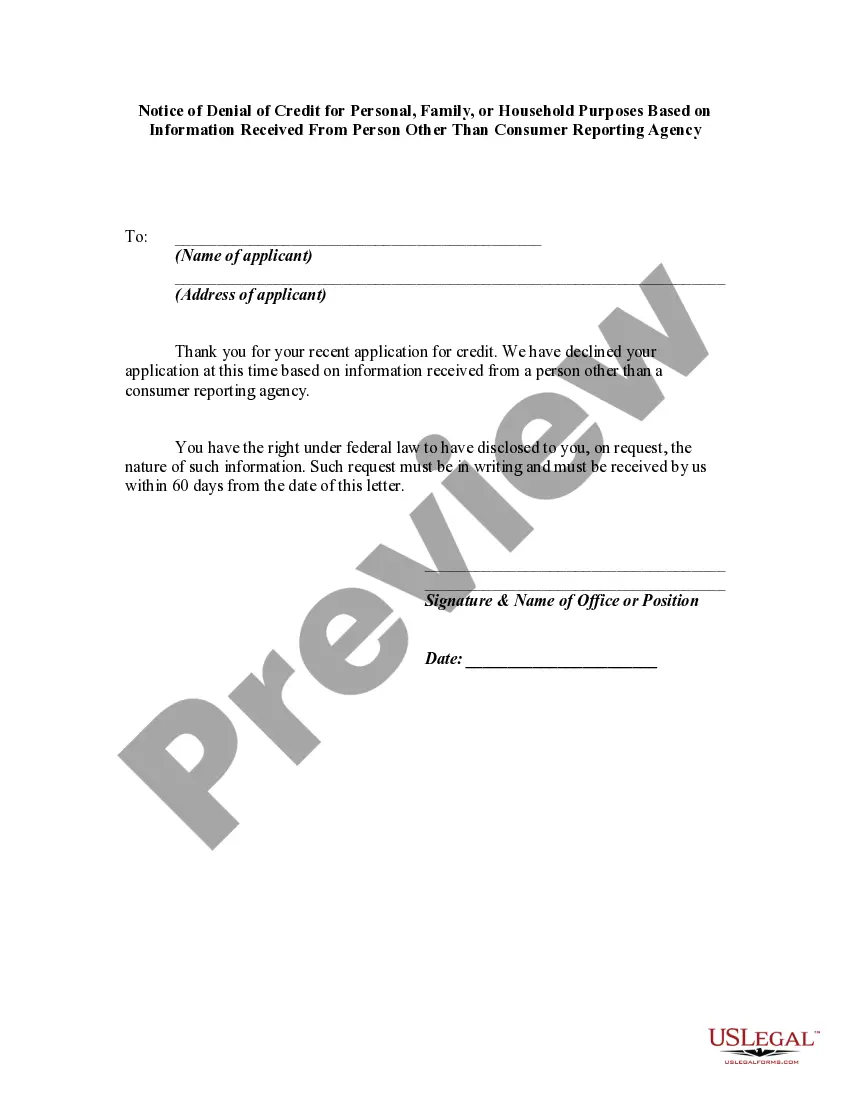

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a formal document that outlines the reasons behind the rejection of an individual's credit application. This notice is based on information provided by someone other than a consumer reporting agency, such as a reference or personal acquaintance. The purpose of this notice is to inform the applicant about the grounds on which their credit request was denied. It is crucial for individuals to understand the reasons behind their denial to rectify any potential inaccuracies or work on improving their financial situation. By providing a detailed description of the denial, applicants have the opportunity to address any concerns and take the necessary steps towards securing credit in the future. There are various types of Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency. These may include: 1. General Denial Notice: This type of notice is sent when an individual's credit application is denied based on negative information received from a person other than a consumer reporting agency. It provides a broad overview of the reasons for denial without going into specific details. 2. Detailed Denial Notice: In some cases, the notice may contain a more comprehensive explanation of the reasons for the denial. This type of notice offers specific information regarding the negative factors that influenced the credit decision. 3. Corrective Action Denial Notice: If the denial is due to incorrect or outdated information received from a person other than a consumer reporting agency, this notice informs the applicant about the need for corrective actions. It may include guidance on how to rectify the inaccuracies and steps to take towards improving creditworthiness. 4. Adverse Factors Notice: This type of notice highlights specific factors that negatively impacted the credit decision, such as excessive debt, missed payments, or a high debt-to-income ratio. It aims to provide insights into the specific aspects that need improvement for future credit applications. 5. Disclosure Notice: This notice focuses on providing a disclosure of information received from a person other than a consumer reporting agency, which was used to evaluate the application. It aims to ensure transparency and allows the individual to review and address any discrepancies or errors in the provided information. In conclusion, the Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency plays a pivotal role in informing applicants about the reasons behind their credit rejection. By understanding the grounds for denial, individuals can take appropriate measures to rectify inaccuracies, address adverse factors, and work towards improving their financial standing for future credit opportunities.Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is a formal document that outlines the reasons behind the rejection of an individual's credit application. This notice is based on information provided by someone other than a consumer reporting agency, such as a reference or personal acquaintance. The purpose of this notice is to inform the applicant about the grounds on which their credit request was denied. It is crucial for individuals to understand the reasons behind their denial to rectify any potential inaccuracies or work on improving their financial situation. By providing a detailed description of the denial, applicants have the opportunity to address any concerns and take the necessary steps towards securing credit in the future. There are various types of Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency. These may include: 1. General Denial Notice: This type of notice is sent when an individual's credit application is denied based on negative information received from a person other than a consumer reporting agency. It provides a broad overview of the reasons for denial without going into specific details. 2. Detailed Denial Notice: In some cases, the notice may contain a more comprehensive explanation of the reasons for the denial. This type of notice offers specific information regarding the negative factors that influenced the credit decision. 3. Corrective Action Denial Notice: If the denial is due to incorrect or outdated information received from a person other than a consumer reporting agency, this notice informs the applicant about the need for corrective actions. It may include guidance on how to rectify the inaccuracies and steps to take towards improving creditworthiness. 4. Adverse Factors Notice: This type of notice highlights specific factors that negatively impacted the credit decision, such as excessive debt, missed payments, or a high debt-to-income ratio. It aims to provide insights into the specific aspects that need improvement for future credit applications. 5. Disclosure Notice: This notice focuses on providing a disclosure of information received from a person other than a consumer reporting agency, which was used to evaluate the application. It aims to ensure transparency and allows the individual to review and address any discrepancies or errors in the provided information. In conclusion, the Oklahoma Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency plays a pivotal role in informing applicants about the reasons behind their credit rejection. By understanding the grounds for denial, individuals can take appropriate measures to rectify inaccuracies, address adverse factors, and work towards improving their financial standing for future credit opportunities.