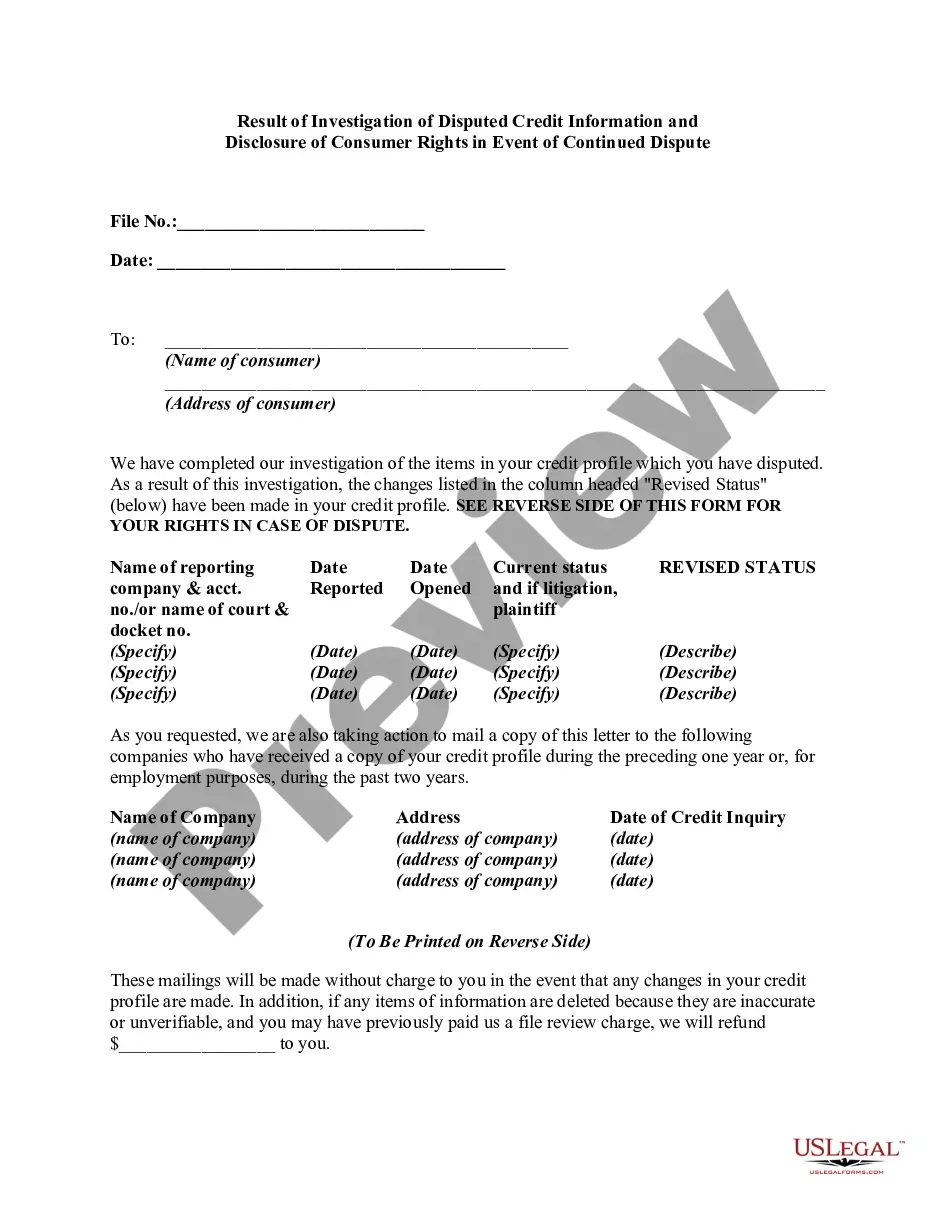

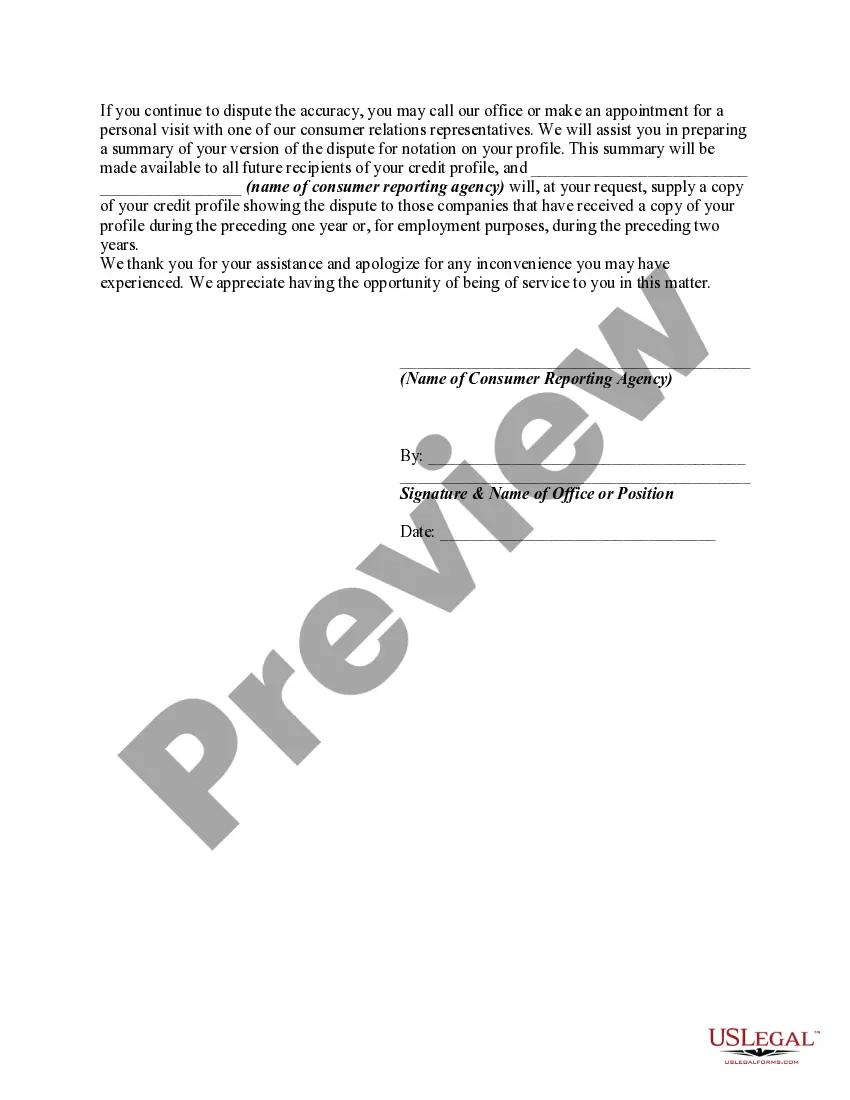

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Ohio Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute Introduction: In the state of Ohio, consumers are protected by specific laws and regulations when it comes to disputing credit information and ensuring accurate and fair reporting. This detailed description will highlight the Ohio result of investigations regarding disputed credit information and elaborate on consumer rights in the event of continued dispute. Keywords: OHIhi— - Result of investigation - Disputed credit information — Disclosure of consumer right— - Continued dispute Ohio Result of Investigation of Disputed Credit Information: When a consumer in Ohio files a dispute regarding inaccurate credit information, the result of the investigation may vary depending on the specific circumstances and evidence provided. The Ohio Revised Code and various federal laws, such as the Fair Credit Reporting Act (FCRA), govern the process and provide guidelines for credit reporting agencies (Crash) and creditors to investigate these disputes thoroughly. Types of Ohio Results of Investigation: 1. Verified Inaccuracies: If the investigation finds that the disputed credit information is indeed inaccurate or incomplete, the result may favor the consumer. This could involve correcting the credit report and ensuring that the erroneous information is removed or updated. 2. Unsubstantiated Claims: In cases where the consumer's dispute lacks supporting evidence or fails to prove inaccuracies, the investigation may result in maintaining the disputed credit information as accurate and complete. The consumer will be notified of the decision, and the disputed information will remain on the credit report. 