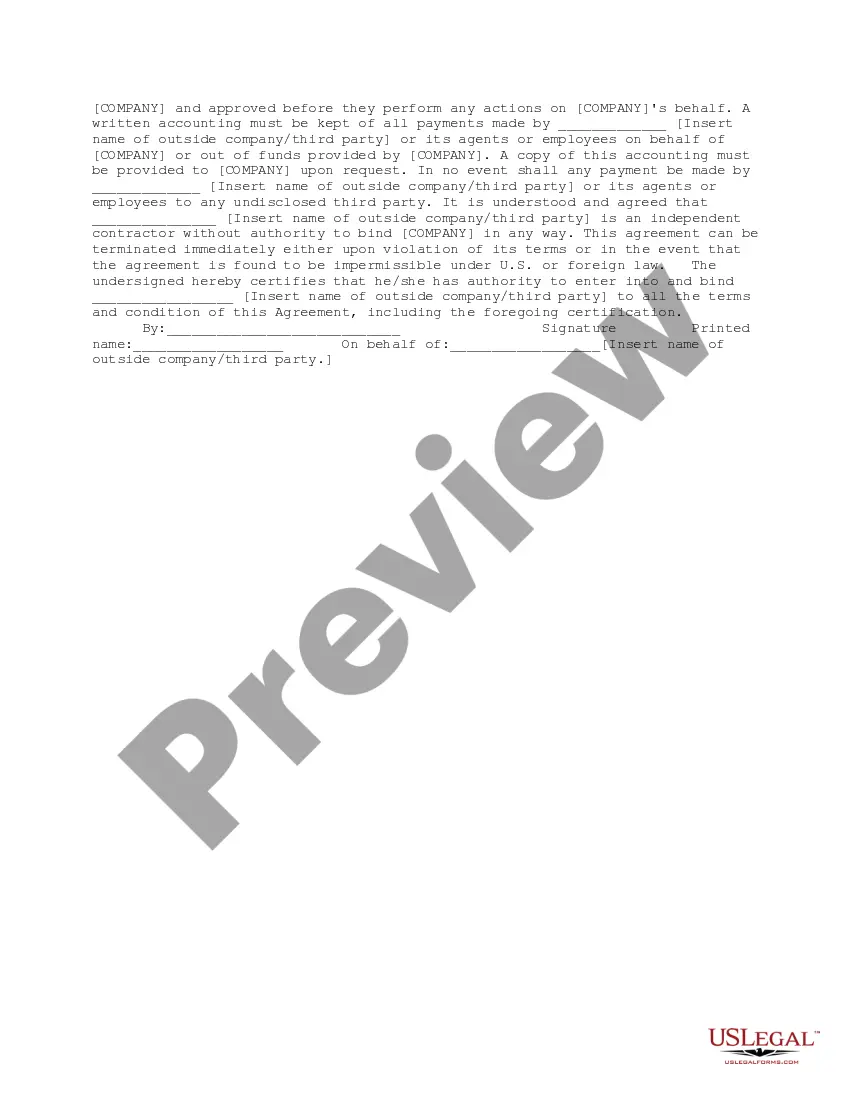

This is a corporate policy document designed to meet the standards of the Foreign Corrupt Practices Act, a provision of the Securities and Exchange Act of 1934. FCPA generally prohibits payments by companies and their representatives to foreign (i.e., non-U.S.) government and quasi-government officials to secure business.

