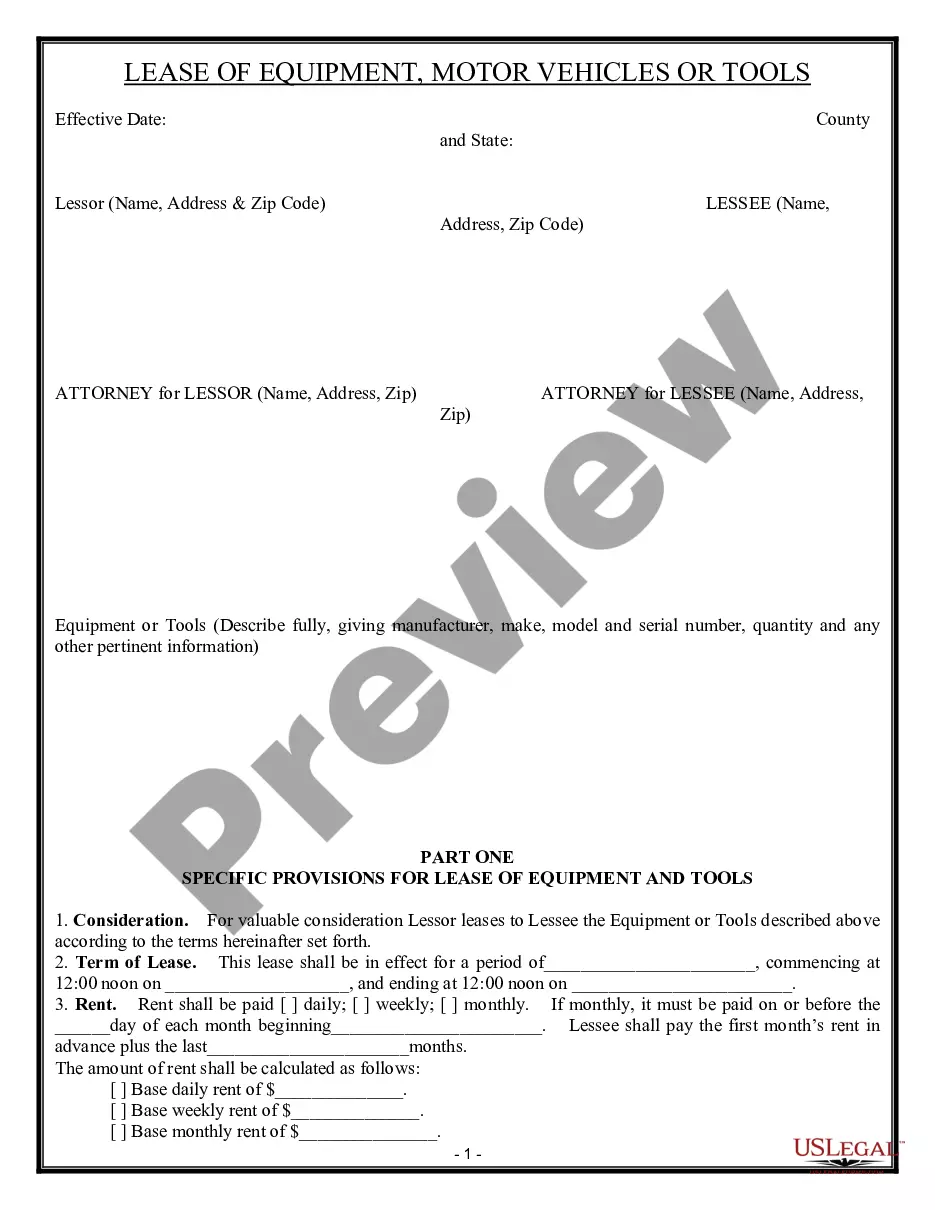

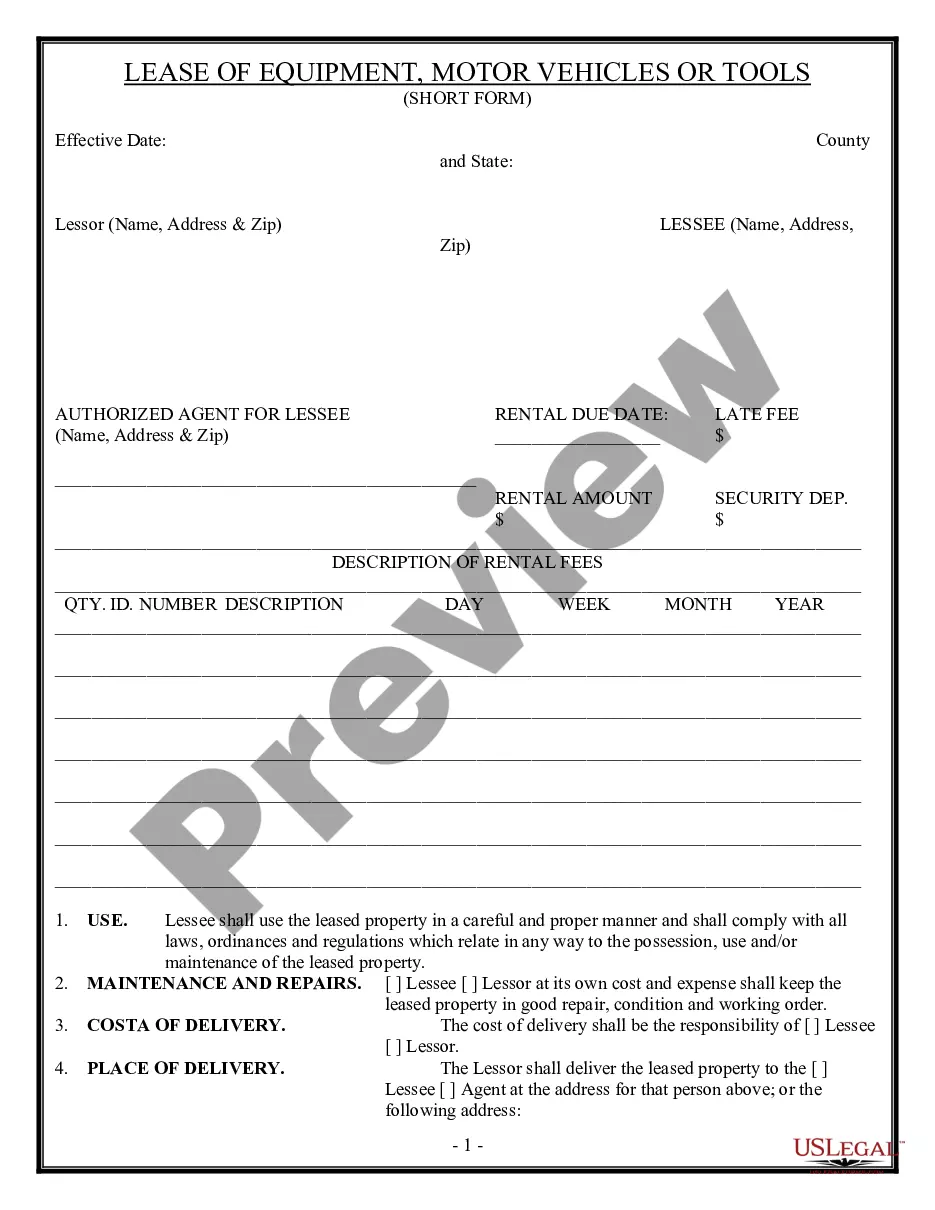

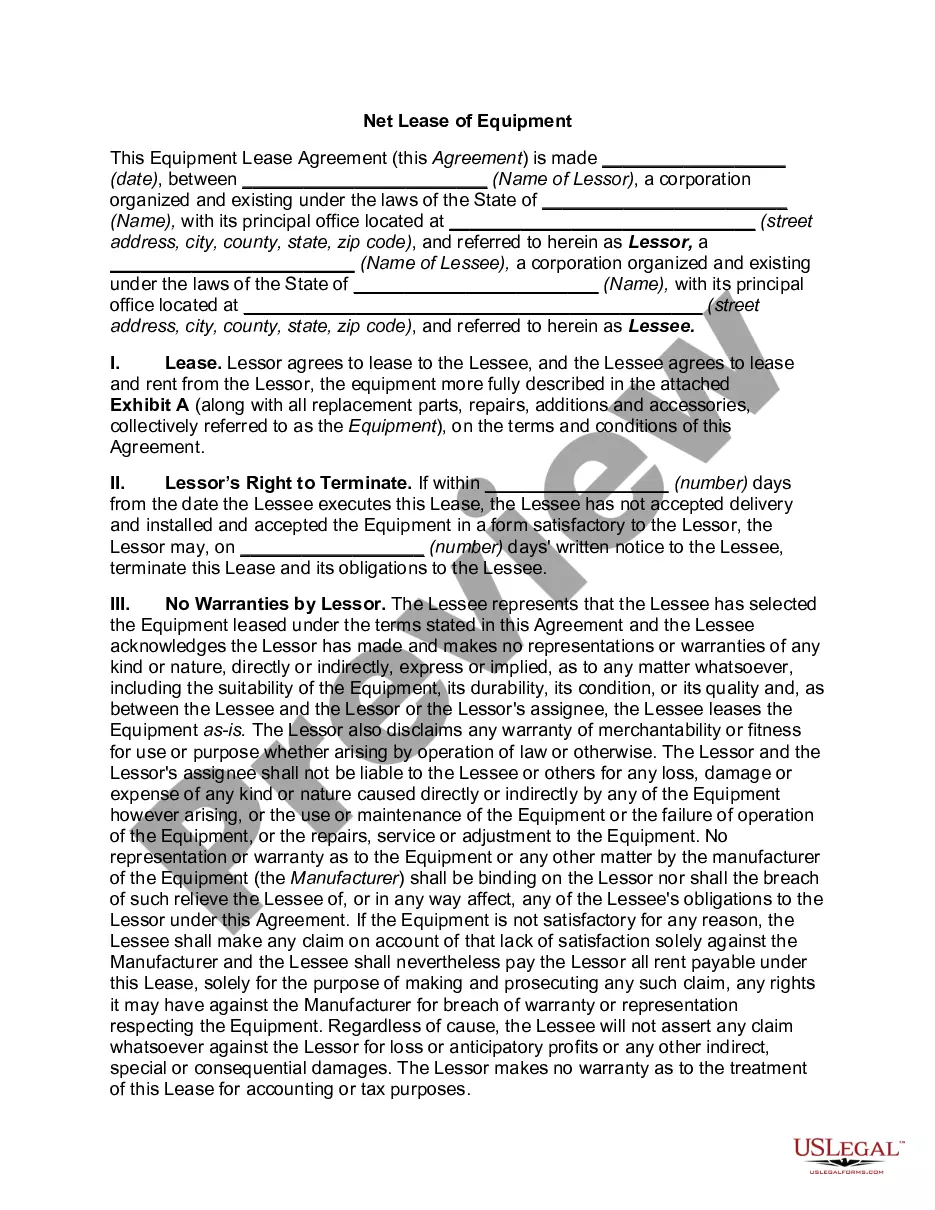

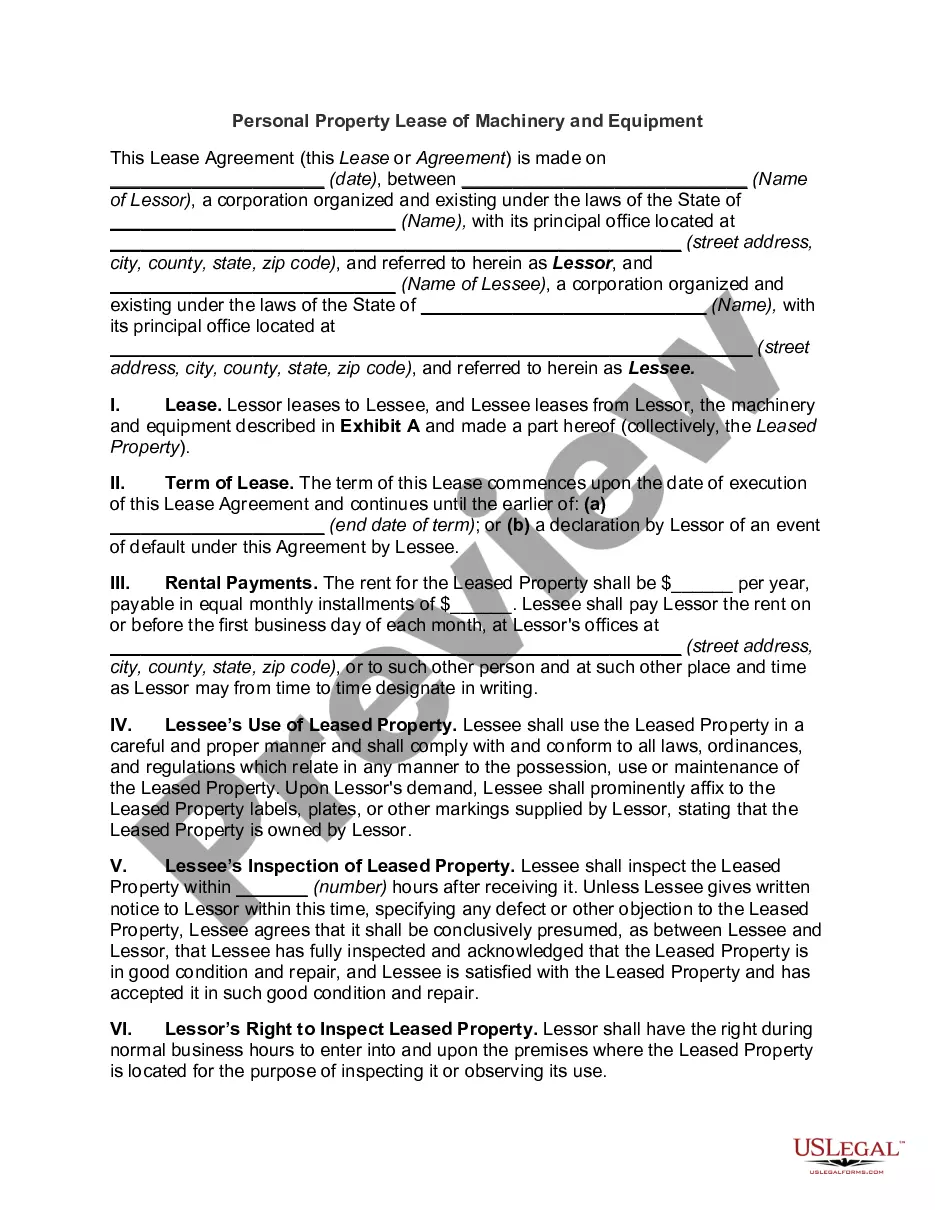

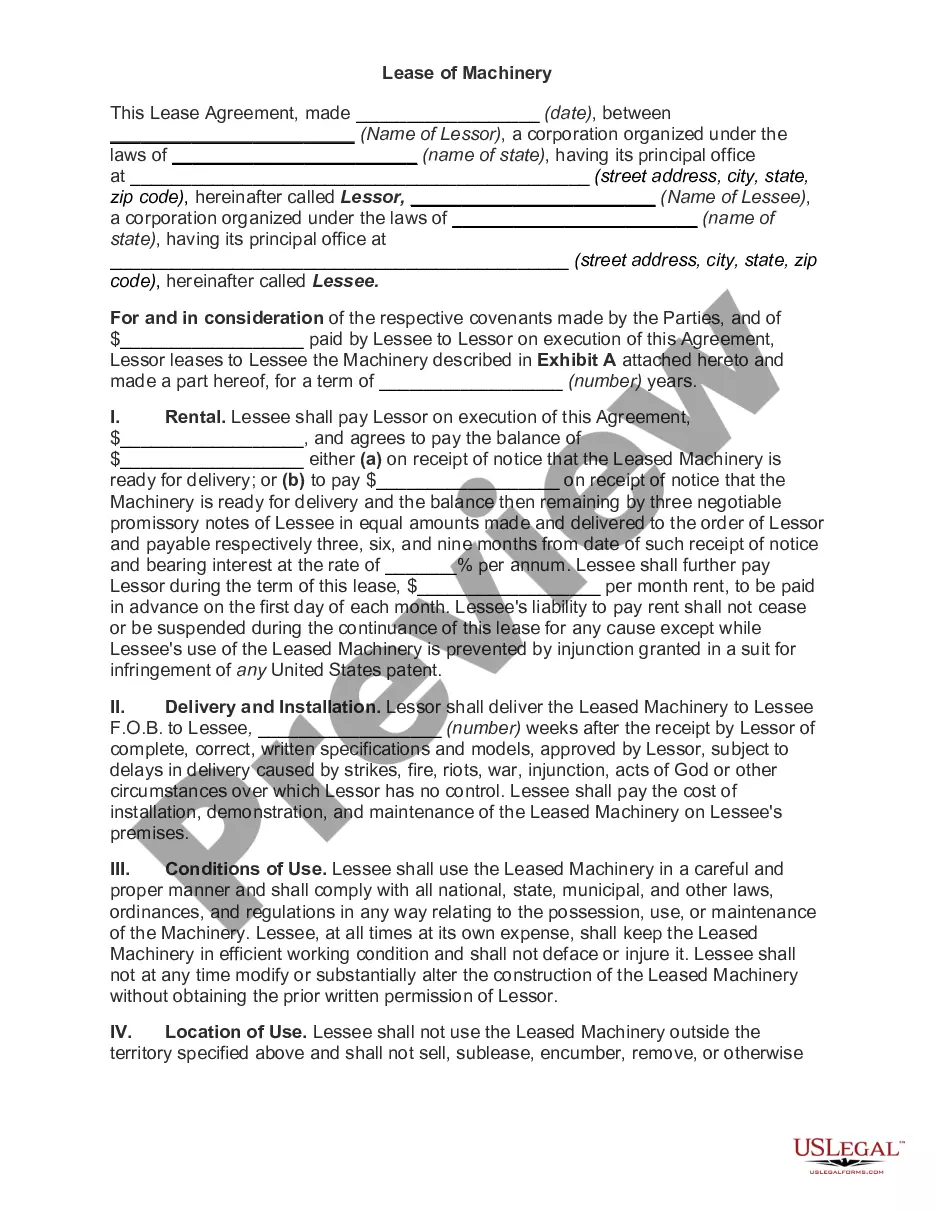

This form is an Equipment Lease. The lessor and lessee have entered into a contract for the renting of machinery and equipment. The contract also provides that the lessee may use the leased property at the location specified in the agreement. The contract is conditioned upon a landlord's waiver being executed.

Ohio Equipment Lease - General

Instant download

Description

Free preview

How to fill out Equipment Lease - General?

Finding the appropriate legal document template can be quite a challenge.

Clearly, there are numerous templates accessible online, but how can you locate the legal document you need.

Make use of the US Legal Forms website.

If you are a new user of US Legal Forms, here are simple guidelines to follow: First, ensure you have selected the correct form for your city/state. You can view the form using the Preview button and read the form description to ensure it is suitable for you.

