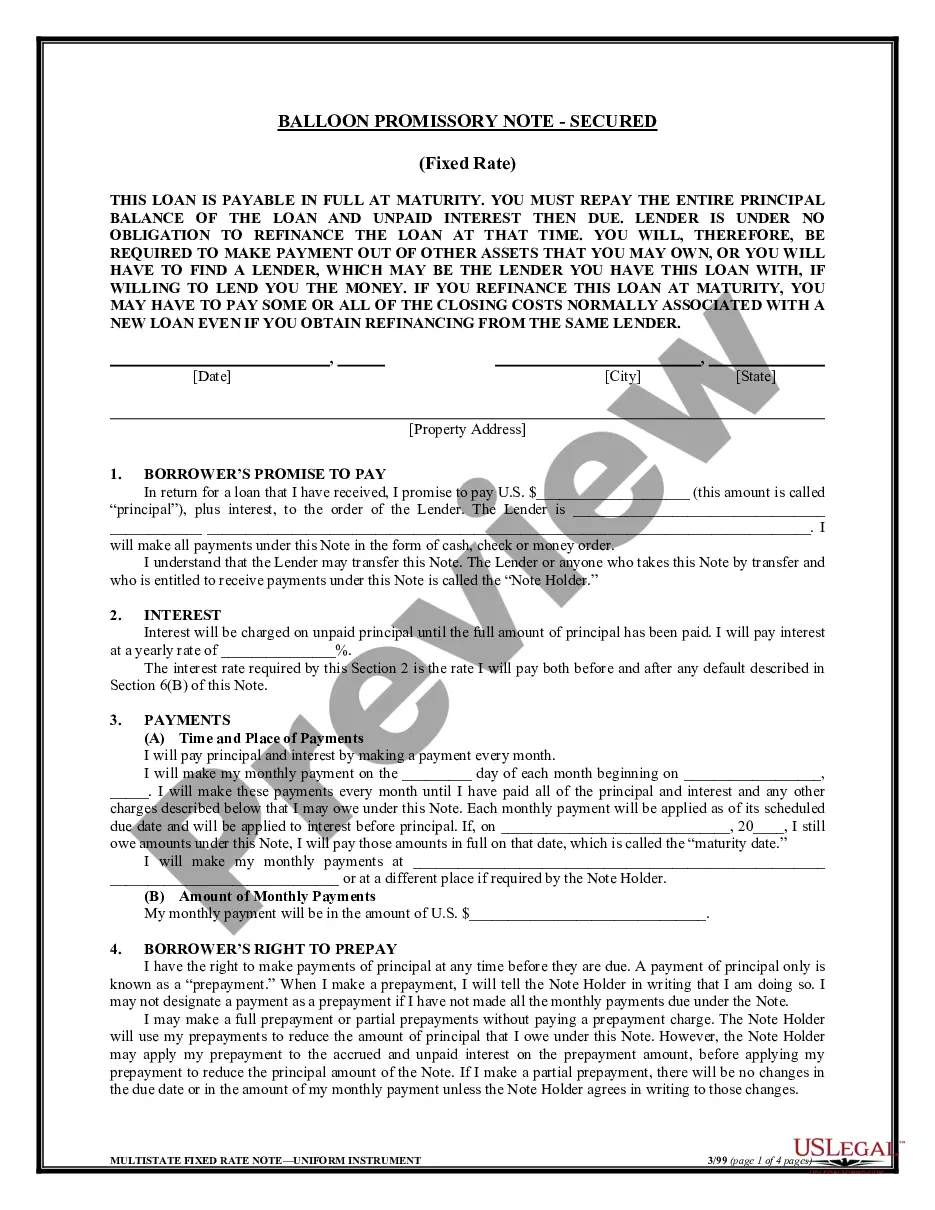

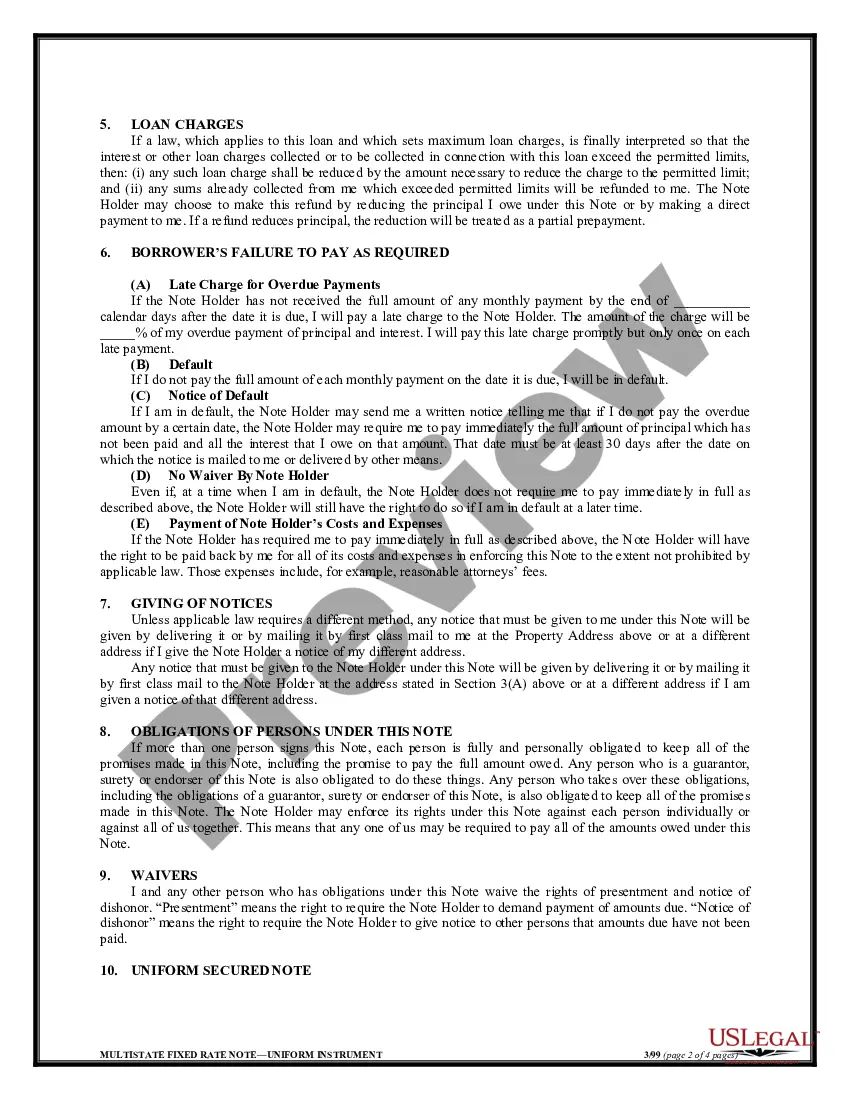

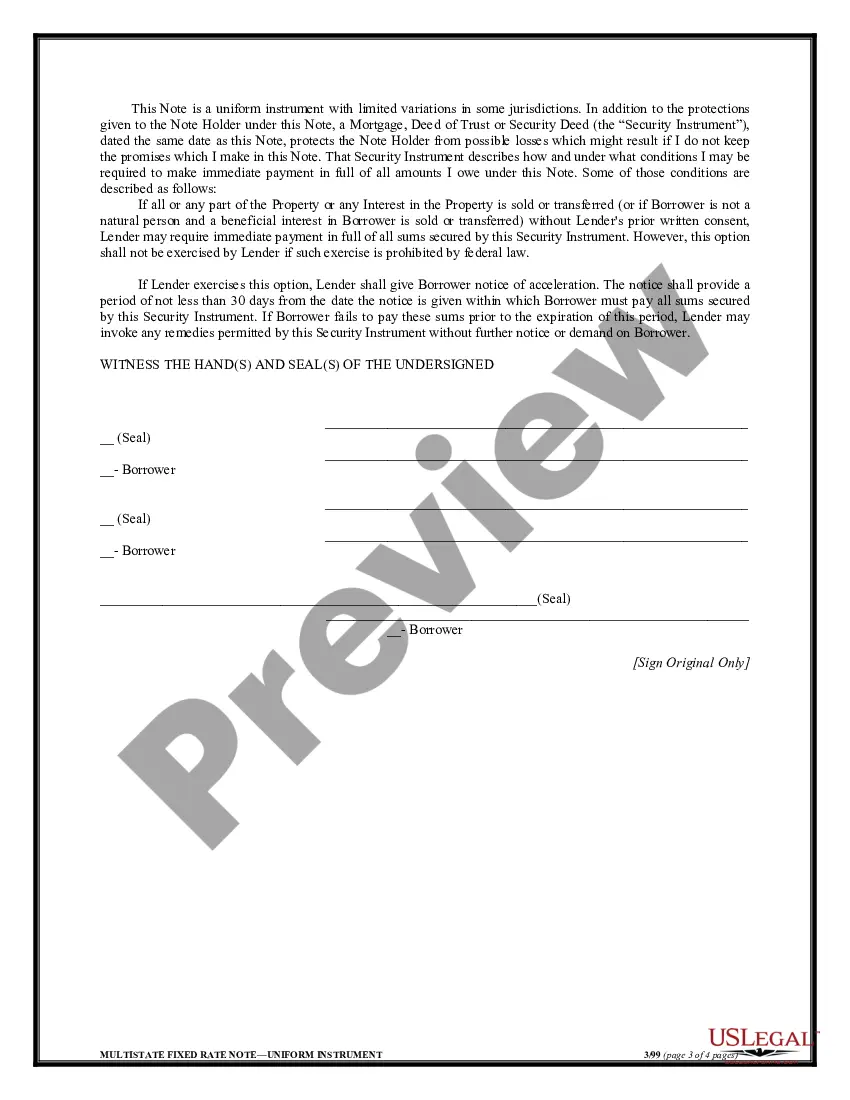

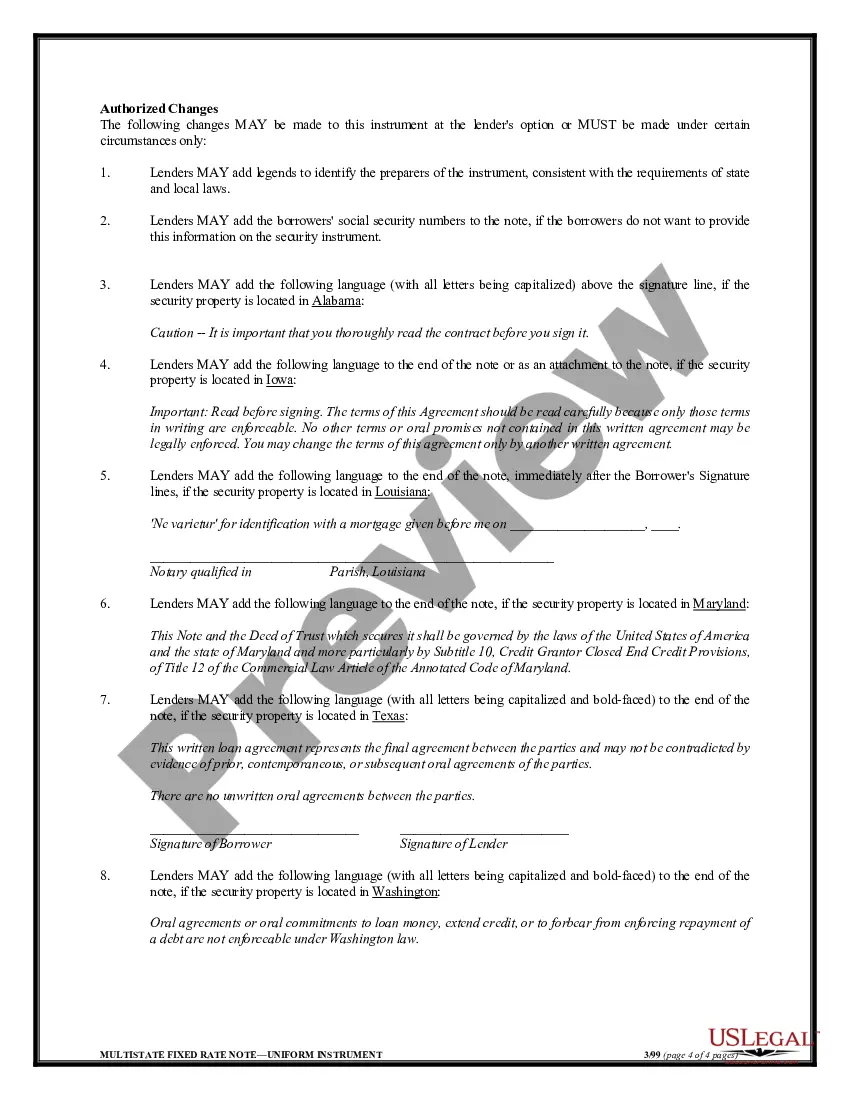

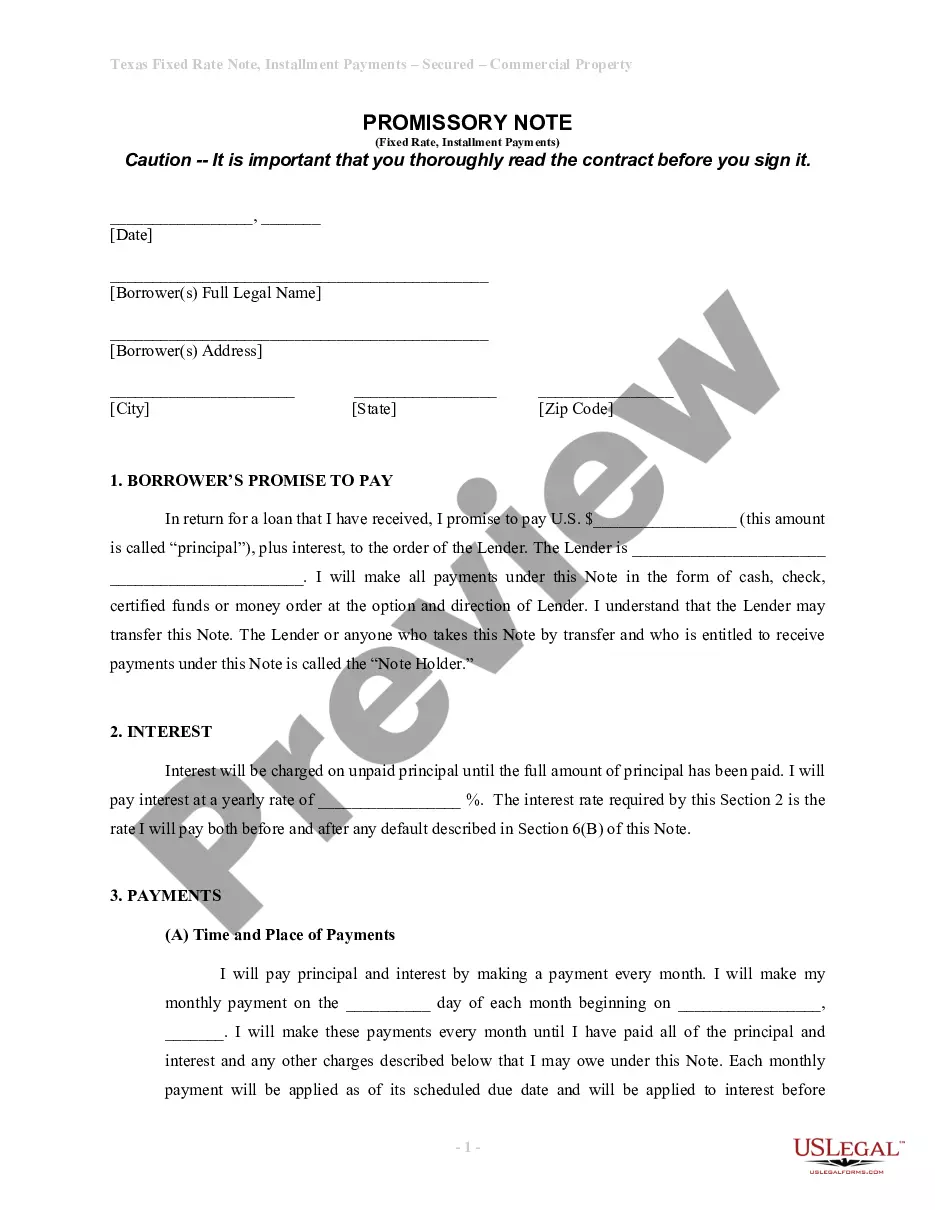

Oklahoma Balloon Secured Note is a financial instrument commonly used in real estate transactions. It functions as a promissory note in which the borrower agrees to repay the loan amount over a specified period of time, typically ranging from 5 to 30 years. The term "balloon" refers to the repayment structure of the note. While the borrower will make regular monthly payments towards the loan principal and interest, the remaining balance (or a significant portion of it) is due in one lump sum payment at the end of the loan term. This final payment is often much larger than the previous monthly payments. The balloon payment structure can be advantageous for borrowers who anticipate a significant source of funds becoming available in the future, such as property sale profits or a business venture's cash flow. It allows borrowers to make lower monthly payments throughout the loan term, which can enhance their cash flow management. However, it is essential for borrowers to consider the potential risks associated with balloon