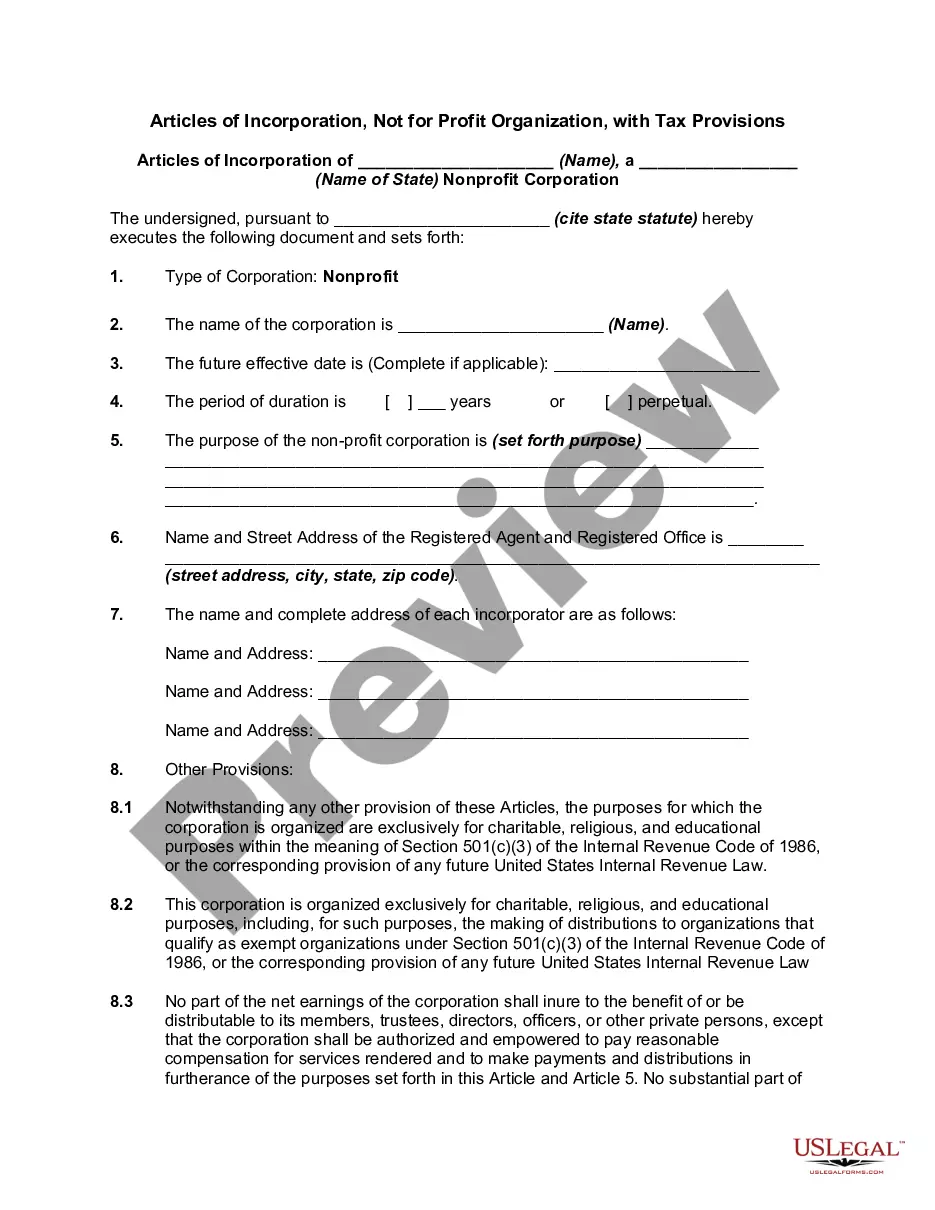

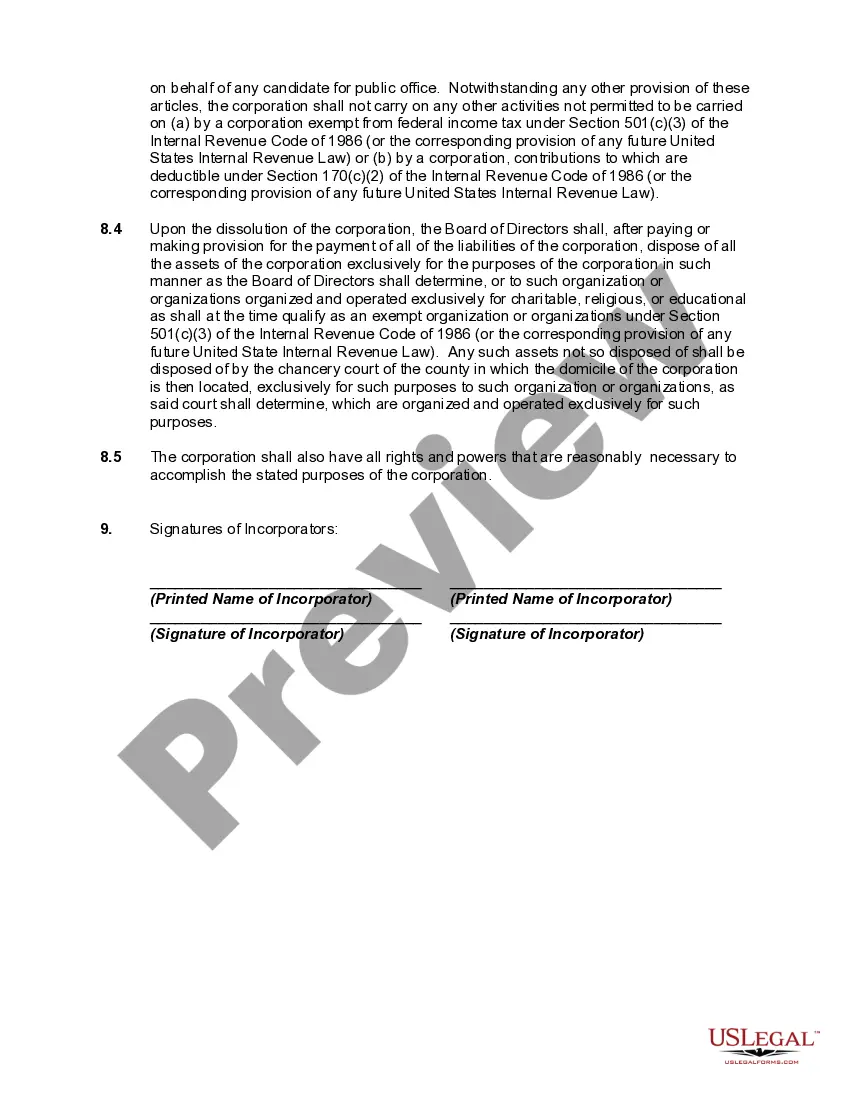

Title: Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions: A Comprehensive Guide Introduction: Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions refer to the legal document required to form and register a nonprofit organization in the state of Ohio. These articles outline important details about the organization and its purpose, while also addressing tax-related provisions to ensure compliance with applicable laws and regulations. This article provides a detailed description of the Ohio Articles of Incorporation, Not for Profit Organization, with a specific focus on its tax provisions. Key Keywords: OHIhi— - Articles of Incorporation - Not for Profit Organization — Tax Provisions Different Types of Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions: 1. Regular Ohio Articles of Incorporation: These articles incorporate a nonprofit organization that aims to serve a charitable, educational, religious, scientific, or other recognized purpose under the law. They include provisions related to tax-exempt status and IRS compliance. 2. Ohio Articles of Incorporation, Public Charity: These articles are specific to nonprofit organizations that qualify as public charities under the tax code. They necessitate adherence to additional rules related to public support and community benefit, resulting in enhanced tax benefits for donors. 3. Ohio Articles of Incorporation, Private Foundation: These articles pertain to nonprofit organizations classified as private foundations. Unlike public charities, private foundations typically rely on a single source or a small group of donors for funding and have different tax implications and restrictions. Detailed Description: The Ohio Articles of Incorporation for a Not for Profit Organization, with Tax Provisions, serve as a foundational document that sets out essential information about the nonprofit's purpose, structure, and governance. It is mandatory to fill out this document as part of the incorporation process or when seeking tax-exempt status. These articles typically include the following key provisions: 1. Name and Purpose: The organization's legal name, as well as a clear and specific purpose statement that aligns with the recognized charitable or nonprofit purposes defined by Ohio law. 2. Duration: Specifies the duration or perpetual nature of the organization, determining its lifespan. 3. Registered Agent: Identifies the registered agent, usually a person or an entity authorized to receive legal notices and correspondence on behalf of the organization. 4. Principal Office: Declares the physical address of the organization's principal office within the state of Ohio. 5. Membership: Details provisions for membership, if applicable. Not all nonprofit organizations include membership structures, as some may operate solely with a board of directors or trustees. 6. Governance: Outlines the structure and responsibilities of the board of directors or trustees, including rules for their appointment, terms, removal, and meetings. 