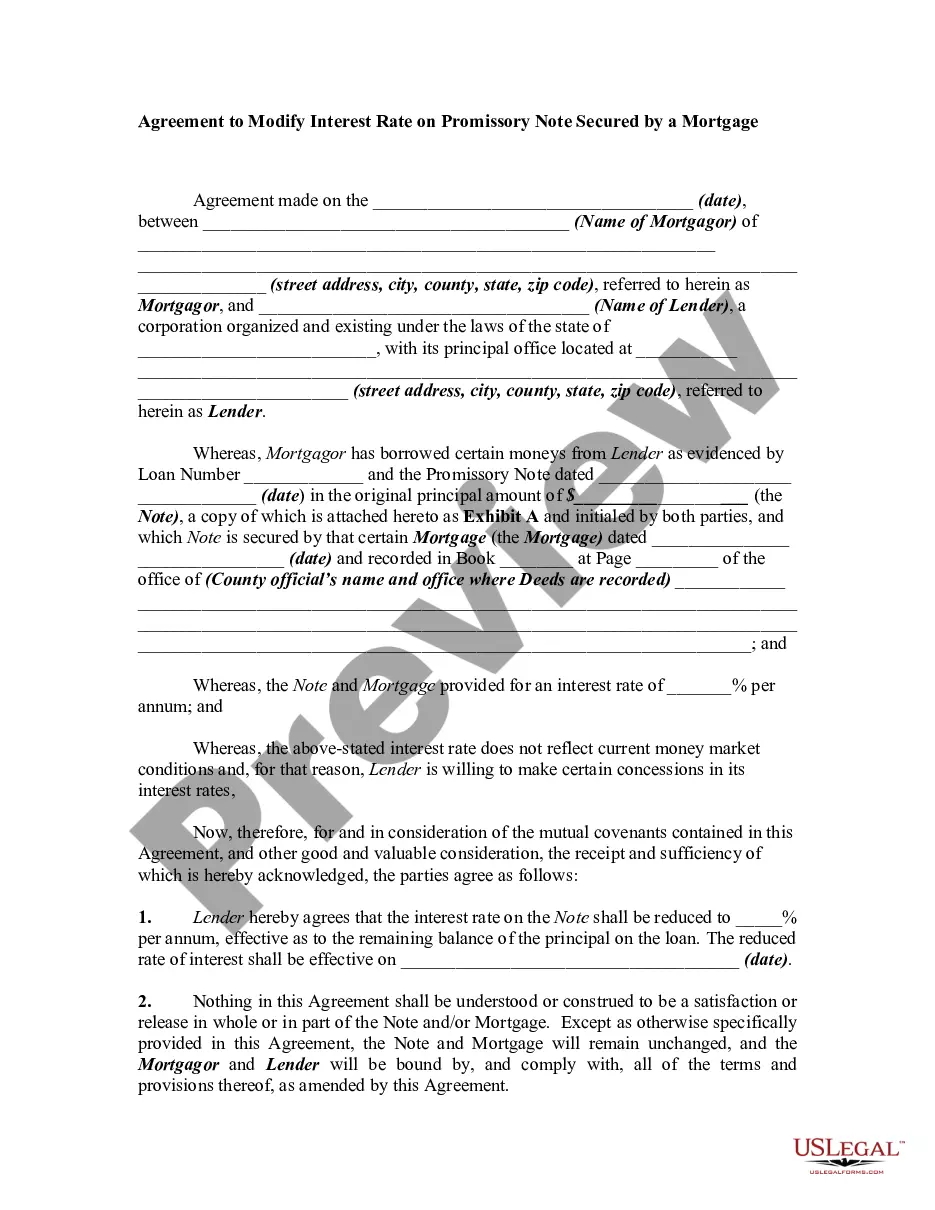

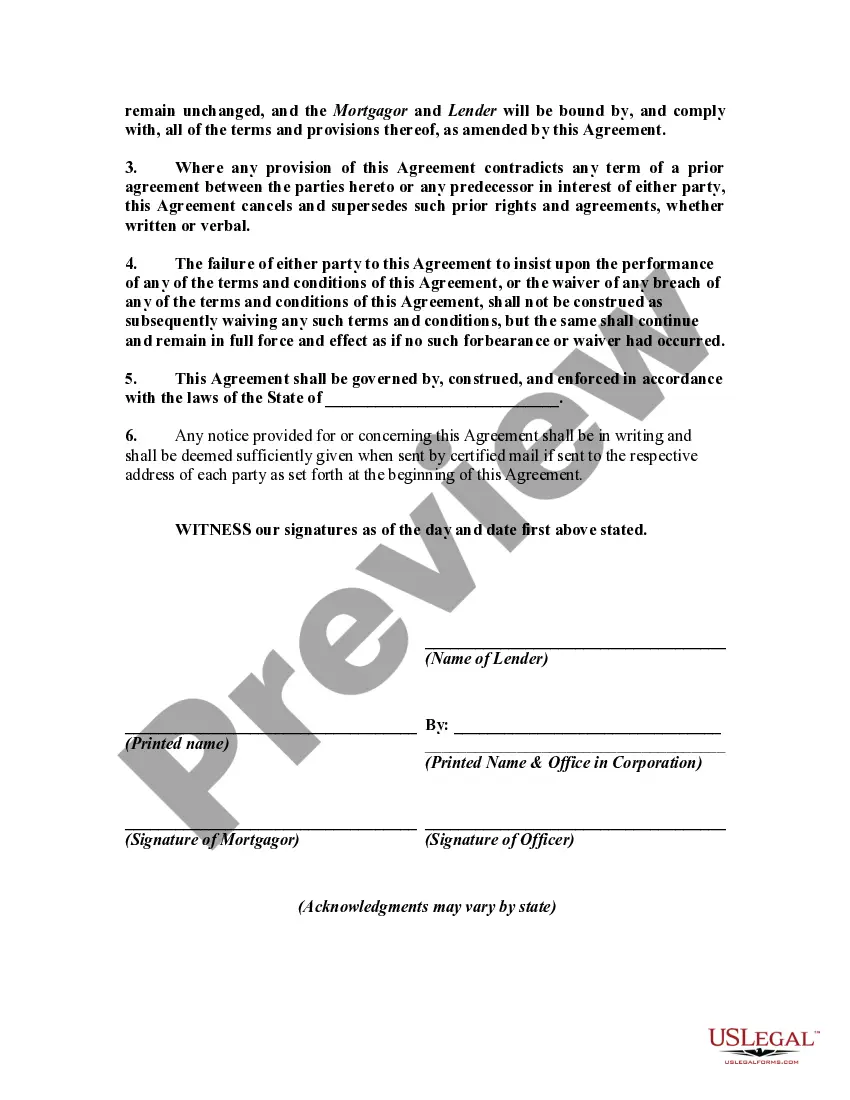

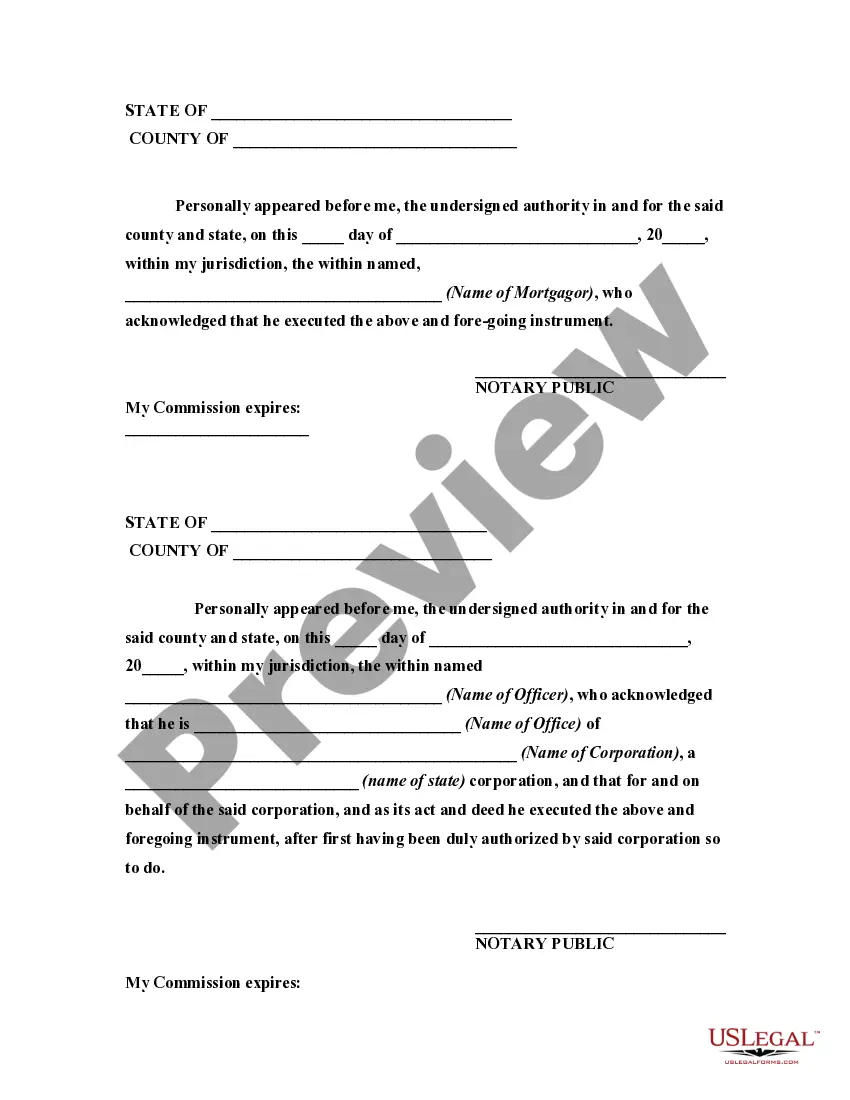

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A detailed description of an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage entails a legal document that outlines the terms and conditions for altering the interest rate on a promissory note that is secured by a mortgage in the state of Ohio, United States. This agreement is typically prepared when the original terms of the promissory note no longer suit the borrower's financial circumstances or when both parties agree to modify the loan agreement. The Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage includes various key elements and provisions to ensure clarity and legal validity. These elements may encompass the identification and contact information of the involved parties, including the borrower and the lender. The document should also specify the original promissory note details, such as the loan amount, the mortgage terms, the original interest rate, and the maturity date. The modified interest rate is a crucial component of this agreement. It should be clearly stated and explicitly indicate the new rate that will be applied to the outstanding balance of the promissory note. The parties should agree on this modified rate, ensuring that it is fair and reasonable for both sides. The agreement might explicitly state whether the modified rate is fixed or variable, establishing how it will be recalculated or adjusted, if applicable. Additionally, an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage should cover the effective date of the modification, describing when the new interest rate will be implemented. The agreement should also include the repayment terms, such as the revised monthly installment amount, the number of remaining payments, any changes to the loan term, or other pertinent details related to the monthly payment