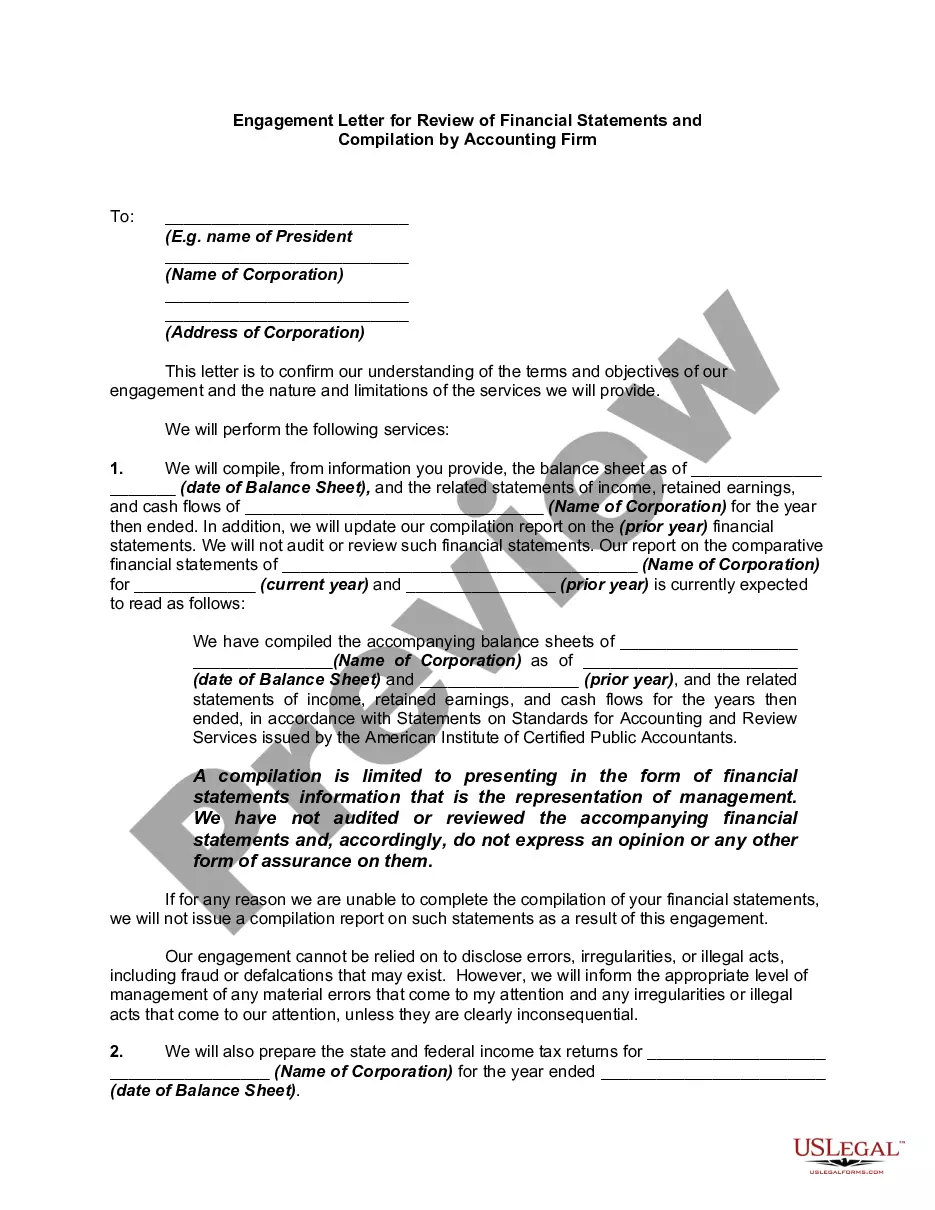

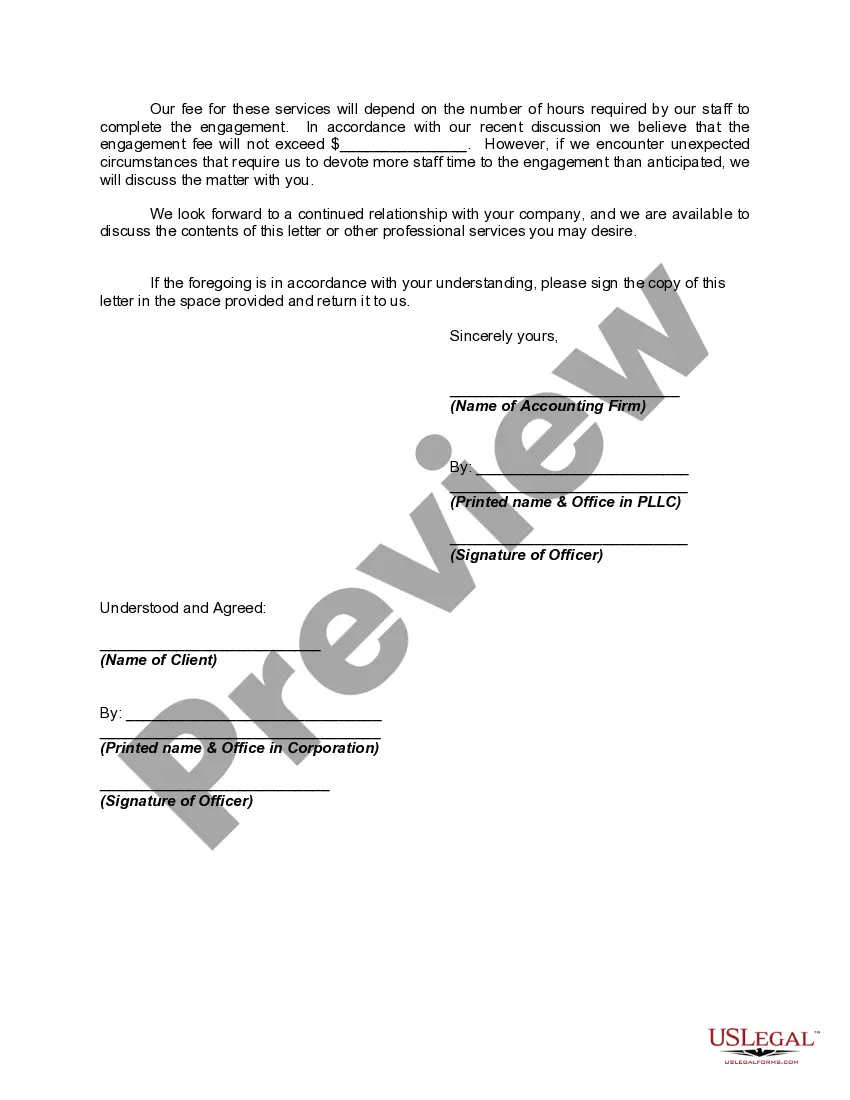

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Ohio Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm: An engagement letter is a formal agreement between an accounting firm and a client to outline the scope of services provided, including the review of financial statements and compilation. In Ohio, there are various types of engagement letters for reviews and compilations, each serving a specific purpose. 1. Ohio Engagement Letter for Review of Financial Statements: This type of engagement letter is used when an accounting firm is hired to conduct a review of a company's financial statements. It outlines the procedures to be performed, the responsibilities of both the accounting firm and the client, and the expected deliverables. The review provides limited assurance, primarily focusing on analytical procedures, inquiries, and discussions with management. 2. Ohio Engagement Letter for Compilation of Financial Statements: This engagement letter is used when an accounting firm is engaged to compile a company's financial statements. It clarifies that the accounting firm will gather and organize the financial data provided by the client, without expressing any assurance on the accuracy or reliability of the information. The compilation ensures that the financial statements are presented in the proper format and conform to the applicable financial reporting framework. 3. Ohio Engagement Letter for Agreed-Upon Procedures: Although not strictly within the review and compilation scope, it is worth mentioning the engagement letter for agreed-upon procedures, as it may be requested in some cases. This type of engagement letter specifies that an accounting firm will perform procedures agreed upon by both the firm and the client. The procedures can address specific financial statement accounts, transactions, or internal controls. The firm will report the factual findings without providing any assurance on the overall financial statements. When drafting an Ohio engagement letter for review of financial statements and compilation, several important keywords should be included: — Accuracy: Ensuring that the financial statements reflect an accurate representation of the company's financial position. — Compliance: Following the relevant financial reporting framework and regulatory requirements. — Procedures: Outlining the specific procedures to be performed in the review or compilation process. — Assurance: Clarifying the extent of the assurance provided, whether it is limited (review) or none (compilation). — Independence: Affirming the accounting firm's independence from the client to maintain objectivity and credibility. — Deliverables: Specifying the final deliverable format, such as a report containing the findings and conclusions of the review or compilation. — Timeframe: Establishing the agreed-upon timeline for completion of the engagement. — Fees: Disclosing the fee structure for the services provided and any additional expenses. Overall, an Ohio engagement letter for review of financial statements and compilation by an accounting firm sets the framework for a transparent and mutually beneficial relationship between the accounting firm and the client. It ensures clear communication, establishes expectations, and provides guidance for the financial reporting process, ultimately contributing to accurate and reliable financial statements.