7. Dissolution Clause: Includes a provision describing how the organization's assets will be distributed if it is dissolved. 8. Tax Provisions: This section addresses important tax-related provisions that ensure compliance with federal and state laws governing tax-exempt organizations. It includes details about applying for tax-exempt status, maintaining compliance with IRS regulations, reporting requirements, and restrictions on lobbying, political activities, and private benefit. Conclusion: Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions, is a crucial legal document that outlines the formation and operational details of a nonprofit organization. Understanding the different types and relevant tax provisions is essential for nonprofit founders, directors, and members to ensure compliance and maximize the organization's ability to fulfill its mission while enjoying tax benefits.

Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Ohio Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

Are you presently in the situation the place you need paperwork for both enterprise or person purposes just about every day time? There are plenty of lawful record templates available online, but getting ones you can rely on is not effortless. US Legal Forms offers a large number of form templates, such as the Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions, that are composed to fulfill state and federal needs.

Should you be currently knowledgeable about US Legal Forms site and get a free account, just log in. Next, you may obtain the Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions format.

Unless you come with an bank account and want to begin using US Legal Forms, follow these steps:

- Obtain the form you require and make sure it is for the right area/state.

- Take advantage of the Preview option to check the form.

- Look at the explanation to ensure that you have selected the proper form.

- If the form is not what you are searching for, make use of the Look for area to obtain the form that meets your needs and needs.

- If you obtain the right form, click on Buy now.

- Select the costs strategy you need, submit the required details to create your account, and pay money for an order with your PayPal or bank card.

- Choose a hassle-free paper formatting and obtain your copy.

Locate all of the record templates you possess bought in the My Forms food list. You can obtain a more copy of Ohio Articles of Incorporation, Not for Profit Organization, with Tax Provisions at any time, if possible. Just click on the required form to obtain or print out the record format.

Use US Legal Forms, one of the most considerable assortment of lawful types, to conserve some time and prevent faults. The support offers appropriately produced lawful record templates which can be used for a variety of purposes. Generate a free account on US Legal Forms and initiate creating your daily life a little easier.