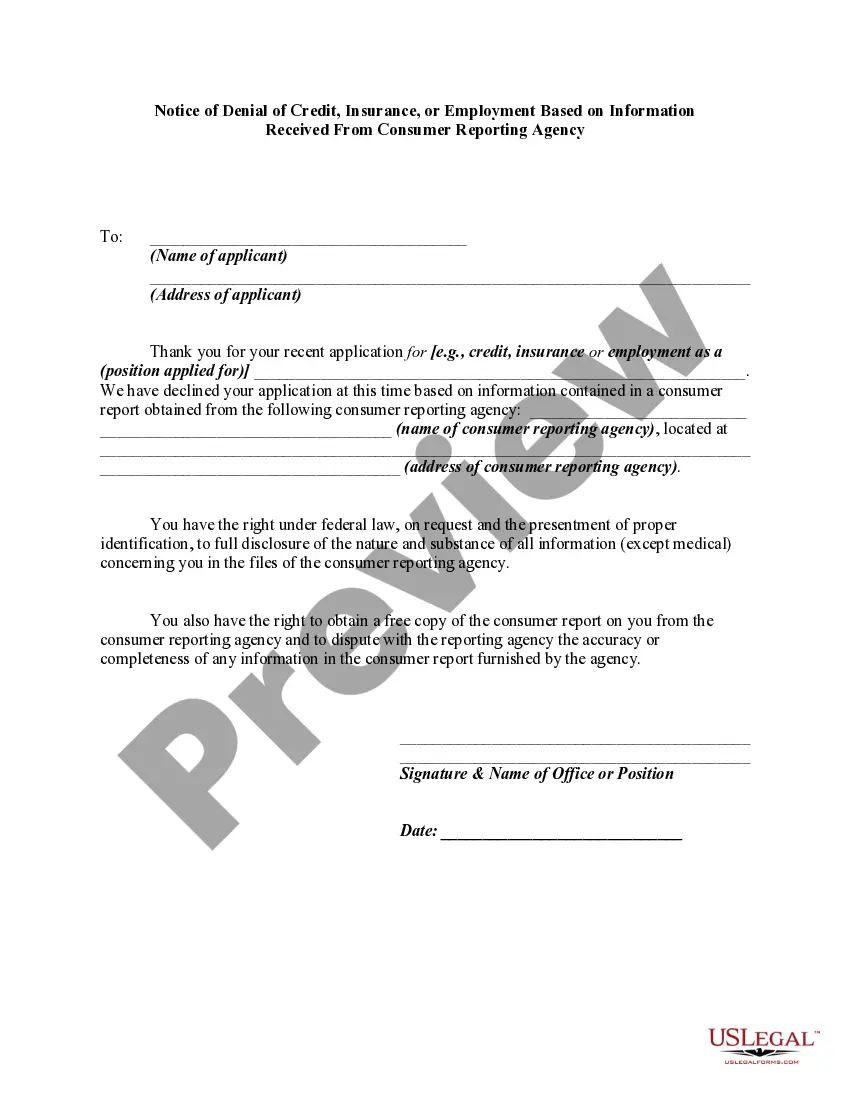

Under the federal Equal Credit Opportunity Act, a creditor must notify a consumer applicant for credit of the reasons for any adverse action taken on the application, and must make certain disclosures to the consumer concerning the applicant's rights and the provisions of federal law prohibiting discrimination in credit opportunities.

Oklahoma Notice of Denial of Credit, Insurance, or Employment Based on Information Received from Consumer Reporting Agency is a legal document that informs individuals about their denial of credit, insurance, or employment based on information obtained from a consumer reporting agency. This notice is crucial for ensuring transparency and compliance with relevant laws, such as the Fair Credit Reporting Act (FCRA) and the Oklahoma Consumer Credit Code. The Oklahoma Notice of Denial of Credit, Insurance, or Employment typically includes important details like the date, the recipient's name and address, and the specific reasons for the denial. The notice also discloses the name, address, and contact information of the consumer reporting agency responsible for providing the negative information. It's important to note that there may be different types of Oklahoma Notice of Denial of Credit, Insurance, or Employment forms based on the specific context and type of denial. For instance, there could be separate notices for credit denials, insurance denials, and employment denials. Each of these notices would include specific information relevant to the particular denial, such as credit score ranges, insurance coverage details, or employment history. In case of credit denials, the notice might specify the credit reporting agency's name and address, along with the credit score used to evaluate the applicant's creditworthiness. It could also mention the adverse factors contributing to the denial, such as recent late payments, high credit utilization, or bankruptcies. For insurance denials, the notice might provide details regarding the consumer reporting agency providing the negative information, the specific insurance coverage requested, and the adverse factors leading to the denial. These factors could include an individual's medical history, driving records, or past insurance claims. In the context of employment denials, the notice may disclose the consumer reporting agency's name, address, and contact information. It could also outline the adverse employment history or background check records that influenced the decision. These records may consist of criminal history, past employment discrepancies, or any negative public records. In conclusion, the Oklahoma Notice of Denial of Credit, Insurance, or Employment Based on Information Received from Consumer Reporting Agency is a crucial document in ensuring transparency and compliance. It informs individuals about the denial of credit, insurance, or employment based on information obtained from consumer reporting agencies, and it may vary based on the specific type of denial.Oklahoma Notice of Denial of Credit, Insurance, or Employment Based on Information Received from Consumer Reporting Agency is a legal document that informs individuals about their denial of credit, insurance, or employment based on information obtained from a consumer reporting agency. This notice is crucial for ensuring transparency and compliance with relevant laws, such as the Fair Credit Reporting Act (FCRA) and the Oklahoma Consumer Credit Code. The Oklahoma Notice of Denial of Credit, Insurance, or Employment typically includes important details like the date, the recipient's name and address, and the specific reasons for the denial. The notice also discloses the name, address, and contact information of the consumer reporting agency responsible for providing the negative information. It's important to note that there may be different types of Oklahoma Notice of Denial of Credit, Insurance, or Employment forms based on the specific context and type of denial. For instance, there could be separate notices for credit denials, insurance denials, and employment denials. Each of these notices would include specific information relevant to the particular denial, such as credit score ranges, insurance coverage details, or employment history. In case of credit denials, the notice might specify the credit reporting agency's name and address, along with the credit score used to evaluate the applicant's creditworthiness. It could also mention the adverse factors contributing to the denial, such as recent late payments, high credit utilization, or bankruptcies. For insurance denials, the notice might provide details regarding the consumer reporting agency providing the negative information, the specific insurance coverage requested, and the adverse factors leading to the denial. These factors could include an individual's medical history, driving records, or past insurance claims. In the context of employment denials, the notice may disclose the consumer reporting agency's name, address, and contact information. It could also outline the adverse employment history or background check records that influenced the decision. These records may consist of criminal history, past employment discrepancies, or any negative public records. In conclusion, the Oklahoma Notice of Denial of Credit, Insurance, or Employment Based on Information Received from Consumer Reporting Agency is a crucial document in ensuring transparency and compliance. It informs individuals about the denial of credit, insurance, or employment based on information obtained from consumer reporting agencies, and it may vary based on the specific type of denial.