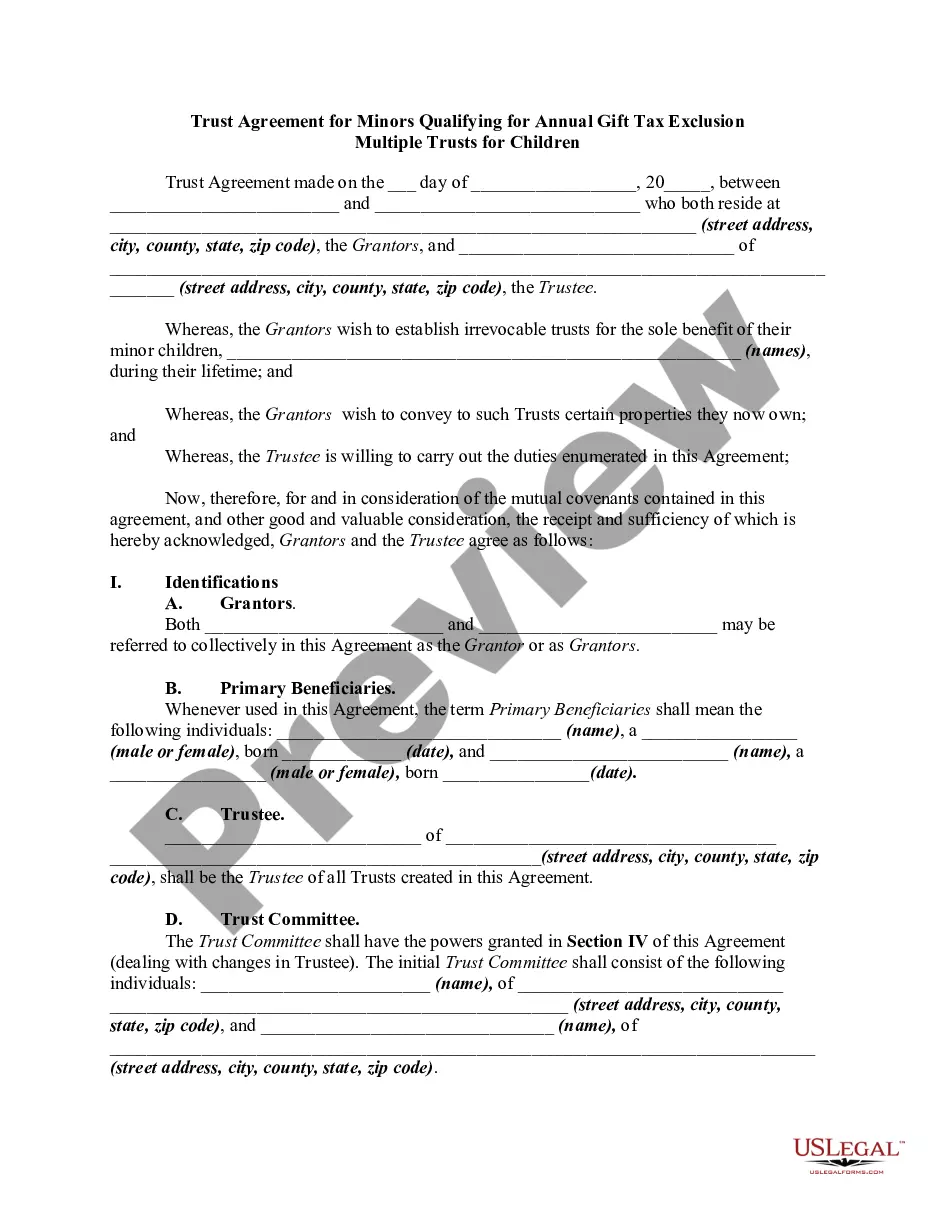

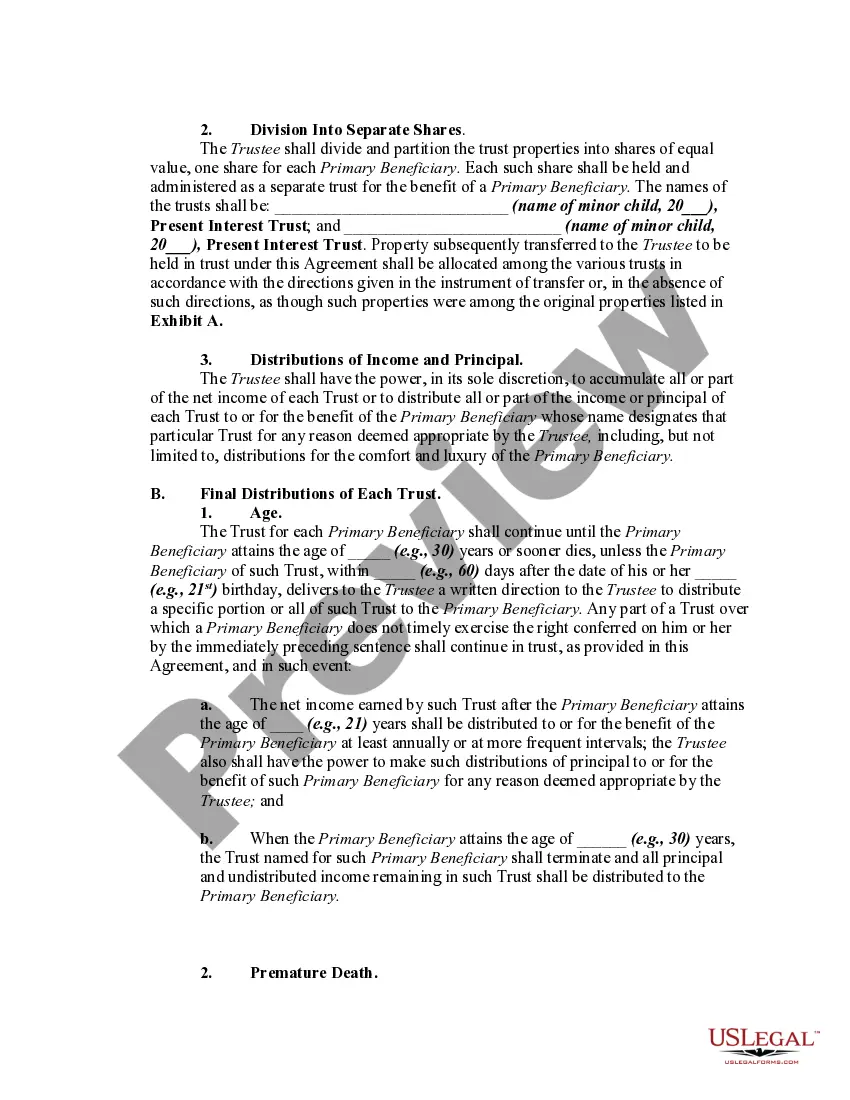

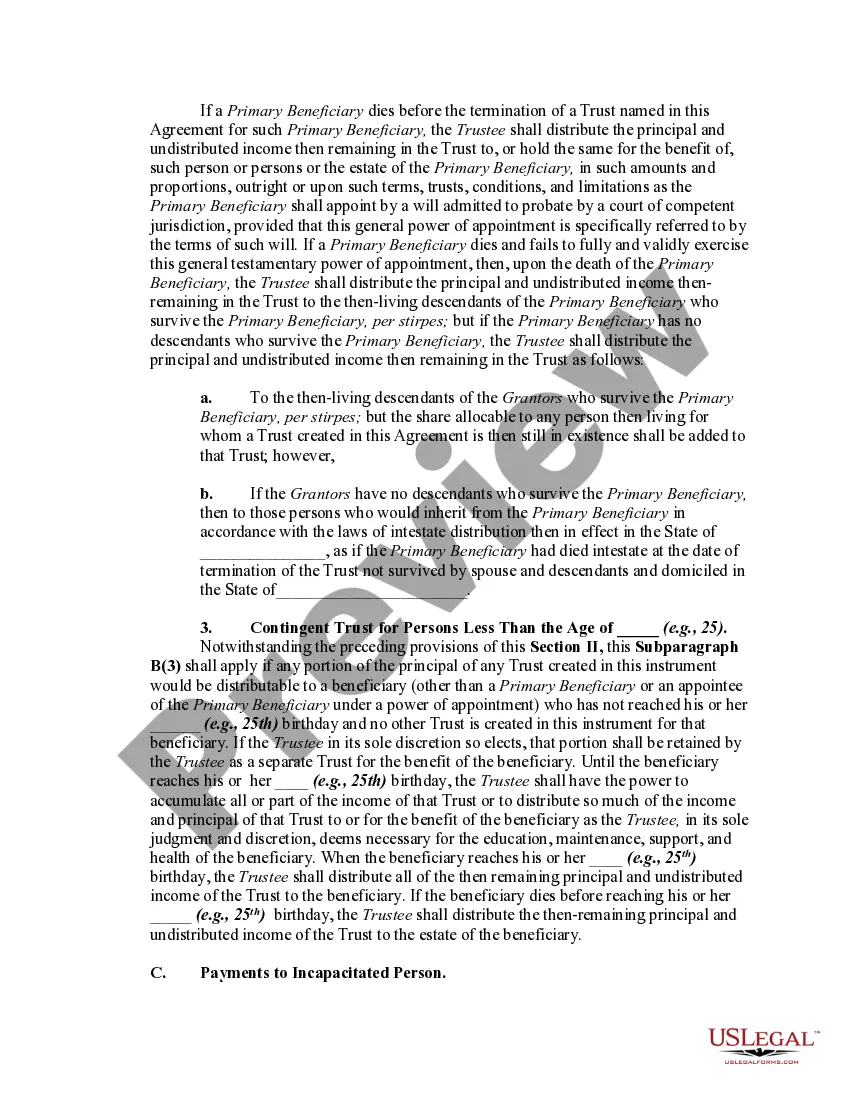

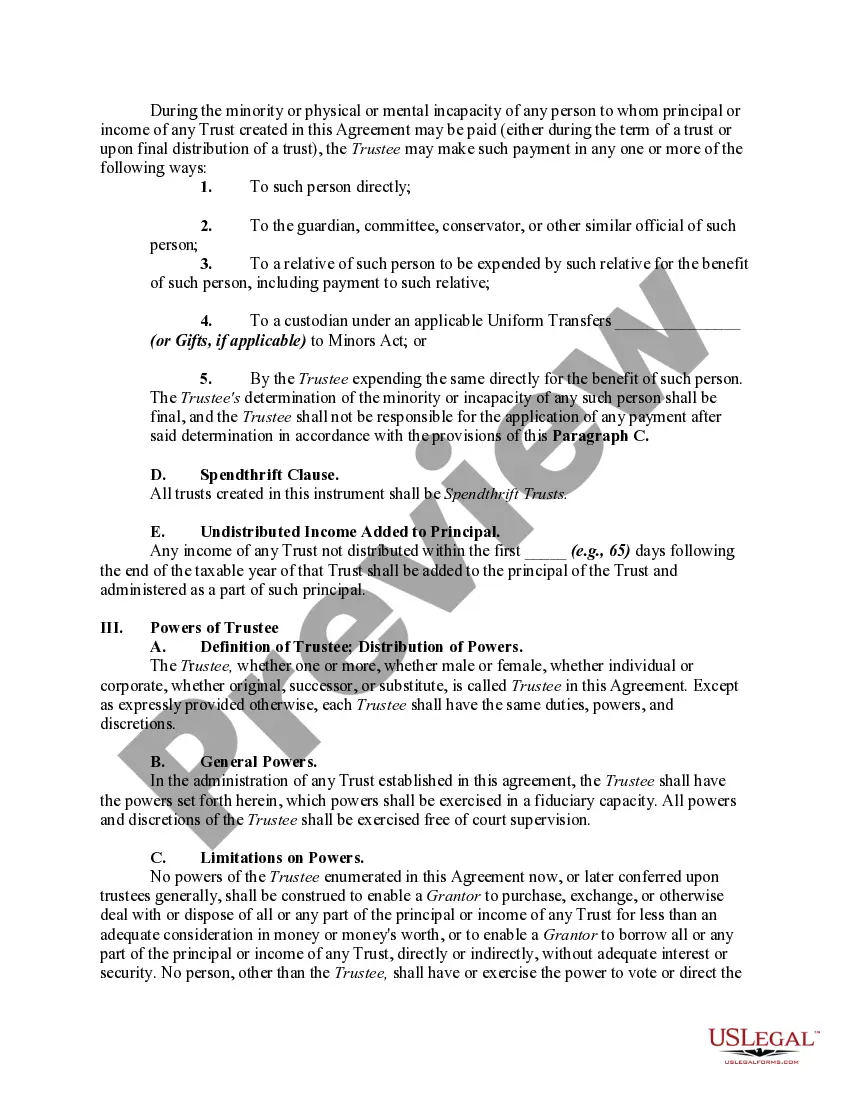

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

The Ohio Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion allows individuals to set up multiple trusts for children that qualify for the annual gift tax exclusion. This legal document ensures that the assets contributed to the trusts are protected and managed responsibly on behalf of the minors until they come of age. With this trust agreement, parents or guardians can create separate trusts for each child, ensuring that their financial needs are addressed individually. This approach allows for customized management of assets and simplifies the distribution process when each child attains the specified age. There are different types of Ohio Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children based on various factors such as distribution age, investment strategy, and purpose: 1. Testamentary Trust for Minors: This trust is established through a will and comes into effect after the granter's death. It ensures that the assets are managed for the child's benefit until they reach a specific age or milestone designated by the granter. 