect to see the outline.

- Step 3. If you are not happy using the form, take advantage of the Lookup area at the top of the display screen to find other models in the authorized form web template.

- Step 4. When you have identified the shape you will need, select the Purchase now key. Choose the pricing strategy you like and put your accreditations to sign up to have an bank account.

- Step 5. Method the transaction. You may use your credit card or PayPal bank account to accomplish the transaction.

- Step 6. Pick the formatting in the authorized form and obtain it on your system.

- Step 7. Comprehensive, edit and print out or sign the New York Exhibit D to Operating Agreement Insurance - Form 1.

Every single authorized record web template you purchase is your own for a long time. You have acces to every single form you downloaded with your acccount. Select the My Forms portion and decide on a form to print out or obtain once again.

Be competitive and obtain, and print out the New York Exhibit D to Operating Agreement Insurance - Form 1 with US Legal Forms. There are millions of professional and express-specific kinds you may use to your company or specific needs.