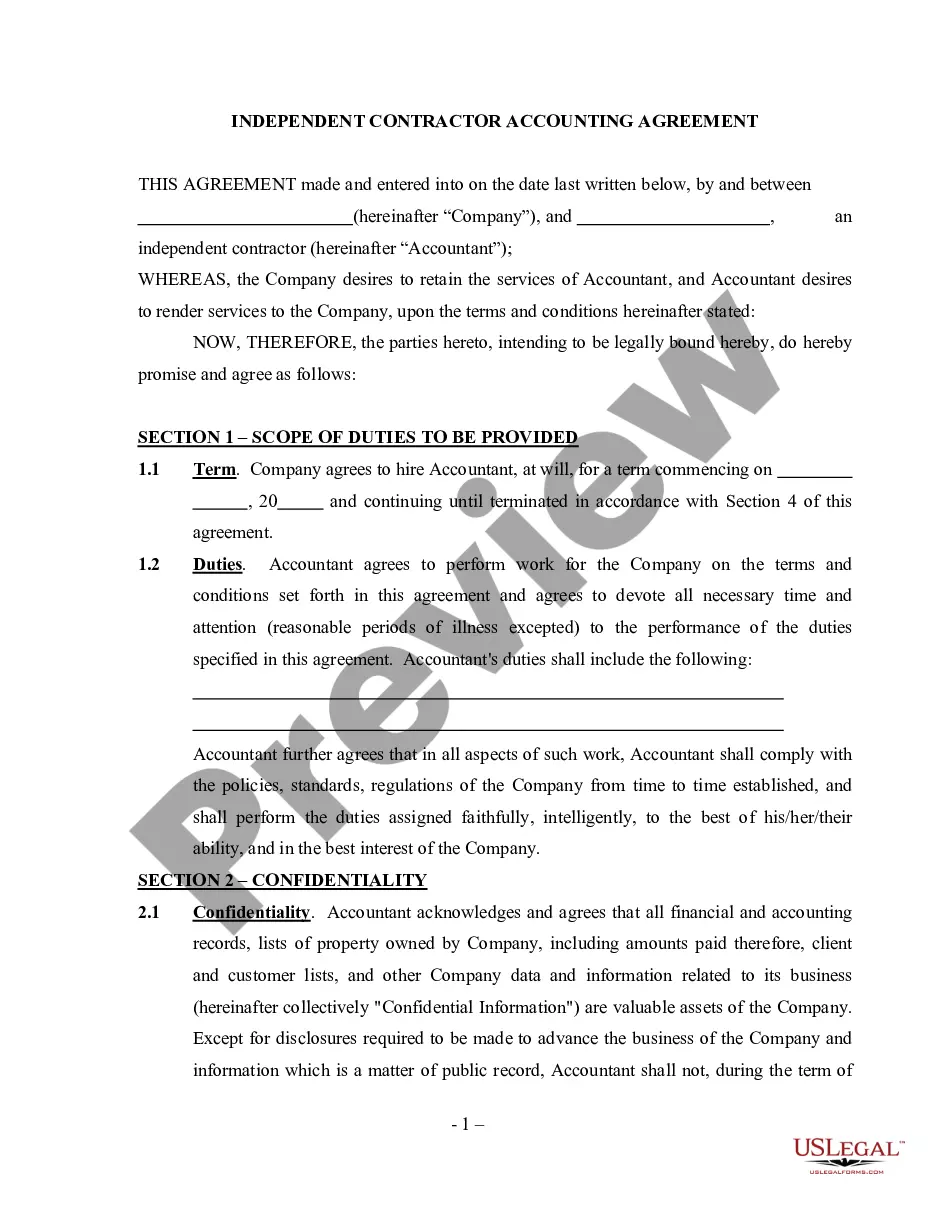

Generally, a contract to employ a certified public accountant need not be in writing.

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Ohio Contract with Accountant to Audit Corporation's Group Medical, Disability, and Life Insurance Program

Instant download

Description

Free preview

How to fill out Contract With Accountant To Audit Corporation's Group Medical, Disability, And Life Insurance Program?

Finding the appropriate legal document template can be challenging. Of course, numerous templates are available online, but how can you locate the legal document you need? Visit the US Legal Forms website. This service provides thousands of templates, including the Ohio Contract with Accountant to Review Corporation's Group Medical, Disability, and Life Insurance Program, which you can utilize for business and personal needs. All documents are reviewed by professionals and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Download button to obtain the Ohio Contract with Accountant to Review Corporation's Group Medical, Disability, and Life Insurance Program. Use your account to search through the legal forms you have previously acquired. Go to the My documents section of your account and retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions you should follow: First, ensure that you have selected the correct form for your city/state. You can review the form using the Review option and read the form summary to confirm it is the right one for you. If the form does not meet your requirements, use the Search field to find the appropriate form. Once you are confident that the form suits your needs, click the Get now button to obtain it. Choose the payment plan you prefer and enter the necessary details. Create your account and pay for the order using your PayPal account or credit card. Select the document format and download the legal document template to your device. Complete, edit, print, and sign the downloaded Ohio Contract with Accountant to Review Corporation's Group Medical, Disability, and Life Insurance Program.

- US Legal Forms is the largest library of legal forms where you can find various document templates.

- Use the service to download well-crafted documents that meet state requirements.