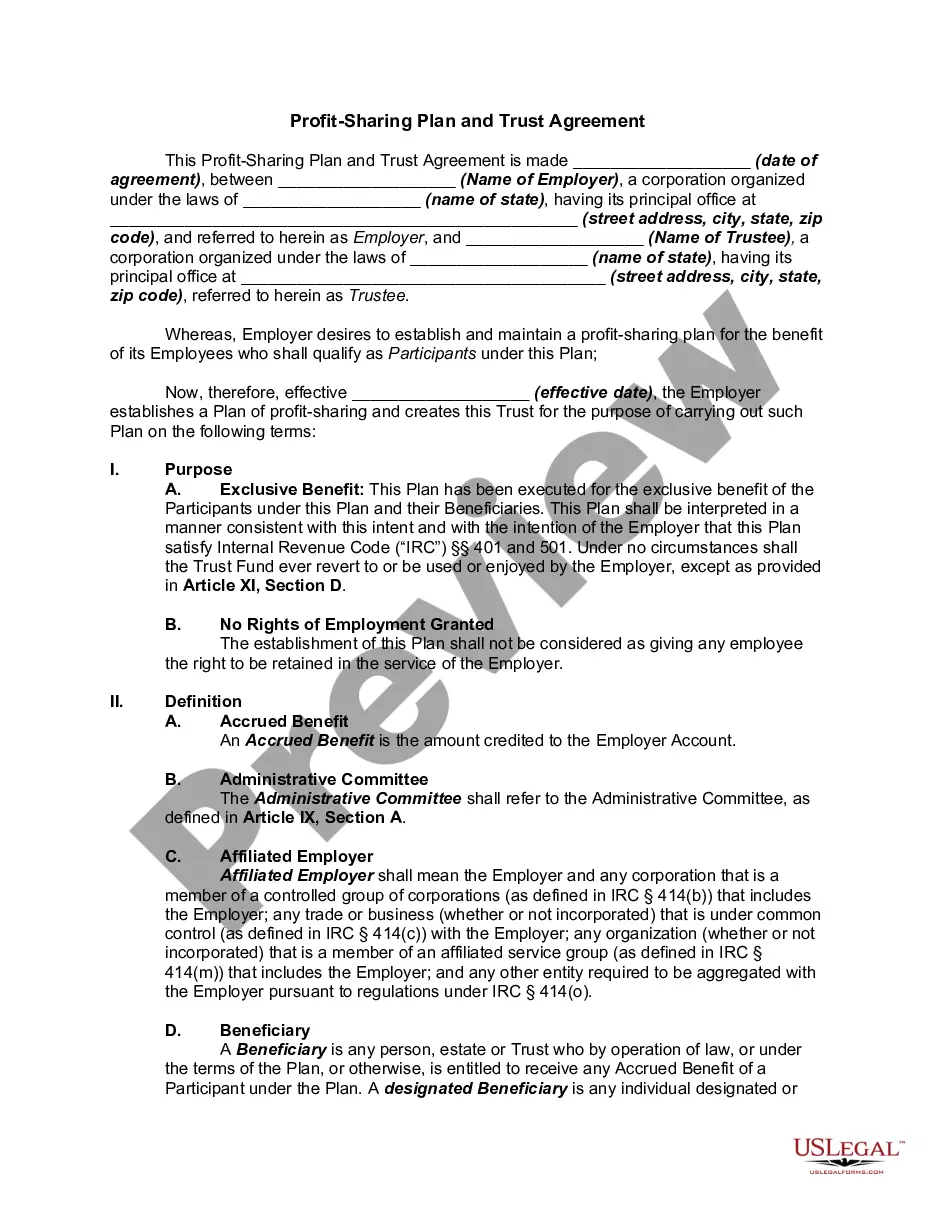

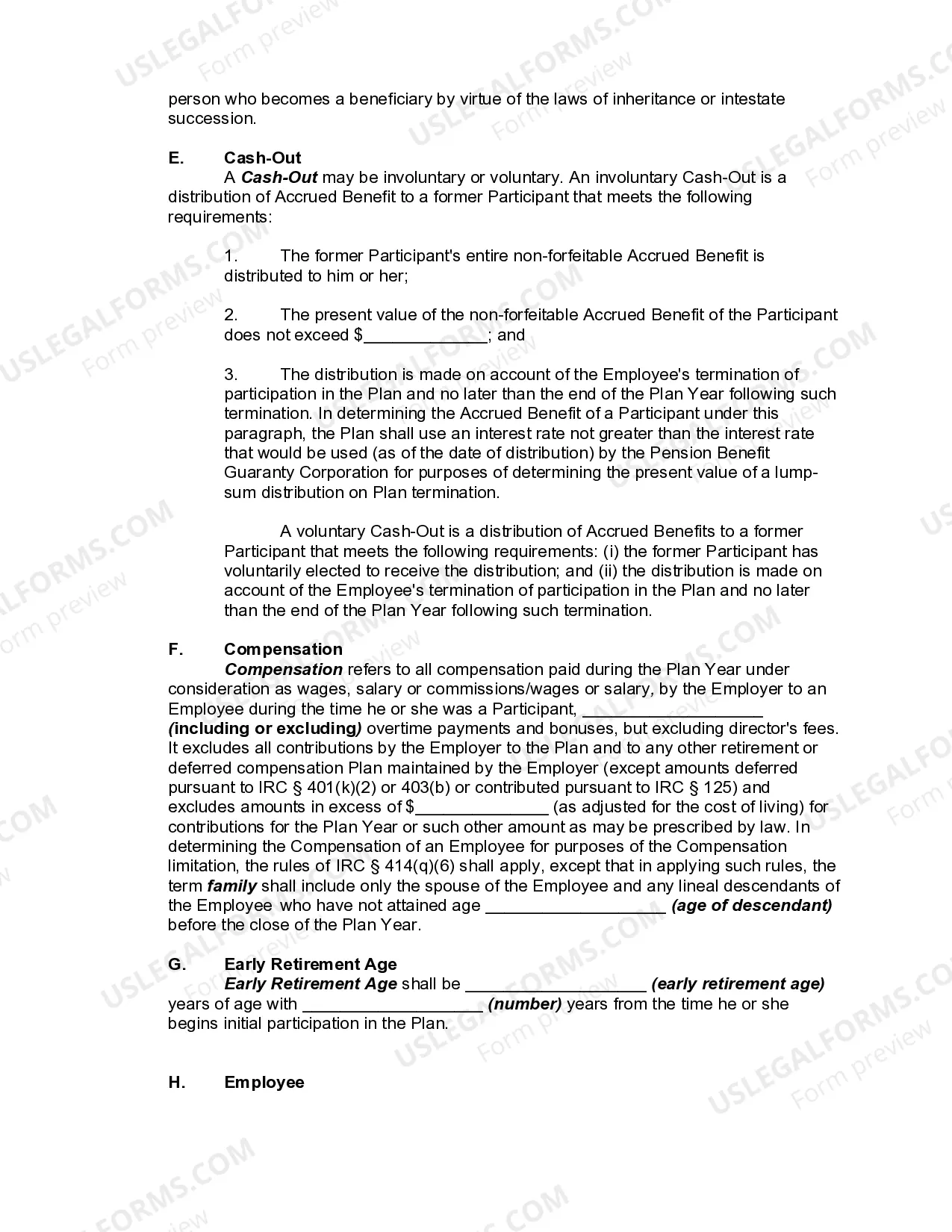

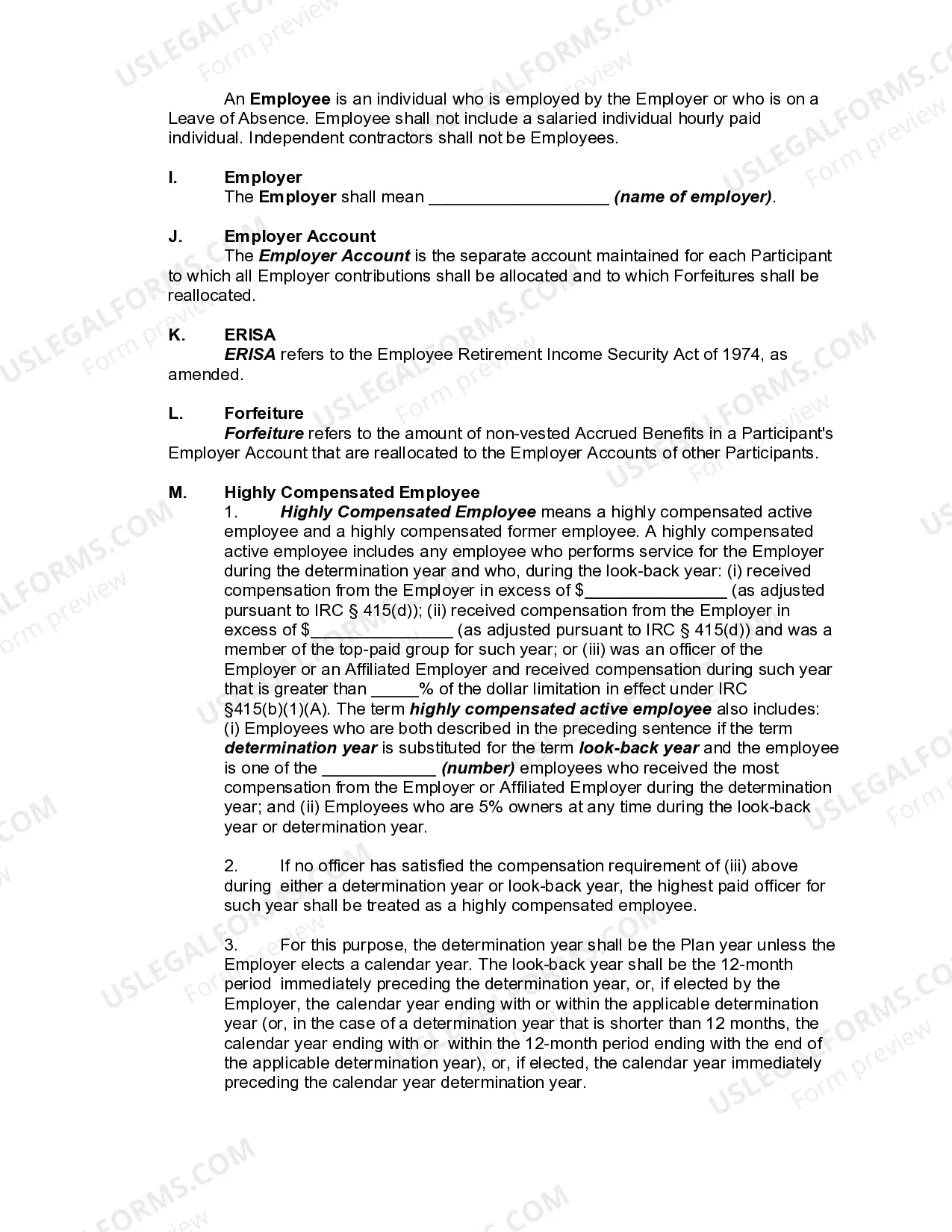

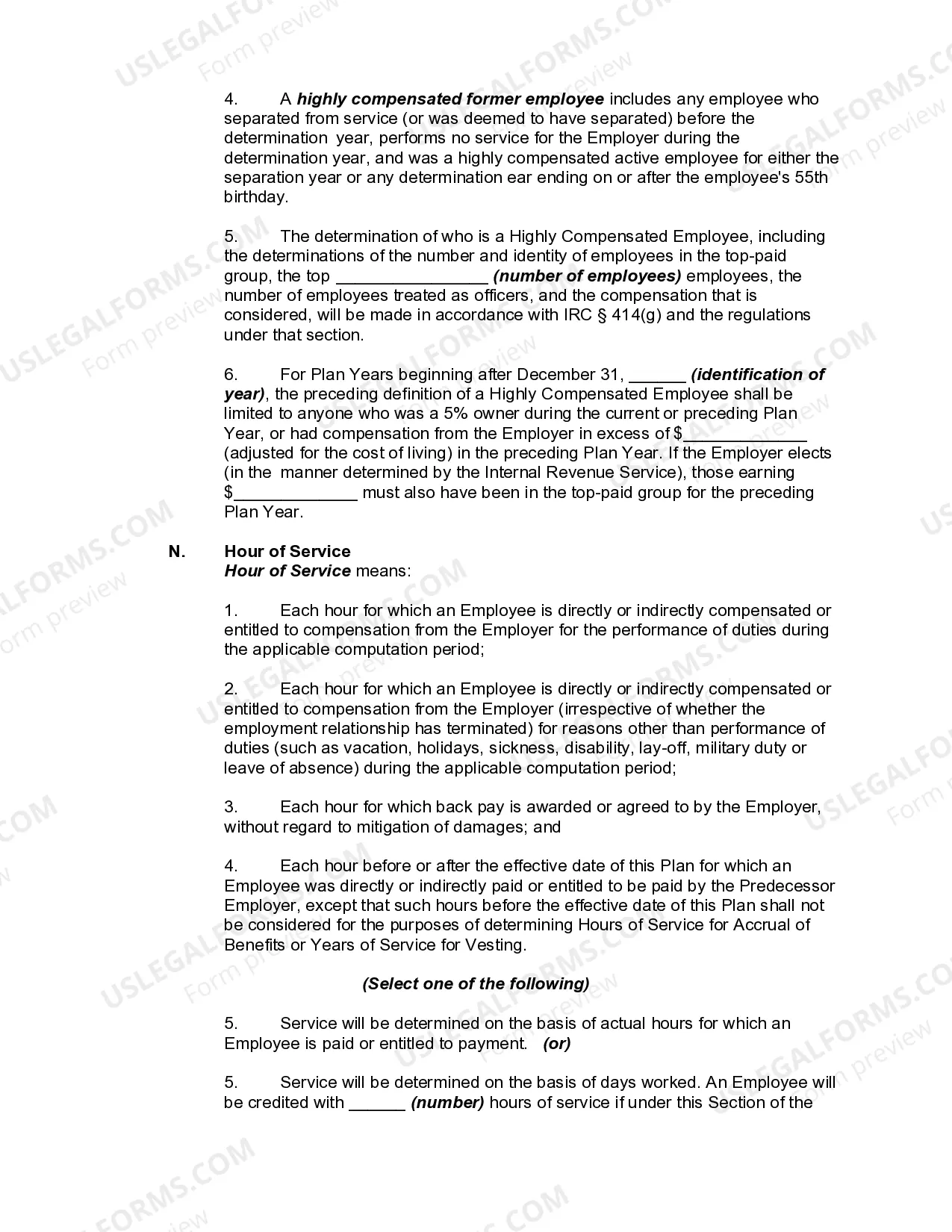

A profit-sharing plan is a defined-contribution plan established and maintained by an employer to provide for the participation in profits by employees and their beneficiaries. The plan must provide a definite predetermined formula for allocating the contributions made to the plan among the participants and for distributing the funds accumulated under the plan.

The Ohio Profit-Sharing Plan and Trust Agreement is a legal document that outlines the terms and conditions of establishing and managing a profit-sharing plan in the state of Ohio. It is designed to incentivize employees by providing them with a