The New York Foreign Corrupt Practices Act (CPA) is a significant legislation that prohibits U.S. entities, including corporations, from engaging in corrupt practices while conducting business abroad. This act aims to maintain fair and ethical business practices globally and encourages transparency in all international transactions. The New York CPA consists of various corporate policies that organizations must adapt to comply with the law and prevent corruption. These policies outline the necessary steps, procedures, and measures companies must implement to deter bribery, kickbacks, and other corrupt activities. Here are different types or components of the New York Foreign Corrupt Practices Act — Corporate Policy: 1. Anti-Bribery Policy: This policy establishes guidelines to prevent bribery by employees, agents, and third parties working on behalf of the organization. It defines what constitutes a bribe, the penalties for noncompliance, and the responsibilities of all company personnel. 2. Due Diligence Policy: This policy ensures that companies conduct thorough due diligence on potential business partners, suppliers, and intermediaries to identify any potential red flags or risks associated with corruption. It sets protocols for assessing the integrity and reputation of individuals or organizations before entering into business relationships. 3. Internal Controls Policy: This policy focuses on creating a robust internal control system to detect and prevent corruption within the organization. It includes procedures for properly documenting transactions, financial reporting, and monitoring compliance with anti-corruption laws. 4. Gifts, Entertainment, and Hospitality Policy: This policy establishes guidelines for offering or accepting gifts, entertainment, or hospitality to prevent inappropriate influences or perceived bribery. It defines acceptable limits, reporting requirements, and ensures transparency in such interactions. 5. Reporting and Whistleblower Policy: This policy encourages employees to report any suspected or actual corrupt practices without fear of retaliation. It outlines the channels through which employees can report concerns and ensures anonymity and protection for whistleblowers. 6. Training and Awareness Policy: This policy emphasizes the importance of educating employees and relevant stakeholders about the New York CPA and the organization's anti-corruption policies. It includes training programs, workshops, and awareness campaigns to promote understanding and compliance. Companies should tailor their New York Foreign Corrupt Practices Act — Corporate Policy to suit their specific organizational structure, industry, and risk profile. By implementing comprehensive anti-corruption policies, organizations can mitigate legal risks, foster a culture of integrity, and foster sustainable business relationships globally.The New York Foreign Corrupt Practices Act (CPA) is a significant legislation that prohibits U.S. entities, including corporations, from engaging in corrupt practices while conducting business abroad. This act aims to maintain fair and ethical business practices globally and encourages transparency in all international transactions. The New York CPA consists of various corporate policies that organizations must adapt to comply with the law and prevent corruption. These policies outline the necessary steps, procedures, and measures companies must implement to deter bribery, kickbacks, and other corrupt activities. Here are different types or components of the New York Foreign Corrupt Practices Act — Corporate Policy: 1. Anti-Bribery Policy: This policy establishes guidelines to prevent bribery by employees, agents, and third parties working on behalf of the organization. It defines what constitutes a bribe, the penalties for noncompliance, and the responsibilities of all company personnel. 2. Due Diligence Policy: This policy ensures that companies conduct thorough due diligence on potential business partners, suppliers, and intermediaries to identify any potential red flags or risks associated with corruption. It sets protocols for assessing the integrity and reputation of individuals or organizations before entering into business relationships. 3. Internal Controls Policy: This policy focuses on creating a robust internal control system to detect and prevent corruption within the organization. It includes procedures for properly documenting transactions, financial reporting, and monitoring compliance with anti-corruption laws. 4. Gifts, Entertainment, and Hospitality Policy: This policy establishes guidelines for offering or accepting gifts, entertainment, or hospitality to prevent inappropriate influences or perceived bribery. It defines acceptable limits, reporting requirements, and ensures transparency in such interactions. 5. Reporting and Whistleblower Policy: This policy encourages employees to report any suspected or actual corrupt practices without fear of retaliation. It outlines the channels through which employees can report concerns and ensures anonymity and protection for whistleblowers. 6. Training and Awareness Policy: This policy emphasizes the importance of educating employees and relevant stakeholders about the New York CPA and the organization's anti-corruption policies. It includes training programs, workshops, and awareness campaigns to promote understanding and compliance. Companies should tailor their New York Foreign Corrupt Practices Act — Corporate Policy to suit their specific organizational structure, industry, and risk profile. By implementing comprehensive anti-corruption policies, organizations can mitigate legal risks, foster a culture of integrity, and foster sustainable business relationships globally.