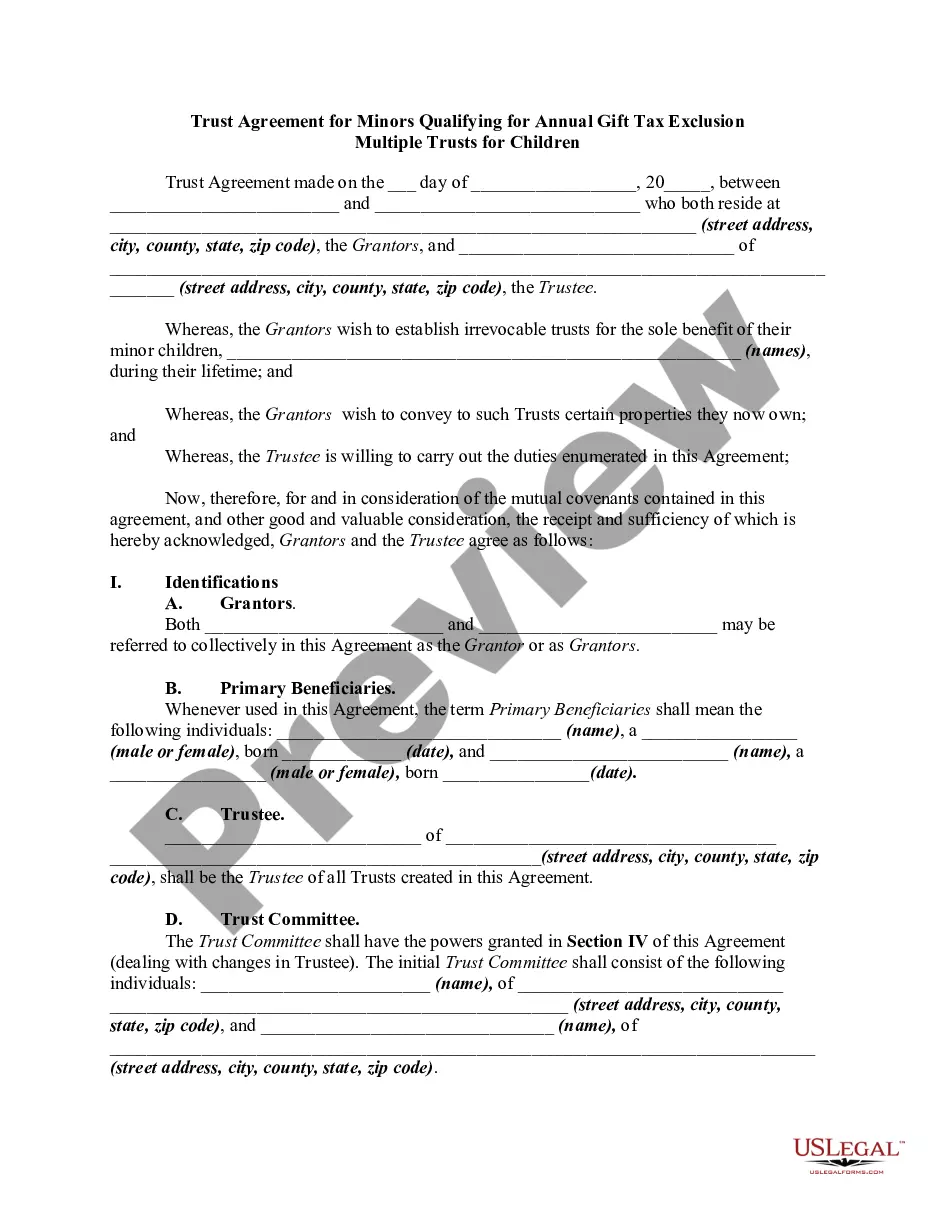

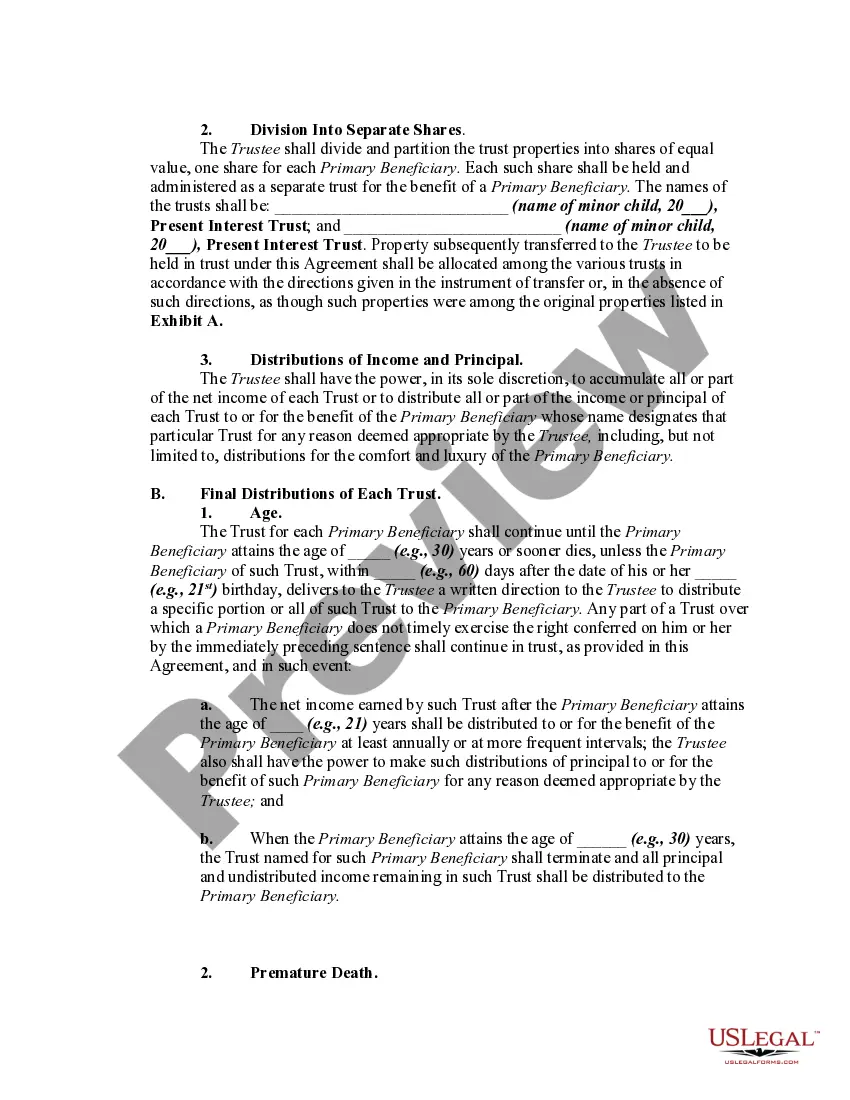

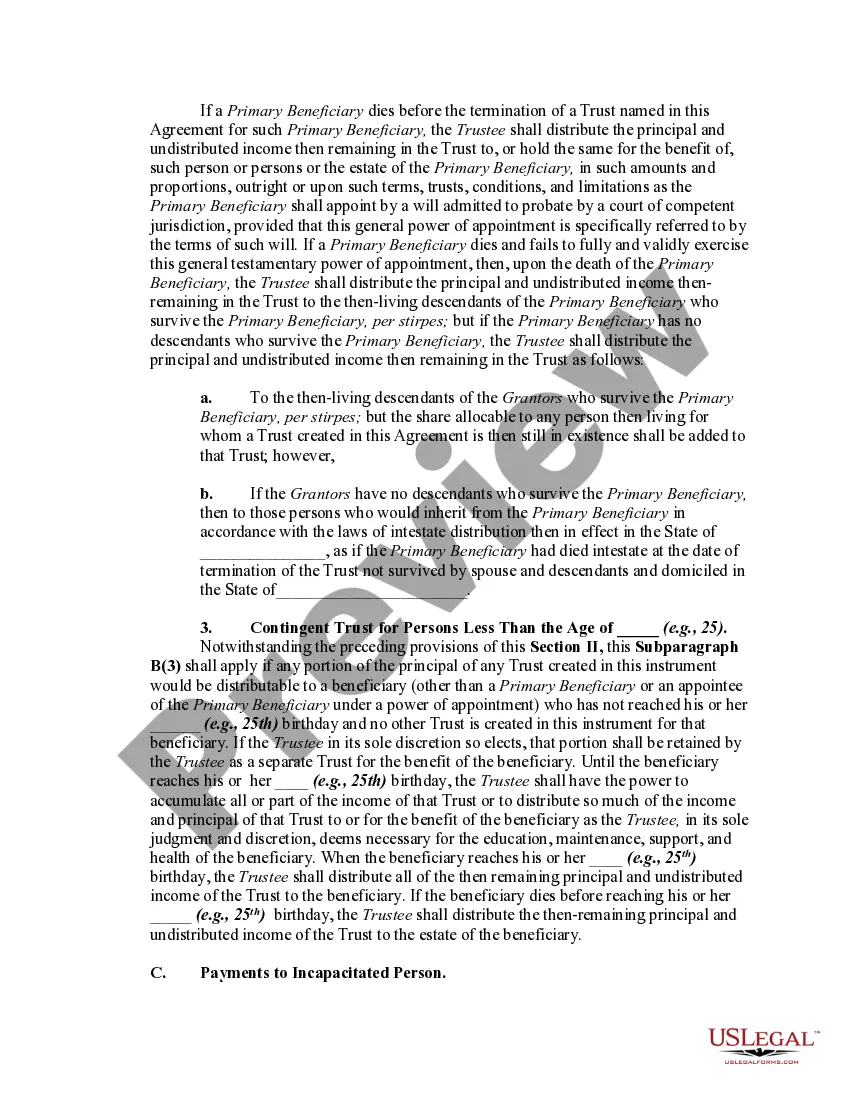

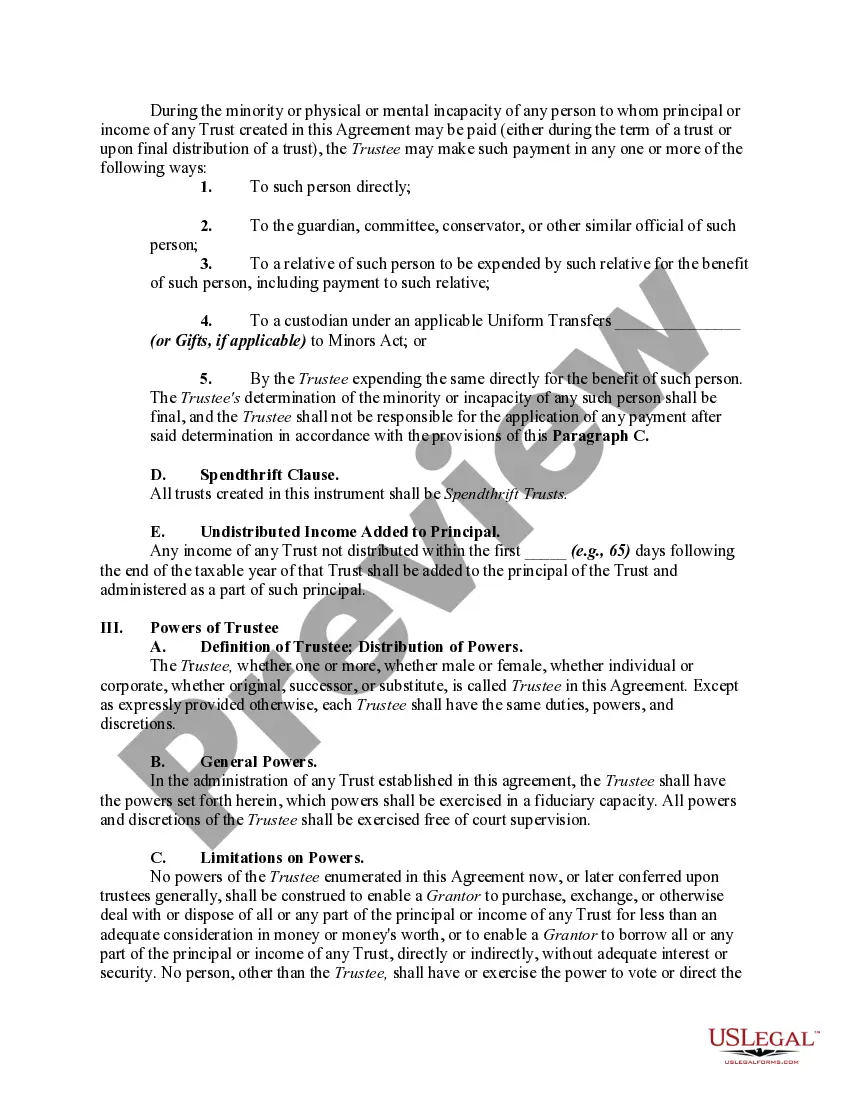

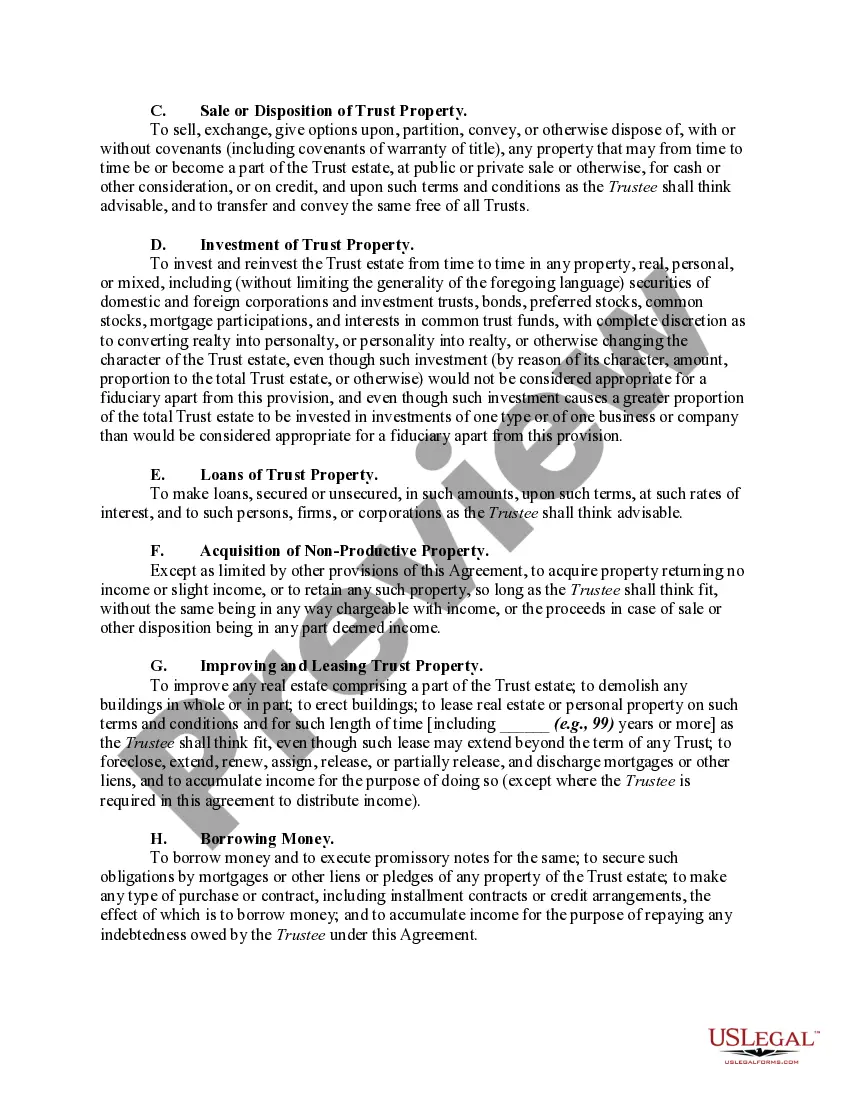

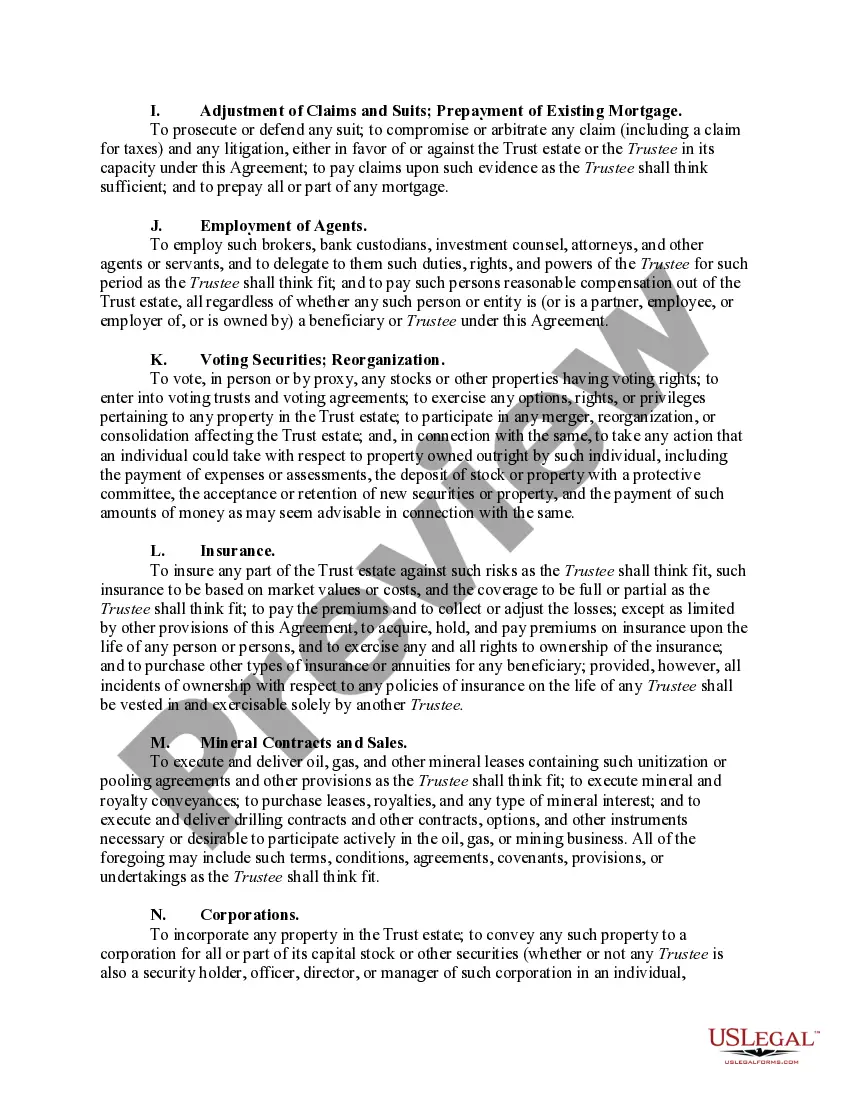

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

Title: Understanding the Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children Introduction: The Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion allows individuals to establish multiple trusts for children while availing annual gift tax exclusions. This legal document ensures that minors' assets are protected and managed effectively, while minimizing potential tax burdens for the granter. In this article, we will delve into the details of the Oklahoma Trust Agreement for Minors, exploring its purpose, requirements, and different types of trusts available. Key Keywords: Oklahoma Trust Agreement, Minor, Annual Gift Tax Exclusion, Multiple Trusts for Children 1. Purpose and Benefits: The Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion serves multiple purposes, including: — Protecting and managing assets for minors until they reach a certain