structure. Furthermore, the agreement should outline the process for amendment, stating any additional documents or actions required by the borrower or lender to solidify the modified interest rate. It may describe any fees associated with the modification or the costs of drafting the agreement, which are often borne by the borrower. It is important to note that while the general elements mentioned above should be present in an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage, the specific terms, details, and structures can vary depending on the individual circumstances and the mutual agreement between the borrower and lender. Different variations or types of this agreement could arise due to unique situations, such as modification of the interest rate on commercial mortgages, residential mortgages, or even government-backed mortgages. However, regardless of the type, it remains crucial to consult with legal professionals to ensure compliance with Ohio state laws, federal regulations, and to safeguard the rights and interests of both parties involved.A detailed description of an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage entails a legal document that outlines the terms and conditions for altering the interest rate on a promissory note that is secured by a mortgage in the state of Ohio, United States. This agreement is typically prepared when the original terms of the promissory note no longer suit the borrower's financial circumstances or when both parties agree to modify the loan agreement. The Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage includes various key elements and provisions to ensure clarity and legal validity. These elements may encompass the identification and contact information of the involved parties, including the borrower and the lender. The document should also specify the original promissory note details, such as the loan amount, the mortgage terms, the original interest rate, and the maturity date. The modified interest rate is a crucial component of this agreement. It should be clearly stated and explicitly indicate the new rate that will be applied to the outstanding balance of the promissory note. The parties should agree on this modified rate, ensuring that it is fair and reasonable for both sides. The agreement might explicitly state whether the modified rate is fixed or variable, establishing how it will be recalculated or adjusted, if applicable. Additionally, an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage should cover the effective date of the modification, describing when the new interest rate will be implemented. The agreement should also include the repayment terms, such as the revised monthly installment amount, the number of remaining payments, any changes to the loan term, or other pertinent details related to the monthly payment structure. Furthermore, the agreement should outline the process for amendment, stating any additional documents or actions required by the borrower or lender to solidify the modified interest rate. It may describe any fees associated with the modification or the costs of drafting the agreement, which are often borne by the borrower. It is important to note that while the general elements mentioned above should be present in an Ohio Agreement to Modify Interest Rate on Promissory Note Secured by a Mortgage, the specific terms, details, and structures can vary depending on the individual circumstances and the mutual agreement between the borrower and lender. Different variations or types of this agreement could arise due to unique situations, such as modification of the interest rate on commercial mortgages, residential mortgages, or even government-backed mortgages. However, regardless of the type, it remains crucial to consult with legal professionals to ensure compliance with Ohio state laws, federal regulations, and to safeguard the rights and interests of both parties involved.