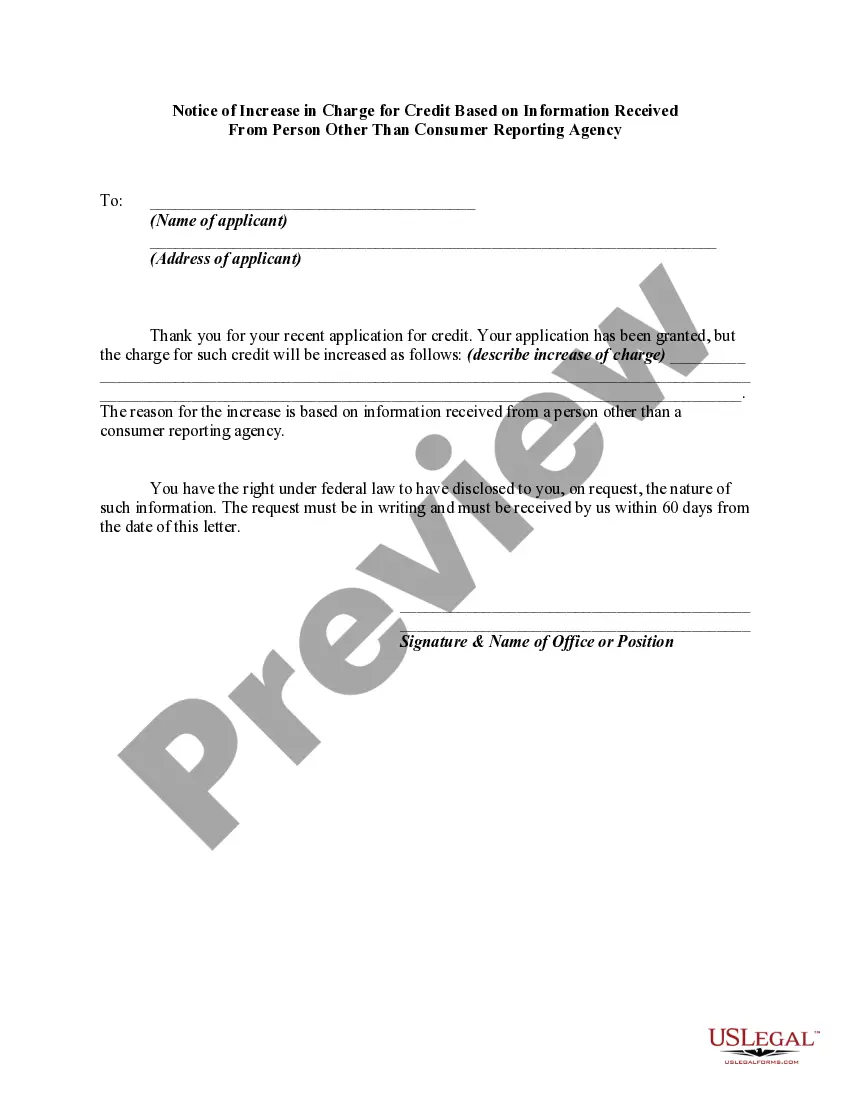

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is an important document used by credit issuers to inform consumers in Oklahoma about changes in their credit terms. This notice is specifically applicable when the credit issuer makes a decision to increase charges based on information received from a non-consumer reporting agency. This could include obtaining information about the consumer's creditworthiness from sources such as an employer, a landlord, or a credit reference. This document serves as a legal notification to the consumer, ensuring transparency and compliance with Oklahoma laws. The notice will outline the specific reasons and details of the increase in charges, providing consumers with an opportunity to review and assess the changes. It is crucial for consumers to carefully read and understand the content of this notice to remain informed about their credit obligations. It's also important to note that there can be different types of Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency, depending on the nature of the credit account and the credit issuer involved. Some specific types of notices could include: 1. Credit Card Notice: This type of notice is specifically related to credit card accounts, where the credit issuer informs the consumer about an increase in charges based on information received from a non-consumer reporting agency. The notice will detail the new charges applicable to the credit card account and any other relevant information that consumers need to be aware of. 2. Personal Loan Notice: This type of notice is relevant to personal loans or installment loans. It is issued when the credit issuer decides to increase the charges associated with the loan based on information obtained from a source other than a consumer reporting agency. Consumers will receive a detailed explanation of the increased charges and any other relevant terms of the loan. 3. Mortgage Notice: For consumers with a mortgage, this type of notice will be sent if the credit issuer decides to raise charges based on information received from a non-consumer reporting agency. The notice will inform the consumer about the new terms, including changes in interest rates, payment amounts, or any other pertinent information. 4. Auto Loan Notice: If a consumer has an auto loan and the credit issuer determines an increase in charges based on information obtained from a non-consumer reporting agency, this notice will be issued. It will provide detailed information about the revised terms, such as a higher interest rate or increased monthly payments. In conclusion, the Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a crucial document that credit issuers use to inform consumers about changes in their credit terms. By receiving this notice, consumers can stay informed about the adjustments in charges and evaluate the impact on their credit obligations.Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is an important document used by credit issuers to inform consumers in Oklahoma about changes in their credit terms. This notice is specifically applicable when the credit issuer makes a decision to increase charges based on information received from a non-consumer reporting agency. This could include obtaining information about the consumer's creditworthiness from sources such as an employer, a landlord, or a credit reference. This document serves as a legal notification to the consumer, ensuring transparency and compliance with Oklahoma laws. The notice will outline the specific reasons and details of the increase in charges, providing consumers with an opportunity to review and assess the changes. It is crucial for consumers to carefully read and understand the content of this notice to remain informed about their credit obligations. It's also important to note that there can be different types of Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency, depending on the nature of the credit account and the credit issuer involved. Some specific types of notices could include: 1. Credit Card Notice: This type of notice is specifically related to credit card accounts, where the credit issuer informs the consumer about an increase in charges based on information received from a non-consumer reporting agency. The notice will detail the new charges applicable to the credit card account and any other relevant information that consumers need to be aware of. 2. Personal Loan Notice: This type of notice is relevant to personal loans or installment loans. It is issued when the credit issuer decides to increase the charges associated with the loan based on information obtained from a source other than a consumer reporting agency. Consumers will receive a detailed explanation of the increased charges and any other relevant terms of the loan. 3. Mortgage Notice: For consumers with a mortgage, this type of notice will be sent if the credit issuer decides to raise charges based on information received from a non-consumer reporting agency. The notice will inform the consumer about the new terms, including changes in interest rates, payment amounts, or any other pertinent information. 4. Auto Loan Notice: If a consumer has an auto loan and the credit issuer determines an increase in charges based on information obtained from a non-consumer reporting agency, this notice will be issued. It will provide detailed information about the revised terms, such as a higher interest rate or increased monthly payments. In conclusion, the Oklahoma Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a crucial document that credit issuers use to inform consumers about changes in their credit terms. By receiving this notice, consumers can stay informed about the adjustments in charges and evaluate the impact on their credit obligations.