age of maturity. — Ensuring tax advantages fograntersrs by utilizing the annual gift tax exclusion. — Authorizing a designated trustee to handle the trust's financial affairs on behalf of the minor. — Preserving thgranteror's intentions and guiding the distribution of assets to beneficiaries. 2. Requirements for Qualification: To establish an Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion, certain requirements must be met, including: — The trust must be created specifically for the benefit of a minor or minors. — It must adhere to the guidelines set forth by the Internal Revenue Service (IRS) regarding annual gift tax exclusions. — Trustees must be named to oversee the management and distribution of trust assets. — The trust agreement should clearly outline the terms and conditions for asset distribution to minors. 3. Different Types of Oklahoma Trust Agreements for Minors: There are several variations of the Oklahoma Trust Agreement that cater to different circumstances, each serving a distinct purpose within the realm of minor trusts. Some common types include: a) Crummy Trust: This type of trust allows the granter to contribute gifts up to the annual gift tax exclusion limit. It is named after the Crummy v. Commissioner court case, which established the legitimacy of this type of trust structure. b) Revocable Living Trust: Also known as a family trust, this type of trust enables the granter to maintain control over trust assets during their lifetime. Upon their passing, it becomes irrevocable, ensuring that the assets are distributed according to the trust's terms. c) Irrevocable Minor's Trust: This trust provides a durable solution for minors, as it cannot be altered or revoked by the granter once established. It guarantees that assets are safeguarded until the child reaches a specified age of distribution. d) Testamentary Trust: Created under a will, this trust comes into effect upon the granter's death. It specifies how the assets will be administered and distributed to minors, allowing for maximum control over their inheritance. Conclusion: Creating an Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children offers numerous benefits to both granters and beneficiaries. By understanding the purpose, requirements, and different types of trusts available, individuals can make informed decisions