3. Insufficient Investigation: If a credit reporting agency fails to conduct a proper investigation within the required timeframe or demonstrates negligence, the Ohio result of the investigation could lean in favor of the consumer. This may involve removing the inaccurate information and potentially imposing penalties on the agency. Disclosure of Consumer Rights in the Event of Continued Dispute: Ohio provides consumers with additional rights and resources to assert their claims in the event of a continued dispute over credit information. These rights aim to safeguard individuals from prolonged injustices that arise from unresolved disputes. Key disclosures and rights include: 1. Right to File a Consumer Complaint: Consumers have the right to file a complaint with the Ohio Attorney General's office, the Consumer Financial Protection Bureau (CFPB), or other relevant regulatory agencies if they believe their dispute has not been adequately addressed or resolved. 2. Right to Legal Action: Consumers retain the right to seek legal action against credit reporting agencies, creditors, or any other party involved if they believe their rights have been violated, such as through continued reporting of inaccurate information or failure to investigate in compliance with Ohio laws. 3. Right to Request Free Credit Reports: Consumers have the right to obtain free credit reports from the three major credit reporting agencies — Equifax, Experian, and TransUnion. Regularly monitoring these reports allows individuals to identify any inaccurate or fraudulent information. Conclusion: Understanding the Ohio result of investigation of disputed credit information and knowledge of consumer rights in the event of a continued dispute is essential for residents to ensure fair and accurate credit reporting. By being aware of their rights and utilizing appropriate channels for resolution, consumers in Ohio can protect their financial reputation and maintain a positive credit profile.