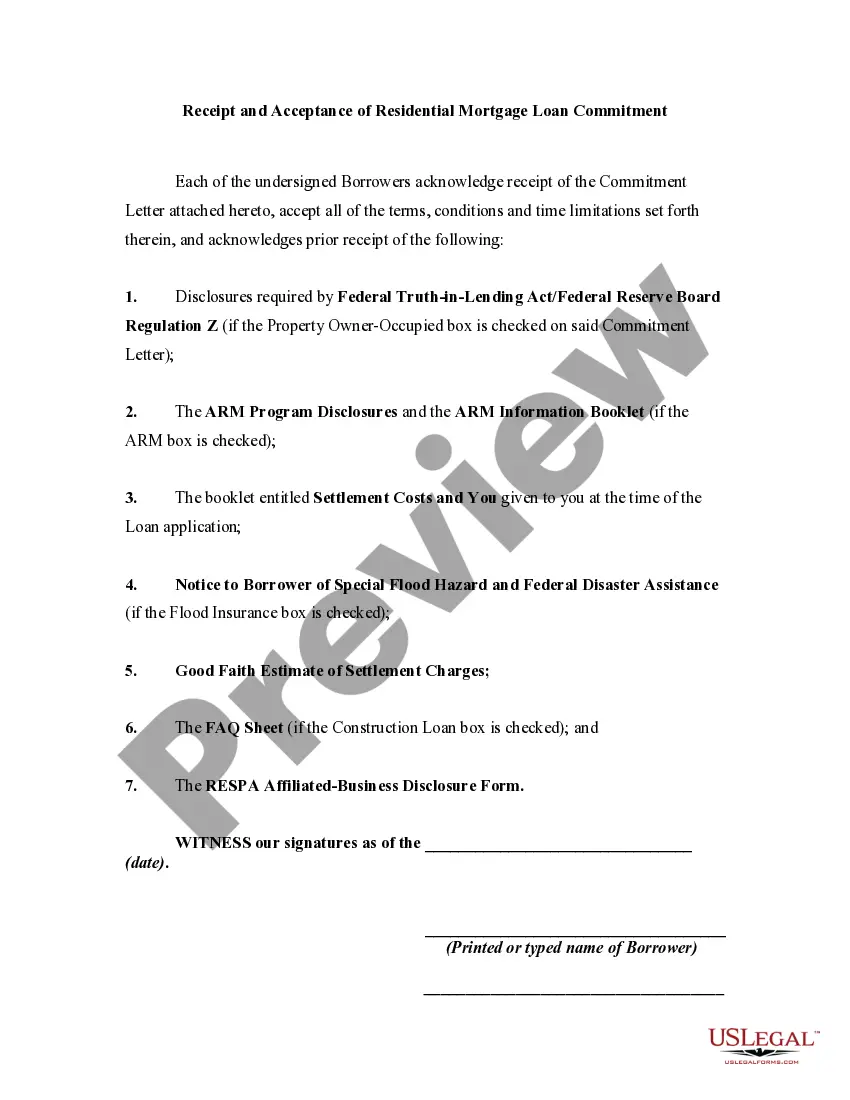

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Oklahoma Receipt and Acceptance of Residential Mortgage Loan Commitment is a crucial document associated with the home buying process in the state of Oklahoma. It serves as evidence of the borrower's acceptance of the terms and conditions outlined in the mortgage loan commitment agreement. This legally binding document signifies both the receipt of the commitment from the lending institution and the borrower's acknowledgment of its terms. A Residential Mortgage Loan Commitment is an agreement between a borrower and a lender outlining the specifics of a mortgage loan. It includes important details such as the loan amount, interest rate, repayment terms, and any specific conditions or contingencies that must be met. The commitment provides certainty for the borrower, ensuring that the lender is committed to providing the loan under the agreed-upon terms. Different types of Oklahoma Receipt and Acceptance of Residential Mortgage Loan Commitment may vary based on the specific lending institution, loan program, and individual circumstances. Some common variations include: 1. Conventional Mortgage Loan Commitments: These commitments are issued by traditional lending institutions such as banks or credit unions. They typically adhere to the guidelines set by Fannie Mae or Freddie Mac, the government-sponsored enterprises that provide liquidity to the mortgage market. 2. FHA (Federal Housing Administration) Mortgage Loan Commitments: These commitments are offered by lenders that participate in the FHA program. FHA loans are insured by the federal government and often provide more lenient qualifying criteria, making them popular for first-time homebuyers or individuals with lower credit scores. 3. VA (Department of Veterans Affairs) Mortgage Loan Commitments: These commitments are specifically for eligible veterans, active-duty service members, and surviving spouses. VA loans are guaranteed by the VA, providing favorable terms and low or no down payment options. 4. USDA (United States Department of Agriculture) Mortgage Loan Commitments: These commitments are available for borrowers in designated rural areas and are backed by the USDA. The USDA loan program supports rural homeownership by providing affordable financing options with low interest rates. 5. Jumbo Mortgage Loan Commitments: Jumbo commitments are for loan amounts exceeding the conforming loan limits set by Fannie Mae and Freddie Mac. Borrowers seeking high-value properties often turn to jumbo loans, which typically carry higher interest rates and stricter qualifying requirements. Obtaining an Oklahoma Receipt and Acceptance of Residential Mortgage Loan Commitment is a significant milestone in the home buying process. It provides confidence to both the borrower and the lending institution that the loan terms have been accepted, leading to the next stages of the transaction, such as the closing and disbursement of funds.