when planning for the financial future of minors. Professional legal advice is recommended to ensure compliance with applicable laws and regulations.Title: Understanding the Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children Introduction: The Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion allows individuals to establish multiple trusts for children while availing annual gift tax exclusions. This legal document ensures that minors' assets are protected and managed effectively, while minimizing potential tax burdens for the granter. In this article, we will delve into the details of the Oklahoma Trust Agreement for Minors, exploring its purpose, requirements, and different types of trusts available. Key Keywords: Oklahoma Trust Agreement, Minor, Annual Gift Tax Exclusion, Multiple Trusts for Children 1. Purpose and Benefits: The Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion serves multiple purposes, including: — Protecting and managing assets for minors until they reach a certain age of maturity. — Ensuring tax advantages fograntersrs by utilizing the annual gift tax exclusion. — Authorizing a designated trustee to handle the trust's financial affairs on behalf of the minor. — Preserving thgranteror's intentions and guiding the distribution of assets to beneficiaries. 2. Requirements for Qualification: To establish an Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion, certain requirements must be met, including: — The trust must be created specifically for the benefit of a minor or minors. — It must adhere to the guidelines set forth by the Internal Revenue Service (IRS) regarding annual gift tax exclusions. — Trustees must be named to oversee the management and distribution of trust assets. — The trust agreement should clearly outline the terms and conditions for asset distribution to minors. 3. Different Types of Oklahoma Trust Agreements for Minors: There are several variations of the Oklahoma Trust Agreement that cater to different circumstances, each serving a distinct purpose within the realm of minor trusts. Some common types include: a) Crummy Trust: This type of trust allows the granter to contribute gifts up to the annual gift tax exclusion limit. It is named after the Crummy v. Commissioner court case, which established the legitimacy of this type of trust structure. b) Revocable Living Trust: Also known as a family trust, this type of trust enables the granter to maintain control over trust assets during their lifetime. Upon their passing, it becomes irrevocable, ensuring that the assets are distributed according to the trust's terms. c) Irrevocable Minor's Trust: This trust provides a durable solution for minors, as it cannot be altered or revoked by the granter once established. It guarantees that assets are safeguarded until the child reaches a specified age of distribution. d) Testamentary Trust: Created under a will, this trust comes into effect upon the granter's death. It specifies how the assets will be administered and distributed to minors, allowing for maximum control over their inheritance. Conclusion: Creating an Oklahoma Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children offers numerous benefits to both granters and beneficiaries. By understanding the purpose, requirements, and different types of trusts available, individuals can make informed decisions when planning for the financial future of minors. Professional legal advice is recommended to ensure compliance with applicable laws and regulations.