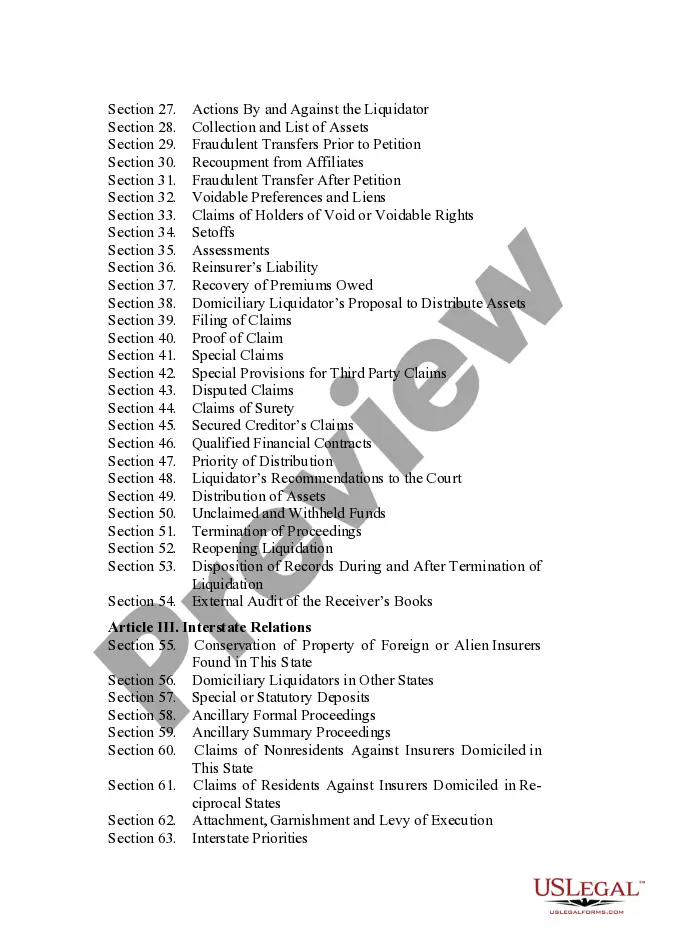

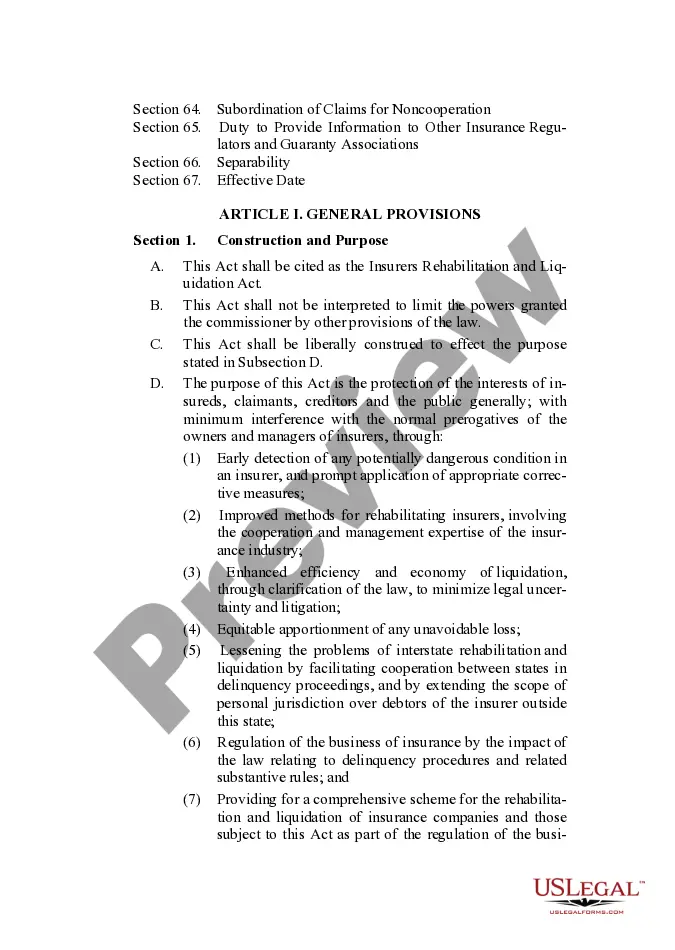

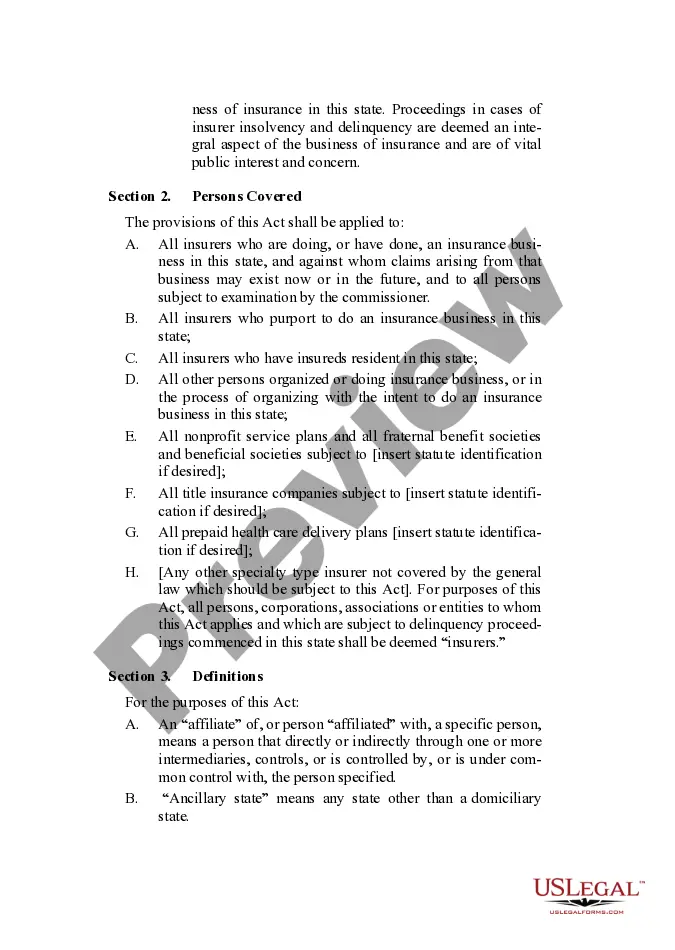

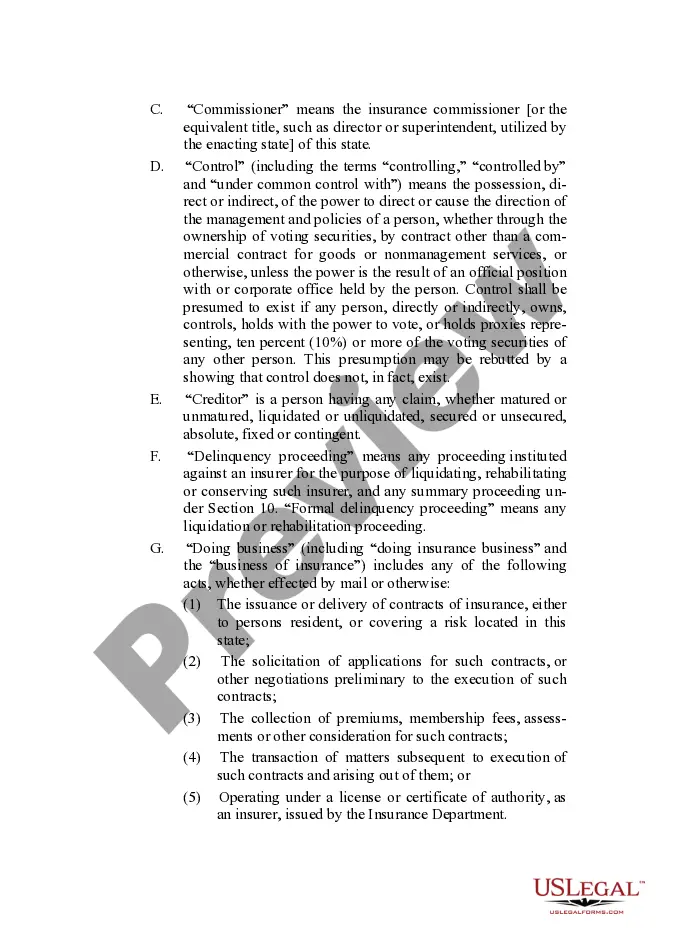

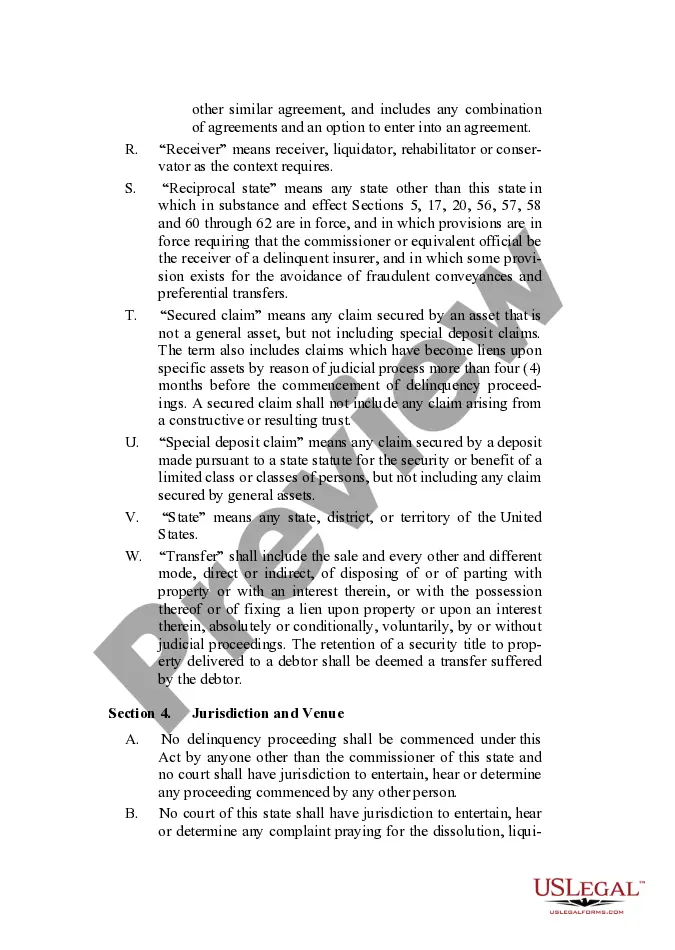

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The Ohio Insurers Rehabilitation and Liquidation Model Act (IRMA) is a comprehensive legislation designed to provide a legal framework for the rehabilitation and liquidation proceedings of insurance companies operating in the state of Ohio. This act ensures that the interests of policyholders, claimants, and other relevant stakeholders are protected when an insurer faces financial distress or insolvency. The IRMA establishes a set of procedures and guidelines for the orderly rehabilitation or liquidation process, aiming to maximize the recovery of assets to satisfy the claims of policyholders and creditors. It also ensures timely and efficient administration of insurance company insolvencies, maintaining regulatory oversight, and preserving the integrity of the insurance marketplace. The IRMA encompasses various provisions that outline the roles and responsibilities of the Ohio Department of Insurance, directors, officers, and other parties involved in the rehabilitation and liquidation process. Key areas covered by the act include: 1. Rehabilitation: This section of the act focuses on rehabilitating financially troubled insurers to ensure their solvency. It provides mechanisms for the department to oversee and supervise the rehabilitative measures undertaken by the insurer, including negotiating with policyholders, reinsurers, and other parties. 