share in the company's profits. The plan is typically established by an employer, who contributes a percentage of the company's annual profits to a trust fund set up specifically for this purpose. The Ohio Profit-Sharing Plan and Trust Agreement serves as a comprehensive guide for employers on how to set up, administer, and distribute profits through the profit-sharing plan. It includes provisions related to eligibility criteria, contribution limits, vesting schedules, participant rights and responsibilities, as well as methods for calculating and allocating profits. There are different types of profit-sharing plans that can be established in Ohio, depending on the specific needs and goals of the employer. Some common variations include: 1. Traditional Profit-Sharing Plan: This type of plan allows employers to contribute a portion of their profits to a trust fund, which is then distributed among eligible employees according to a predetermined formula. The distribution may be based on factors such as the employee's salary, length of service, or position within the company. 2. 401(k) Profit-Sharing Plan: This plan combines elements of both a traditional profit-sharing plan and a 401(k) retirement plan. In addition to receiving a share of the company's profits, employees are also given the option to contribute a portion of their salary to the plan on a pre-tax basis. The employer may choose to match a certain percentage of the employee's contributions, further enhancing their retirement savings. 3. New Comparability Profit-Sharing Plan: This type of plan allows employers to allocate different contribution percentages to different groups of employees based on various factors. For example, employers can contribute a higher percentage of profits to key executives or employees in specialized roles, while providing a lower contribution percentage for other employees. When establishing an Ohio Profit-Sharing Plan and Trust Agreement, it is essential to consult with legal and financial professionals who can guide employers through the intricacies of plan design, compliance with state and federal regulations, and tax considerations. Implementing a well-designed profit-sharing plan can help attract and retain talented employees, foster a cooperative work environment, and provide valuable retirement benefits.