payments, such as uncertain future financial circumstances or difficulty in obtaining refinancing. If unable to make the balloon payment, borrowers may face foreclosure or have to sell the property to cover the outstanding debt. In Oklahoma, there may be different types of Balloon Secured Notes, including residential or commercial varieties. These notes can vary based on the loan amount, interest rate, loan term, and specific terms agreed upon by the lender and borrower. It is crucial for both parties to carefully review and negotiate the terms to ensure they align with their financial goals and capabilities. Keywords: Oklahoma, Balloon Secured Note, financial instrument, promissory note, real estate transactions, loan amount, repayment structure, regular monthly payments, loan principal, interest, final payment, lump sum, loan term, property sale profits, cash flow, risks, refinancing, foreclosure, residential, commercial, interest rate, negotiation.

Oklahoma Balloon Secured Note

Description

How to fill out Oklahoma Balloon Secured Note?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a variety of legal form templates you can download or print.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of forms such as the Oklahoma Balloon Secured Note in just minutes.

If you already have a subscription, Log In and download the Oklahoma Balloon Secured Note from the US Legal Forms repository. The Download button will appear on every form you view. You have access to all previously downloaded forms from the My documents section of your account.

Choose the format and download the form to your device.

Make alterations. Complete, modify, print, and sign the downloaded Oklahoma Balloon Secured Note.

- Ensure you have selected the correct form for your region/county. Click the Review button to check the form's content.

- Read the form description to confirm you have chosen the right form.

- If the form does not suit your needs, use the Search field at the top of the screen to find one that does.

- When you are happy with the form, confirm your selection by clicking the Acquire now button.

- Then, choose your preferred payment plan and provide your details to register for an account.

- Process the transaction. Use your credit card or PayPal account to finalize the transaction.

Form popularity

FAQ

Balloon mortgages were far more common before the 2008-09 financial crisis. These days, most mortgages are 15- or 30-year loans with fixed interest rates. But balloon mortgages still exist.