2. Revocable Living Trust for Minors: Created during the granter's lifetime, this trust allows for more flexibility and can be amended or revoked as circumstances change. It offers the granter control over the assets while providing for the child's needs until they come of age. 3. Irrevocable Trust for Minors: This type of trust cannot be modified or terminated once established, but it offers significant tax advantages. It helps protect assets from estate taxes and creditors while allowing for income generation and management for the minors. 4. 529 College Savings Trust for Minors: This specialized trust focuses on funding education expenses by investing in a 529 college savings plan. The granter can contribute a portion of the gift tax exclusion annually, and the funds grow tax-free until used for qualifying education expenses. Ohio's Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children provides important safeguards and guidelines for trustees appointed to manage and distribute the trust assets in the best interests of the minors. It ensures transparency and accountability, allowing parents or guardians to secure their children's financial future while minimizing potential tax burdens.The Ohio Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion allows individuals to set up multiple trusts for children that qualify for the annual gift tax exclusion. This legal document ensures that the assets contributed to the trusts are protected and managed responsibly on behalf of the minors until they come of age. With this trust agreement, parents or guardians can create separate trusts for each child, ensuring that their financial needs are addressed individually. This approach allows for customized management of assets and simplifies the distribution process when each child attains the specified age. There are different types of Ohio Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children based on various factors such as distribution age, investment strategy, and purpose: 1. Testamentary Trust for Minors: This trust is established through a will and comes into effect after the granter's death. It ensures that the assets are managed for the child's benefit until they reach a specific age or milestone designated by the granter. 2. Revocable Living Trust for Minors: Created during the granter's lifetime, this trust allows for more flexibility and can be amended or revoked as circumstances change. It offers the granter control over the assets while providing for the child's needs until they come of age. 3. Irrevocable Trust for Minors: This type of trust cannot be modified or terminated once established, but it offers significant tax advantages. It helps protect assets from estate taxes and creditors while allowing for income generation and management for the minors. 4. 529 College Savings Trust for Minors: This specialized trust focuses on funding education expenses by investing in a 529 college savings plan. The granter can contribute a portion of the gift tax exclusion annually, and the funds grow tax-free until used for qualifying education expenses. Ohio's Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children provides important safeguards and guidelines for trustees appointed to manage and distribute the trust assets in the best interests of the minors. It ensures transparency and accountability, allowing parents or guardians to secure their children's financial future while minimizing potential tax burdens.