- This service offers a multitude of templates, such as the Ohio Equipment Lease - General, that can be utilized for both business and personal purposes.

- All forms are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Download button to obtain the Ohio Equipment Lease - General.

- Use your account to search through the legal forms you have previously purchased.

- Go to the My documents tab in your account to get another copy of the document you need.

Form popularity

FAQ

To record an equipment lease in accounting, start by determining the present value of the lease payments. This amount is then debited to an asset account and credited to a lease liability account. As part of managing your Ohio Equipment Lease - General, use tools like US Legal Forms to simplify this process and ensure accurate documentation.

In accounting, a lease is recorded by recognizing the leased asset and its corresponding liability on your balance sheet. This is essential for reflecting the true financial position of your company. For an Ohio Equipment Lease - General, you will create separate accounts for the asset and liability to ensure clarity and compliance with accounting standards.

A journal entry for an Ohio Equipment Lease - General typically involves recording the asset and liability. When the lease begins, you will debit the equipment account to recognize the asset and credit a lease liability account. This process reflects your obligation to make future lease payments, maintaining accurate records for financial reporting.

To depreciate leased equipment under an Ohio Equipment Lease - General, you first need to determine if the lease qualifies as an operating lease or a capital lease. For an operating lease, you typically do not depreciate the equipment; instead, you recognize lease payments as an expense. If it’s a capital lease, you can depreciate the leased asset over its useful life. Utilizing resources like US Legal Forms can help you navigate the complexities of lease agreements and ensure you manage depreciation correctly.