2. Liquidation: When rehabilitation efforts prove unsuccessful or not in the best interest of policyholders and creditors, the act provides guidance for the liquidation of the insolvent insurer's assets. It outlines the procedures for marshaling, valuing, and distributing assets to satisfy claims, giving priority to policyholder claims over general creditors. 3. Conservation: The IRMA also allows the Department of Insurance to initiate conservation proceedings in cases where an insurer's financial condition raises concerns but is not yet in a state of insolvency. Conservation aims to safeguard the insurer's assets and prevent further deterioration while efforts for rehabilitation or liquidation are made. 4. Reinsurance: The act addresses the treatment of reinsurance agreements held by the insolvent insurer, ensuring that the reinsured claims are properly accounted for and paid according to established guidelines. It also includes provisions to protect reinsurers' rights and obligations during the rehabilitation or liquidation process. It is worth noting that the Ohio Insurers Rehabilitation and Liquidation Model Act may have variations or amendments depending on the jurisdiction, as states may adapt the model act according to their specific legislative needs and regulatory requirements. However, these adaptations generally maintain the core principles and objectives of the act while accommodating state-specific considerations. In Ohio, the model act serves as the foundation for the state's insurance rehabilitation and liquidation proceedings and provides a structured approach to address insurer insolvency situations. By implementing this act, Ohio ensures that policyholders and claimants will have a fair and orderly process to rely on when facing