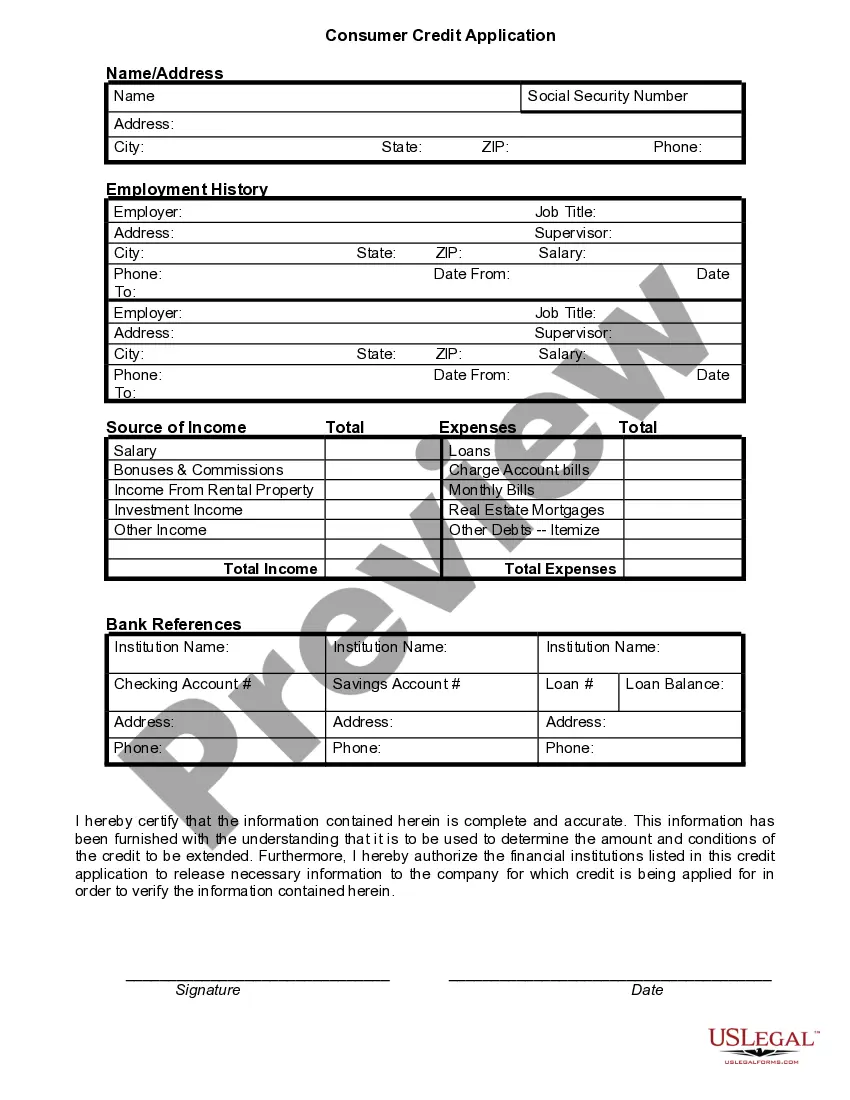

This form is a Consumer Loan Application. The form provides sections for: information regarding applicant, marital status, and asset information.

Ohio Consumer Loan Application - Personal Loan Agreement

Category:

State:

Multi-State

Control #:

US-01706-AZ

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Consumer Loan Application - Personal Loan Agreement?

Are you currently within a position where you will need documents for possibly business or specific uses just about every time? There are plenty of authorized record layouts available on the net, but getting versions you can rely is not easy. US Legal Forms gives thousands of kind layouts, much like the Ohio Consumer Loan Application - Personal Loan Agreement, which are written to satisfy federal and state demands.

In case you are previously familiar with US Legal Forms web site and get a merchant account, merely log in. Afterward, it is possible to obtain the Ohio Consumer Loan Application - Personal Loan Agreement format.

If you do not provide an bank account and want to begin to use US Legal Forms, adopt these measures:

- Get the kind you need and ensure it is to the proper metropolis/region.

- Take advantage of the Review option to examine the shape.

- Browse the outline to ensure that you have chosen the appropriate kind.

- In the event the kind is not what you`re trying to find, make use of the Search area to get the kind that suits you and demands.

- When you find the proper kind, just click Acquire now.

- Select the prices program you need, fill out the necessary details to make your money, and pay money for the order using your PayPal or bank card.

- Decide on a convenient file file format and obtain your copy.

Locate all of the record layouts you have purchased in the My Forms food list. You can obtain a extra copy of Ohio Consumer Loan Application - Personal Loan Agreement whenever, if possible. Just click the necessary kind to obtain or print the record format.

Use US Legal Forms, one of the most considerable selection of authorized types, to save lots of some time and avoid blunders. The support gives professionally made authorized record layouts that you can use for a selection of uses. Create a merchant account on US Legal Forms and start creating your daily life a little easier.

Form popularity

FAQ

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

They are designed to set expectations for a loan so that both the borrower and the lender understand the terms. A personal loan agreement can be referred to if there are questions about repayment, and it can be used to legally enforce terms if one party doesn't adhere to them.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

How to make a family loan agreement The amount borrowed and how it will be used. Repayment terms, including payment amounts, frequency and when the loan will be repaid in full. The loan's interest rate. ... If the loan can be repaid early without penalty, and how much interest will be saved by early repayment.

What a personal loan agreement should include Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided. Repayment date. Interest rate to be charged (if applicable). Annual percentage rate (if applicable).

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

Hear this out loud PauseInclude key terms of the loan, such as the lender and borrower's contact information, the reason for the loan, what is being loaned, the interest rate, the repayment plan, what would happen if the borrower can't make the payments, and more. The amount of the loan, also known as the principal amount.

Hear this out loud PauseDo you need to notarize a Loan Agreement? First and foremost, understand that personal loan agreements fall into the classification of contracts. Technically, you don't have to notarize these documents. But if you want to make this document legally binding, then notarization is the best course of action.