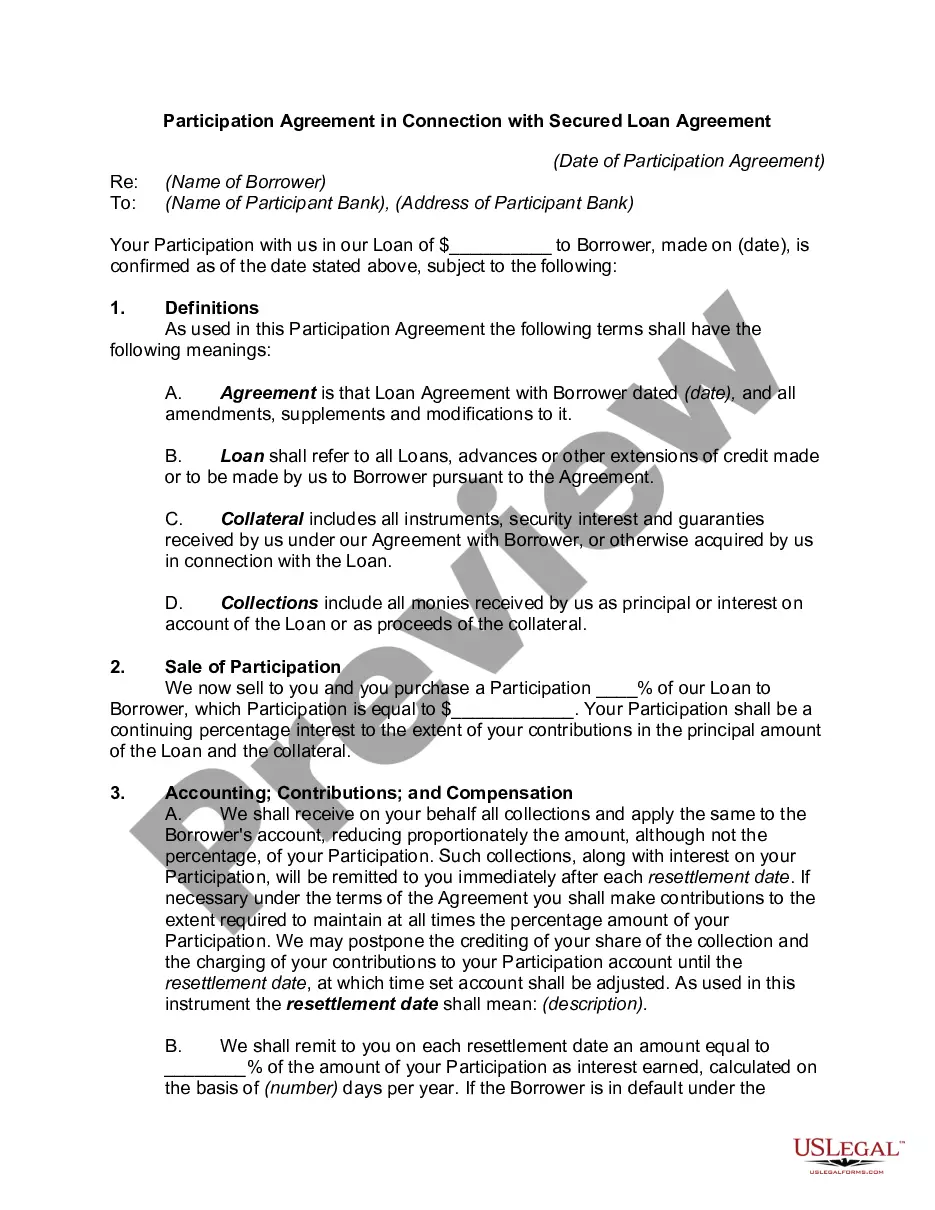

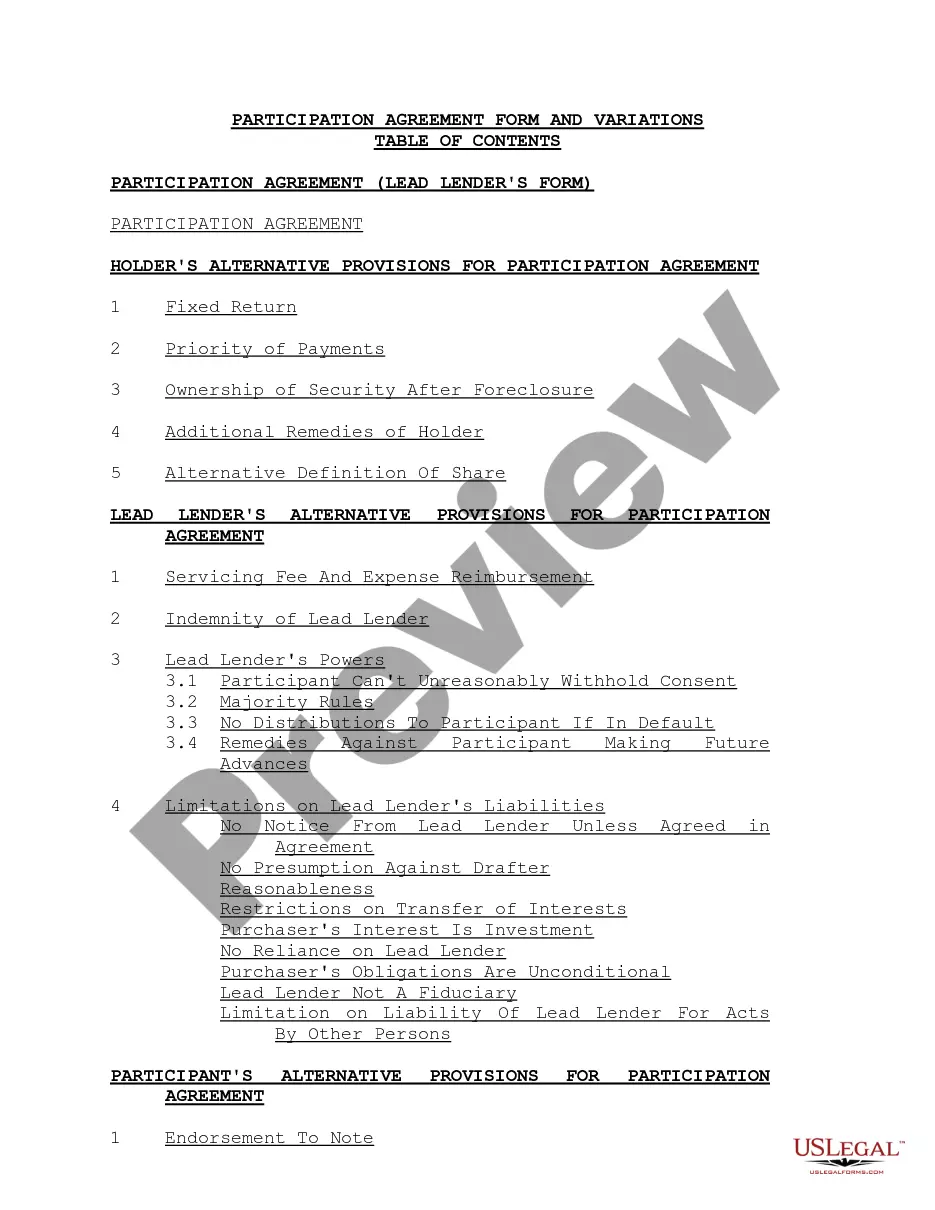

Participation loans are loans made by multiple lenders to a single borrower. Several banks, for example, might chip in to fund one extremely large loan, with one of the banks taking the role of the "lead bank." This lending institution then recruits other banks to participate and share the risks and profits. The lead bank typically originates the loan, takes responsibility for the loan servicing of the participation loan, organizes and manages the participation, and deals directly with the borrower.

Participations in the loan are sold by the lead bank to other banks. A separate contract called a loan participation agreement is structured and agreed among the banks. Loan participations can either be made with equal risk sharing for all loan participants, or on a senior/subordinated basis, where the senior lender is paid first and the subordinate loan participation paid only if there is sufficient funds left over to make the payments.