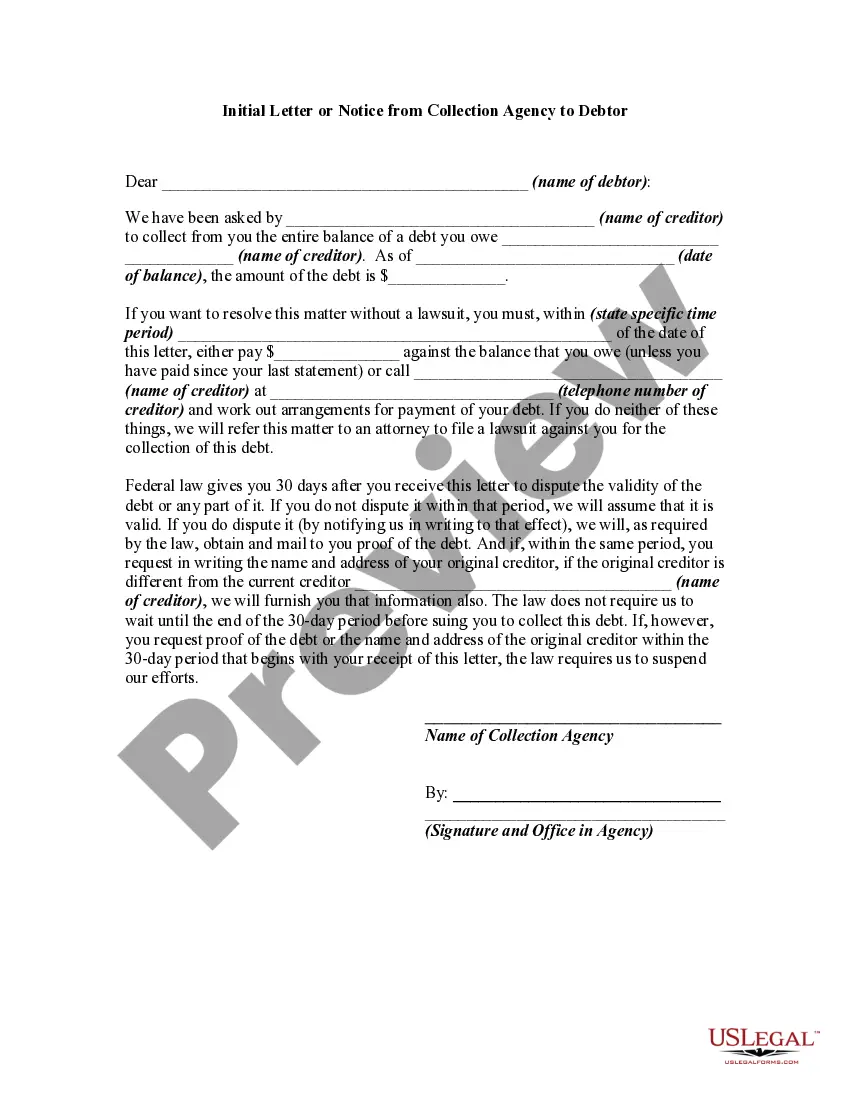

The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representa?¬tions are forbidden, such as representing that the debt collector is associated with the state or federal government, or stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

The FDCPA applies only to those who regularly engage in the business of collecting debts for others -- primarily to collection agencies. The Act does not apply when a creditor attempts to collect debts owed to it by directly contacting the debtors. It applies only to the collection of consumer debts and does not apply to the collection of commercial debts. Consumer debts are debts for personal, home, or family purposes.

Title: Comprehensive Guide to Oklahoma Initial Letter or Notice from Collection Agency to Debtor Introduction: When it comes to debt collection in Oklahoma, it is essential for collection agencies to adhere to specific guidelines and regulations set forth by the state. One important requirement is providing debtors with an initial letter or notice, informing them of the collection attempt and their rights. In this article, we will delve into the details of what an Oklahoma Initial Letter or Notice from Collection Agency to Debtor entails, covering its purpose, content, and variations. Purpose of Oklahoma Initial Letter or Notice: An Oklahoma Initial Letter or Notice from a Collection Agency serves multiple purposes. Firstly, it acts as a communication tool, informing debtors that they owe a certain amount of money to a particular creditor and that the collection agency has been entrusted to collect the debt. Secondly, it aims to educate debtors about their rights outlined under the Fair Debt Collection Practices Act (FD CPA) to ensure fair treatment during the collection process. Content of an Oklahoma Initial Letter or Notice: 1. Identification: The letter should clearly identify the collection agency, including its name, address, and contact information. 2. Debtor Information: The notice must include the name of the debtor, any associated account numbers, and the total amount owed, including interest, fees, and any applicable charges. 3. Creditor Information: The letter should identify the original creditor, providing details such as the creditor's name, contact information, and the original account number. 4. Validation of Debt: The notice should inform debtors that they have the right to request validation of the debt within 30 days of receiving the letter. It should also specify the process to follow to dispute the debt. 5. Cease and Desist Option: The letter must inform debtors of their right to request the collection agency to cease further communication attempts by sending a written notice. This ensures compliance with the FD CPA if the debtor wishes to halt future contact. 6. Legal Actions: If applicable, the letter should state that failure to resolve the debt may result in legal action, providing a general outline of the potential consequences. Types of Oklahoma Initial Letters or Notices: 1. Standard Initial Letter: This is the most common type of initial letter sent to debtors in Oklahoma. It includes all the essential elements described above. 2. Specific Account Notice: In cases where a debtor has multiple accounts with the same collection agency, these notices may be sent separately to provide a clearer breakdown of each debt and the corresponding creditor. 3. Final Notice: If previous attempts to contact the debtor have been unsuccessful or the debt is nearing the statute of limitations, the collection agency may send a final notice before taking legal action or closing the case. Conclusion: Oklahoma Initial Letters or Notices from Collection Agencies are critical for debt recovery while ensuring debtors are informed of their rights. By including comprehensive information and complying with relevant state and federal laws, collection agencies can establish effective communication channels with debtors and work towards potential debt resolution.