Balloon payments are often packaged into two-step mortgages. In a "balloon payment mortgage," the borrower pays a set interest rate for a certain number of years. Then, the loan then resets and the balloon payment rolls into a new or continuing amortized mortgage at the prevailing market rates at the end of that term.

You can handle a balloon payment in several different ways.Refinance: When the balloon payment is due, one option is to pay it off by obtaining another loan.Sell the asset: Another option for dealing with a balloon payment is to sell whatever you bought with the loan.More items...

A Promissory Note with Balloon Payments is a loan contract that enables a lender set loan terms with one or more larger payments at the end. This lending document helps you to clarify the terms of a loan, define the payment schedule, and provide an amortization table, if the loan includes interest.

Here are a few ways that you can get out of a balloon car payment:Sell your car and use the profit to pay off the loan.Pay the loan in full.Refinance the loan to extend your loan repayment period and even out the remaining monthly payments.

If you don't have the funds to settle your balloon payment and if you don't qualify for credit for refinancing, then you risk repossession. This could also get you blacklisted. It's more expensive.

What Happens When the Balloon Payment Is Due? When your balloon payment is due, you have two choices to pay it off: You can take out another mortgage for the amount of the balloon payment or you can sell your home and use the proceeds to pay it off.

A balloon payment provision in a loan is not illegal per se. Federal and state legislatures have enacted various laws designed to protect consumers from being victimized by such a loan. The Federal TRUTH IN LENDING ACT (15U.

What is a balloon note payment? This is a large payment due at the end of a loan that will pay off the balance. It is often equal to around two times the average monthly payment of the loan. It doesn't matter the amount that is due; you are required to pay the entire balloon payment when it's due.

A balloon mortgage may be a good idea if: You know with a high degree of certainty that you aren't going to still be in the property when the balloon payment comes due. You expect, again with a great deal of confidence, that you're going to receive a lump sum at least equal to the balloon payment that will come due