financial troubles with their insurance providers, safeguarding their interests and maintaining confidence in the insurance industry.The Ohio Insurers Rehabilitation and Liquidation Model Act (IRMA) is a comprehensive legislation designed to provide a legal framework for the rehabilitation and liquidation proceedings of insurance companies operating in the state of Ohio. This act ensures that the interests of policyholders, claimants, and other relevant stakeholders are protected when an insurer faces financial distress or insolvency. The IRMA establishes a set of procedures and guidelines for the orderly rehabilitation or liquidation process, aiming to maximize the recovery of assets to satisfy the claims of policyholders and creditors. It also ensures timely and efficient administration of insurance company insolvencies, maintaining regulatory oversight, and preserving the integrity of the insurance marketplace. The IRMA encompasses various provisions that outline the roles and responsibilities of the Ohio Department of Insurance, directors, officers, and other parties involved in the rehabilitation and liquidation process. Key areas covered by the act include: 1. Rehabilitation: This section of the act focuses on rehabilitating financially troubled insurers to ensure their solvency. It provides mechanisms for the department to oversee and supervise the rehabilitative measures undertaken by the insurer, including negotiating with policyholders, reinsurers, and other parties. 2. Liquidation: When rehabilitation efforts prove unsuccessful or not in the best interest of policyholders and creditors, the act provides guidance for the liquidation of the insolvent insurer's assets. It outlines the procedures for marshaling, valuing, and distributing assets to satisfy claims, giving priority to policyholder claims over general creditors. 3. Conservation: The IRMA also allows the Department of Insurance to initiate conservation proceedings in cases where an insurer's financial condition raises concerns but is not yet in a state of insolvency. Conservation aims to safeguard the insurer's assets and prevent further deterioration while efforts for rehabilitation or liquidation are made. 4. Reinsurance: The act addresses the treatment of reinsurance agreements held by the insolvent insurer, ensuring that the reinsured claims are properly accounted for and paid according to established guidelines. It also includes provisions to protect reinsurers' rights and obligations during the rehabilitation or liquidation process. It is worth noting that the Ohio Insurers Rehabilitation and Liquidation Model Act may have variations or amendments depending on the jurisdiction, as states may adapt the model act according to their specific legislative needs and regulatory requirements. However, these adaptations generally maintain the core principles and objectives of the act while accommodating state-specific considerations. In Ohio, the model act serves as the foundation for the state's insurance rehabilitation and liquidation proceedings and provides a structured approach to address insurer insolvency situations. By implementing this act, Ohio ensures that policyholders and claimants will have a fair and orderly process to rely on when facing financial troubles with their insurance providers, safeguarding their interests and maintaining confidence in the insurance industry.