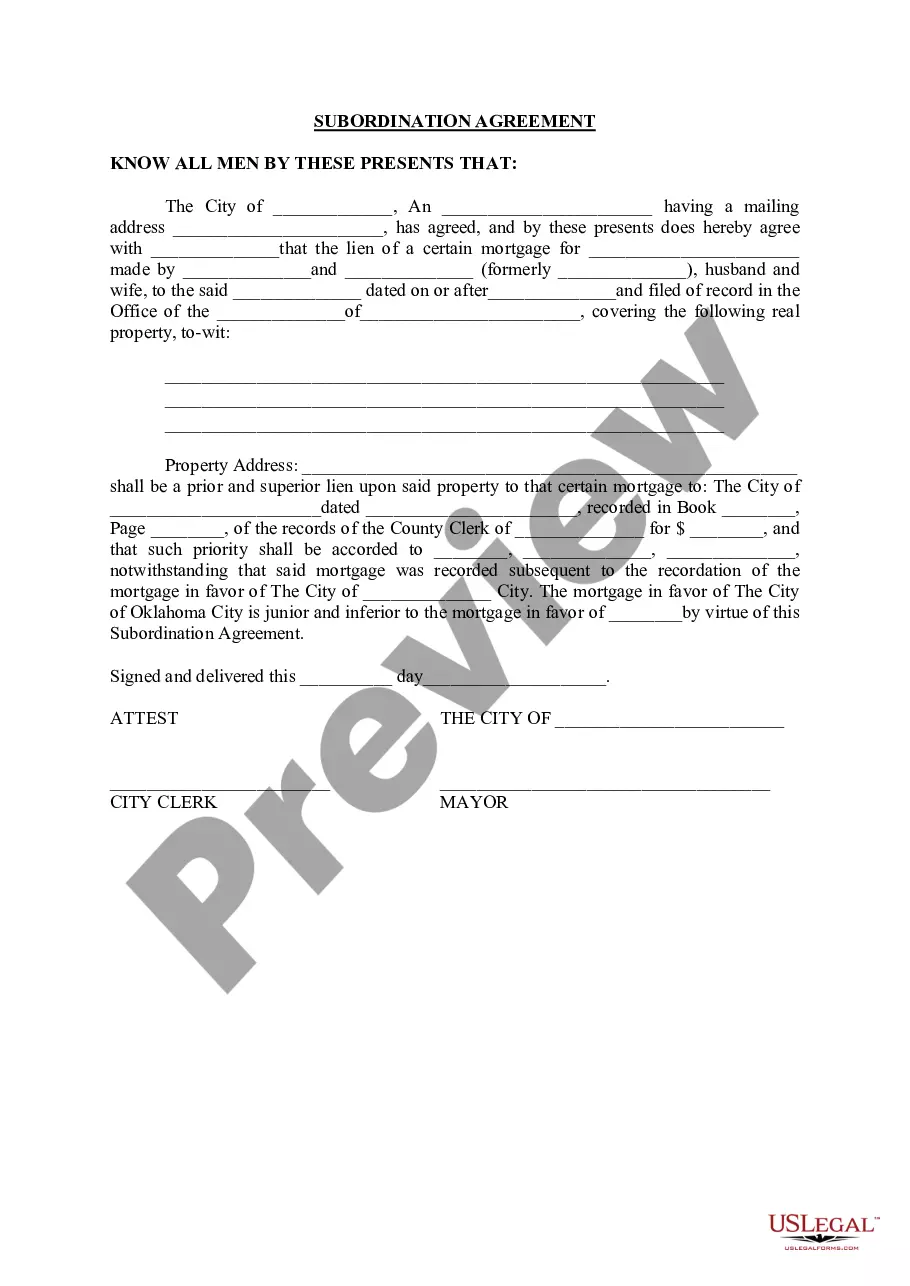

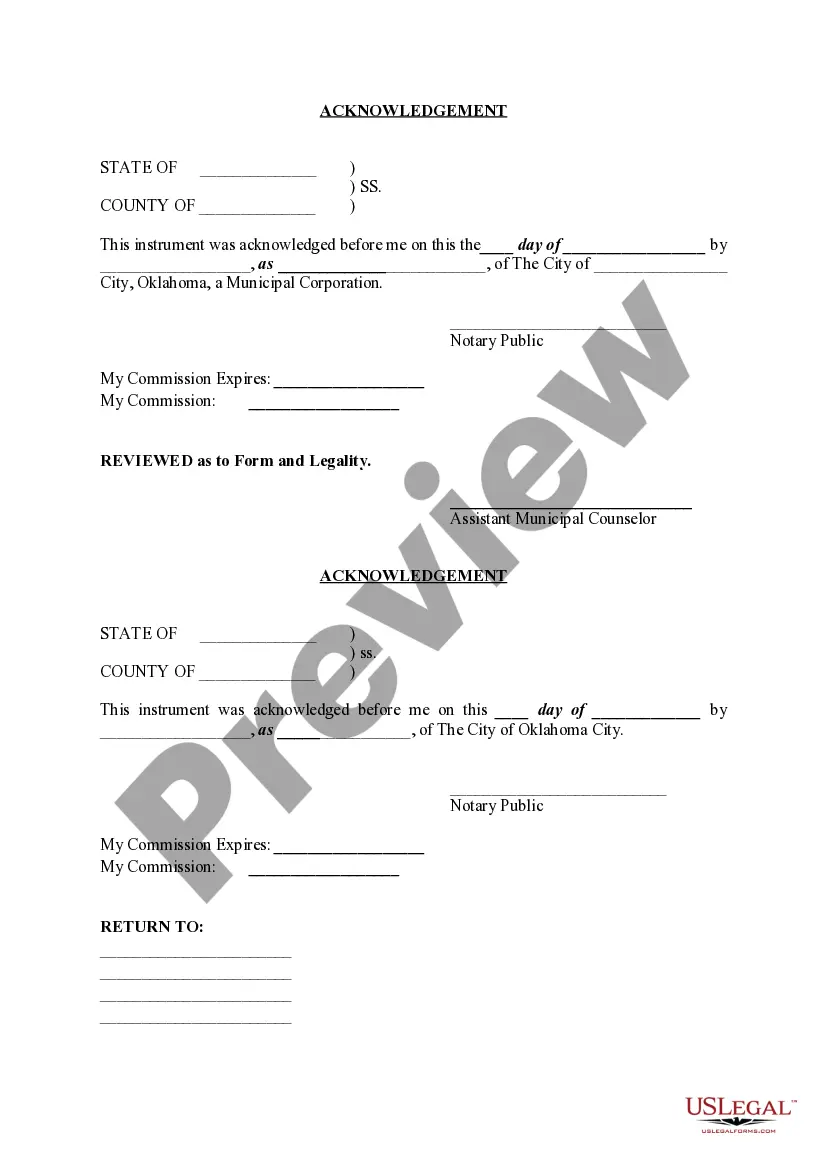

Oklahoma Subordination Agreement

Description Subordinate Loan Meaning

How to fill out Oklahoma Subordination Agreement?

In terms of submitting Oklahoma Subordination Agreement, you almost certainly imagine an extensive procedure that involves getting a ideal form among a huge selection of similar ones after which being forced to pay out an attorney to fill it out for you. Generally, that’s a slow and expensive option. Use US Legal Forms and select the state-specific document within just clicks.

In case you have a subscription, just log in and then click Download to get the Oklahoma Subordination Agreement template.

In the event you don’t have an account yet but want one, stick to the step-by-step guideline below:

- Be sure the document you’re downloading is valid in your state (or the state it’s required in).

- Do this by looking at the form’s description and by clicking the Preview function (if offered) to find out the form’s content.

- Click on Buy Now button.

- Pick the proper plan for your financial budget.

- Join an account and choose how you want to pay out: by PayPal or by credit card.

- Save the file in .pdf or .docx format.

- Find the file on the device or in your My Forms folder.

Professional legal professionals work on creating our templates to ensure after saving, you don't have to bother about editing and enhancing content outside of your personal info or your business’s info. Join US Legal Forms and receive your Oklahoma Subordination Agreement example now.

Form popularity

FAQ

Despite its technical-sounding name, the subordination agreement has one simple purpose. It assigns your new mortgage to first lien position, making it possible to refinance with a home equity loan or line of credit.

