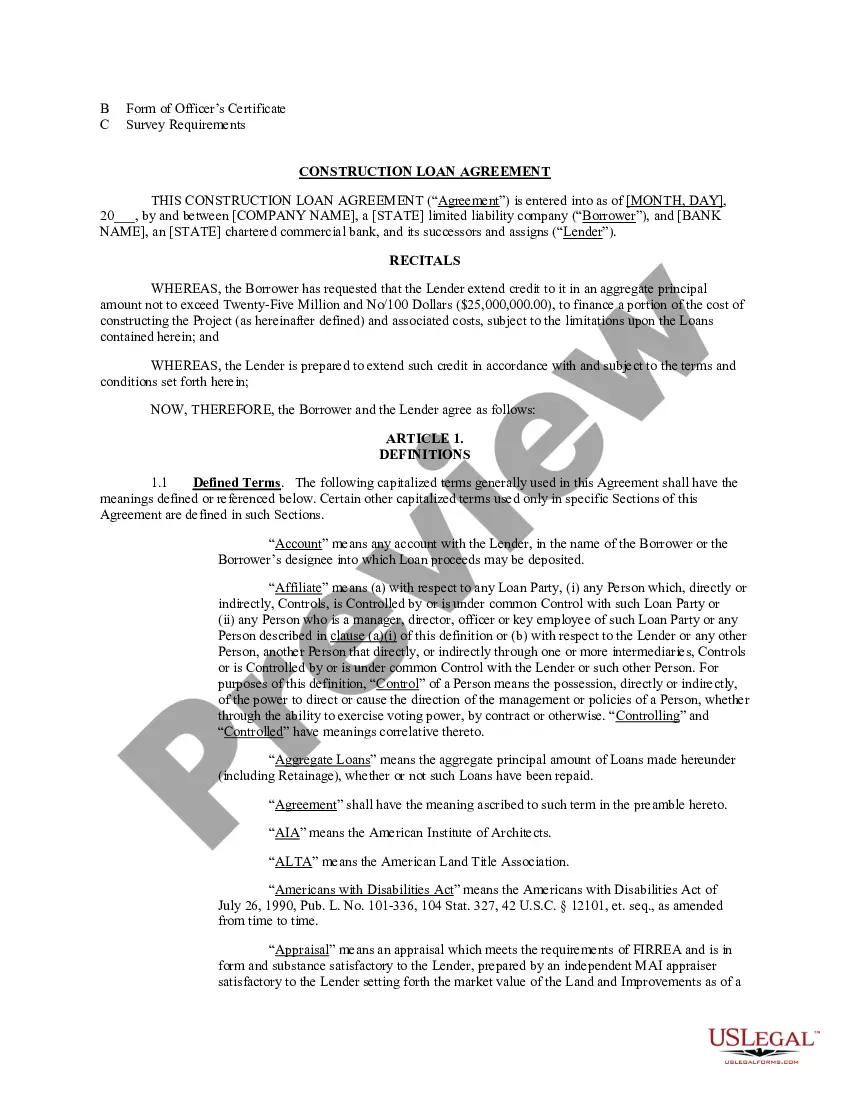

The Ohio Construction Loan Agreement is a legal contract that establishes the terms and conditions for a loan provided to finance the construction or renovation of a property in the state of Ohio. This loan agreement is crucial for both lenders and borrowers involved in the construction process, as it outlines the obligations, requirements, and rights of all parties involved. Keywords: Ohio Construction Loan Agreement, legal contract, terms and conditions, finance, construction, renovation, property, state of Ohio, loan agreement, lenders, borrowers, obligations, requirements, rights, parties involved. There are different types of Ohio Construction Loan Agreements available, based on the specific requirements and circumstances of the construction project. Some common types of Ohio Construction Loan Agreements are: 1. Single-Close Construction Loan Agreement: This type of agreement combines the financing for the land purchase and the construction costs into a single loan. It is suitable for borrowers who wish to streamline the financing process and avoid the hassle of obtaining separate loans. 2. Two-Time Close Construction Loan Agreement: In this arrangement, the borrower initially obtains a loan to purchase the land, and once the construction starts, a second loan is obtained to cover the construction costs. This type of agreement is typically used when the borrower already owns the land or wishes to buy it separately. 3. Construction-to-Permanent Loan Agreement: This agreement is designed for borrowers who plan to convert their construction loan into a long-term mortgage once the construction is completed. It eliminates the need for a separate loan for the permanent financing and simplifies the lending process. 4. Renovation Construction Loan Agreement: This type of agreement is tailored for borrowers who want to renovate or rebuild an existing property. It allows the borrower to finance the construction or renovation costs while considering the appraised value of the completed project. 5. Owner-Builder Construction Loan Agreement: This agreement is specifically crafted for individuals who intend to act as their own general contractors or builders during the construction process. It addresses the unique requirements and responsibilities of owner-builders and provides the necessary provisions for their involvement. It is important to note that these are just a few examples of Ohio Construction Loan Agreements, and the specific terms and conditions may vary depending on the lender, borrower, and the nature of the construction project.

Ohio Construction Loan Agreement

Description

How to fill out Ohio Construction Loan Agreement?

US Legal Forms - one of many most significant libraries of legal kinds in America - offers a variety of legal record templates you may down load or print out. While using site, you can get a large number of kinds for business and individual uses, sorted by groups, suggests, or key phrases.You can find the latest versions of kinds like the Ohio Construction Loan Agreement in seconds.

If you already have a subscription, log in and down load Ohio Construction Loan Agreement in the US Legal Forms collection. The Download key can look on each and every develop you perspective. You get access to all formerly delivered electronically kinds inside the My Forms tab of your own account.

If you want to use US Legal Forms the very first time, allow me to share basic directions to obtain started:

- Make sure you have picked the proper develop for the city/region. Click the Preview key to check the form`s articles. Look at the develop description to actually have chosen the right develop.

- In the event the develop does not satisfy your demands, use the Search area on top of the screen to obtain the one who does.

- When you are satisfied with the shape, validate your choice by clicking on the Acquire now key. Then, choose the pricing strategy you prefer and give your references to sign up to have an account.

- Process the deal. Utilize your credit card or PayPal account to accomplish the deal.

- Choose the file format and down load the shape on your own gadget.

- Make changes. Load, revise and print out and indication the delivered electronically Ohio Construction Loan Agreement.

Every design you included with your bank account lacks an expiry particular date and it is your own property for a long time. So, if you want to down load or print out yet another duplicate, just proceed to the My Forms portion and then click around the develop you want.

Gain access to the Ohio Construction Loan Agreement with US Legal Forms, by far the most comprehensive collection of legal record templates. Use a large number of specialist and state-certain templates that fulfill your small business or individual demands and demands.