Certain items are exempt from sales tax in Ohio, including many goods used in manufacturing and equipment sold to a qualifying business. Specifically, items purchased for resale are typically tax-exempt. When entering into an Ohio Equipment Lease - General, understanding these exemptions can benefit your finances. Using the US Legal Forms platform can help you navigate these regulations effectively.

In Ohio, the taxation of material handling equipment depends on specific circumstances, particularly regarding its use. Generally, if the equipment is used in manufacturing or for resale, it can be exempt from sales tax. If you are leasing material handling equipment under an Ohio Equipment Lease - General agreement, consider understanding the tax implications. For personalized advice, consult a tax professional or explore the resources available on the US Legal Forms platform.

To record a lease on equipment, start by ensuring that you have a written lease agreement that complies with Ohio regulations. You should then document the lease in your financial records, indicating the equipment and the terms of the lease. Keeping accurate records can help you track depreciation and tax deductions associated with your Ohio Equipment Lease - General.

Filling out an Ohio residential lease agreement involves providing essential details like tenant and landlord information, rent amount, and duration of the lease. Be sure to include rules about security deposits and maintenance responsibilities. US Legal Forms offers easy-to-use templates that guide you through the process, ensuring that all crucial elements are covered.

Creating an equipment rental agreement requires you to specify the equipment details, rental duration, and payment terms. You should clearly outline the responsibilities regarding maintenance and liability for damages. Using platforms like US Legal Forms can help you find templates and guides to ensure that your equipment rental agreement complies with Ohio law.

To set up an Ohio Equipment Lease - General, begin by identifying the equipment you want to lease. Next, determine the lease term and payment structure, then draft a lease agreement that outlines the responsibilities of both parties. It is important to include details such as maintenance, insurance, and termination conditions to ensure clarity and protect your interests.