A written contract in which a lender who has secured a loan by a mortgage or deed of trust agrees with the property owner to subordinate its loan (accept a lower priority for the collection of its debt), thus giving the new loan priority in any foreclosure or payoff.

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.

But as property values are going up and the demand for refinance isn't as much, it seems that the subordination process has gotten a little easier. Typically, it takes two to three weeks to get the resubordination paperwork through, and it is likely to set you back $200 to $300.

Subordination agreements are prepared by your lender. The process occurs internally if you only have one lender. When your mortgage and home equity line or loan have different lenders, both financial institutions work together to draft the necessary paperwork.

Subordination clauses in mortgages refer to the portion of your agreement with the mortgage company that says their lien takes precedence over any other liens you may have on your property.The primary lien on a house is usually a mortgage. However, it's also possible to have other liens.

A subordination agreement often comes up when a home has a first and a second mortgage, and the borrower wants to refinance the first mortgage. If you have two mortgages on your home and refinance the first loan, the refinancing lender might require a subordination agreement.

A subordination is a process where the second lender asks the first lender if they will let go of a particular class of collateral.Where an intercreditor agreement differs from a subordination is in the way it is structured. When lenders use intercreditor agreements they both file UCC-1 financing statements.

Subordination is the tenant's agreement that its interest under the lease will be subordinate to that of the lender. Of course, in many situations, the mortgage will already be superior, depending on when the mortgage was recorded and when the lease was recorded or the tenant took possession of the property.