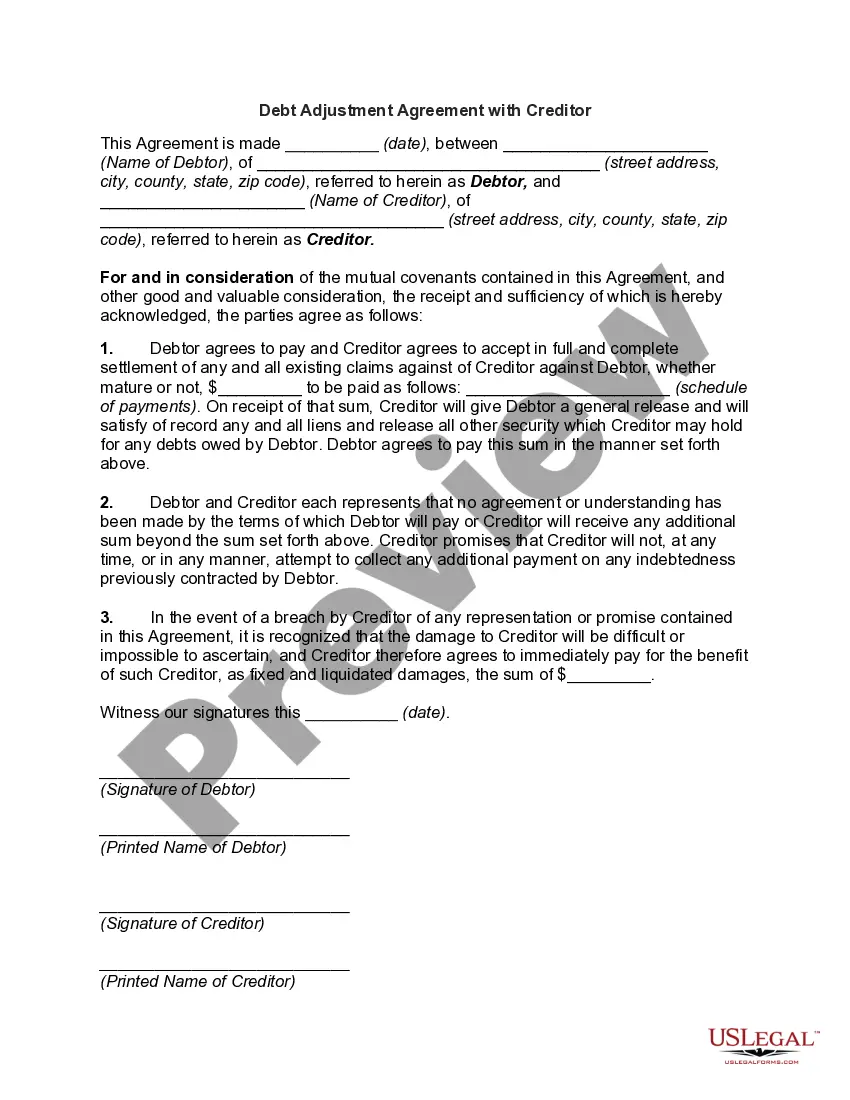

Ohio Agreement that Statement of Account is True, Correct and Settled

Description

How to fill out Agreement That Statement Of Account Is True, Correct And Settled?

If you aim to be thorough, obtain, or generate legal document templates, utilize US Legal Forms, the largest selection of legal forms available online.

Take advantage of the site's straightforward and user-friendly search to locate the documents you require.

Various templates for business and personal purposes are categorized by types and states, or keywords.

Step 3. If you are not satisfied with the form, use the Search box at the top of the screen to find other versions of the legal form format.

Step 4. Once you have identified the form you need, click the Get now button. Choose the pricing plan you prefer and add your information to register for the account.

- Use US Legal Forms to find the Ohio Agreement that Affirms Statement of Account is Accurate, Correct, and Settled with just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to obtain the Ohio Agreement that Affirms Statement of Account is Accurate, Correct, and Settled.

- You can also access forms you previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Utilize the Review option to examine the form's content. Don't forget to read the description.

Form popularity

FAQ

Civil Rule 75 in Ohio governs the procedures for divorce and legal separation cases. It outlines how courts manage and resolve disputes regarding property, child custody, and other family law matters. Following these rules is essential for a fair and efficient legal process. For your peace of mind, consider using an Ohio Agreement that Statement of Account is True, Correct and Settled to document and confirm your financial standings.

Section 1337.14 in the Ohio Revised Code deals with the management of property interests and the importance of agreements between parties involved. This section underscores the necessity of forming clear and concise agreements that show that accounts are true, correct, and settled, which is vital in real estate transactions. Understanding these stipulations can help you avoid legal disputes. For assistance in creating compliant agreements, consider using uslegalforms for reliable legal documentation.

Claims against the estate may be made up to six months from the date of death. A small estate that does not require the filing of a federal estate tax return and has no creditor issues often can be settled within six months of the appointment of the executor or administrator.

The Executor of an Estate is allowed to sell property owned by the deceased person, as long as there are no surviving joint owners or clauses in the Will that prevent selling the property.

If assets have to be sold to produce funds to pay Joan's debts, the Executors must agree which assets are to be sold. They cannot make unilateral decisions and act on them just because they think it is the sensible thing to do; or because some of the beneficiaries are pressurising them to do it.

How to Probate A Will In OhioStep 1: Find and File the Decedent's Will.Step 2: Order Decedent's Death Certificate.Step 3: Petition for Probate.Step 4: The Probate Is Opened and Letters of Authority Are Issued.Step 5: Administration, Creditors, and Inventory of the Estate.More items...?

Rule 4(d) provides that a magistrate judge may issue an arrest warrant or summons based on information submitted electronically rather than in person.

Once creditors have been dealt with, the executor must petition the probate court to close the estate. To help move the closeout process along, they may seek and receive waivers from the estate's beneficiaries. Upon approval from the court, the estate can be distributed to beneficiaries.

(3) All motions shall be ruled upon within one hundred twenty days from the date the moti on was filed, except as otherwi se noted on the report forms.

No probate at all is necessary if the estate is worth less than $5,000 or the amount of the funeral expenses. In that case, anyone (except the surviving spouse) who has paid or is obligated to pay those expenses may ask the court for a summary release from administration.