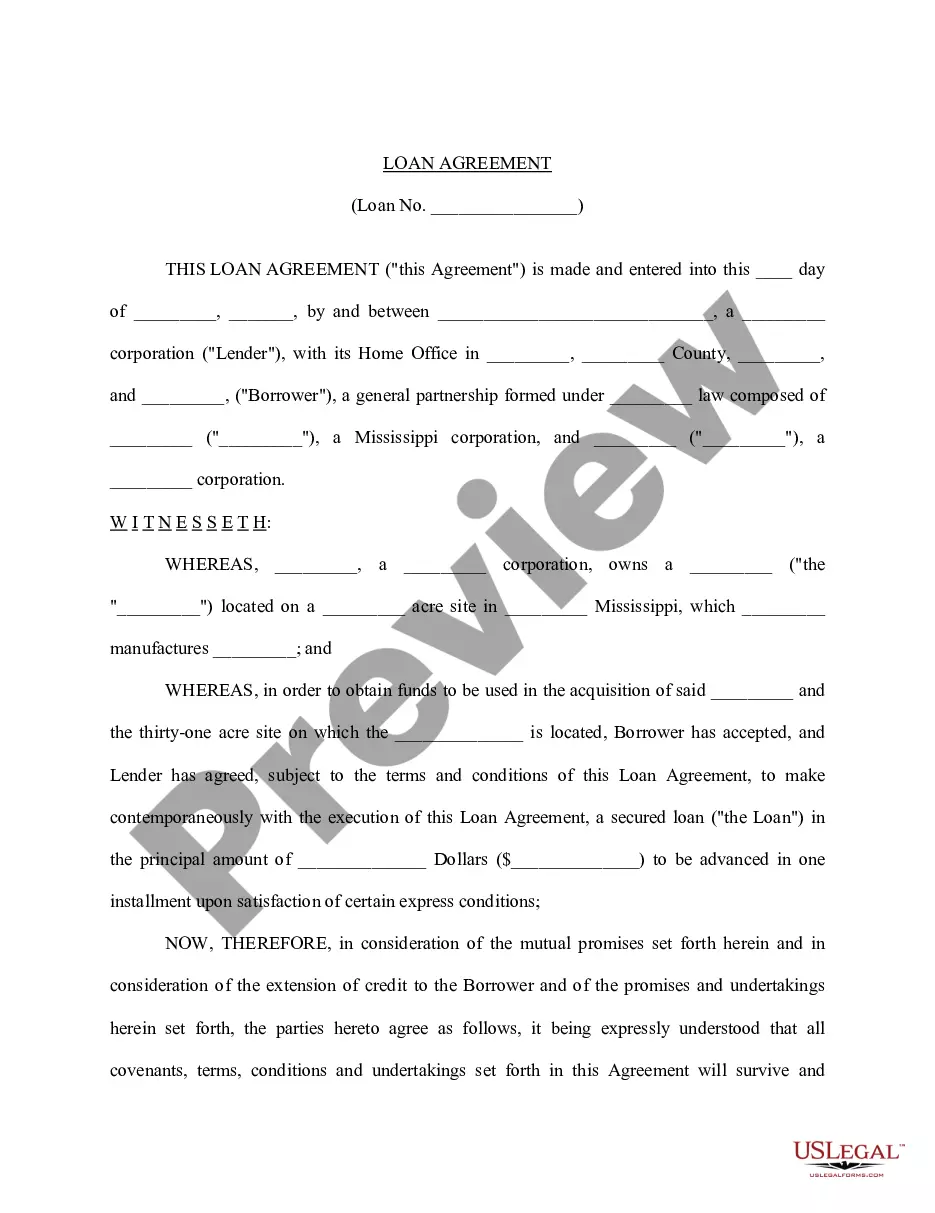

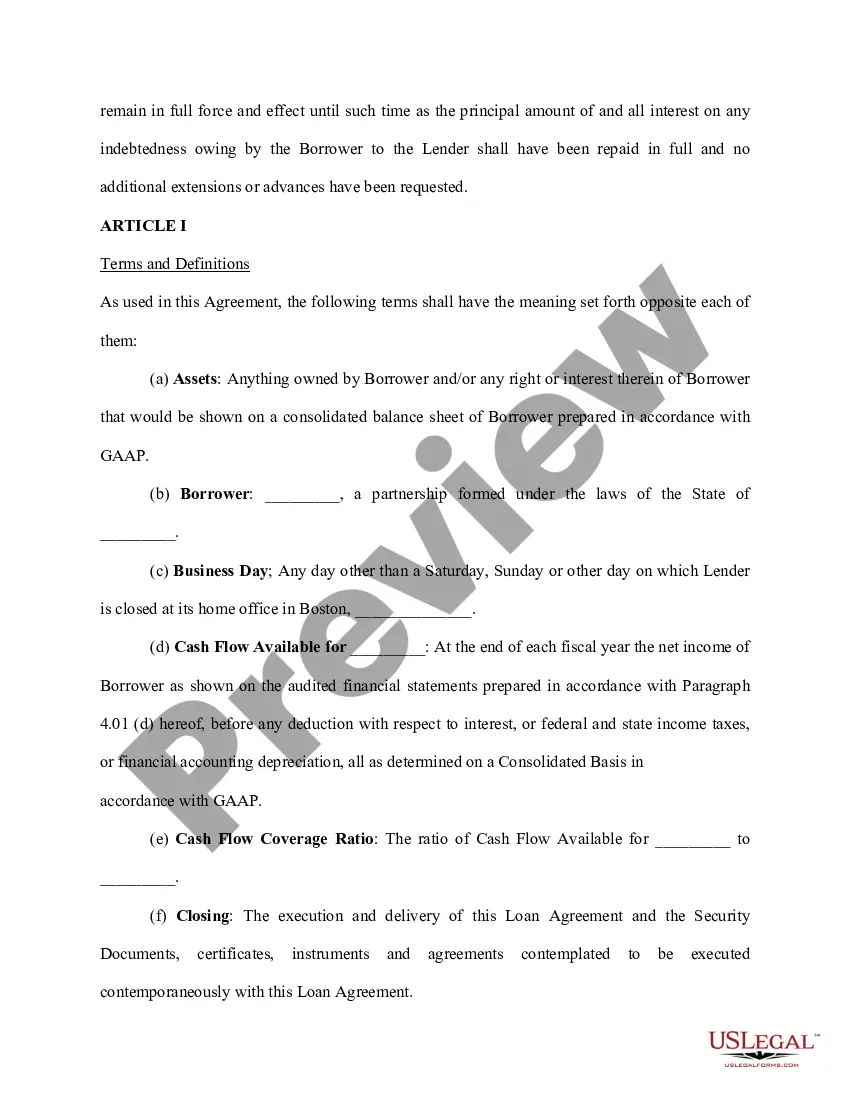

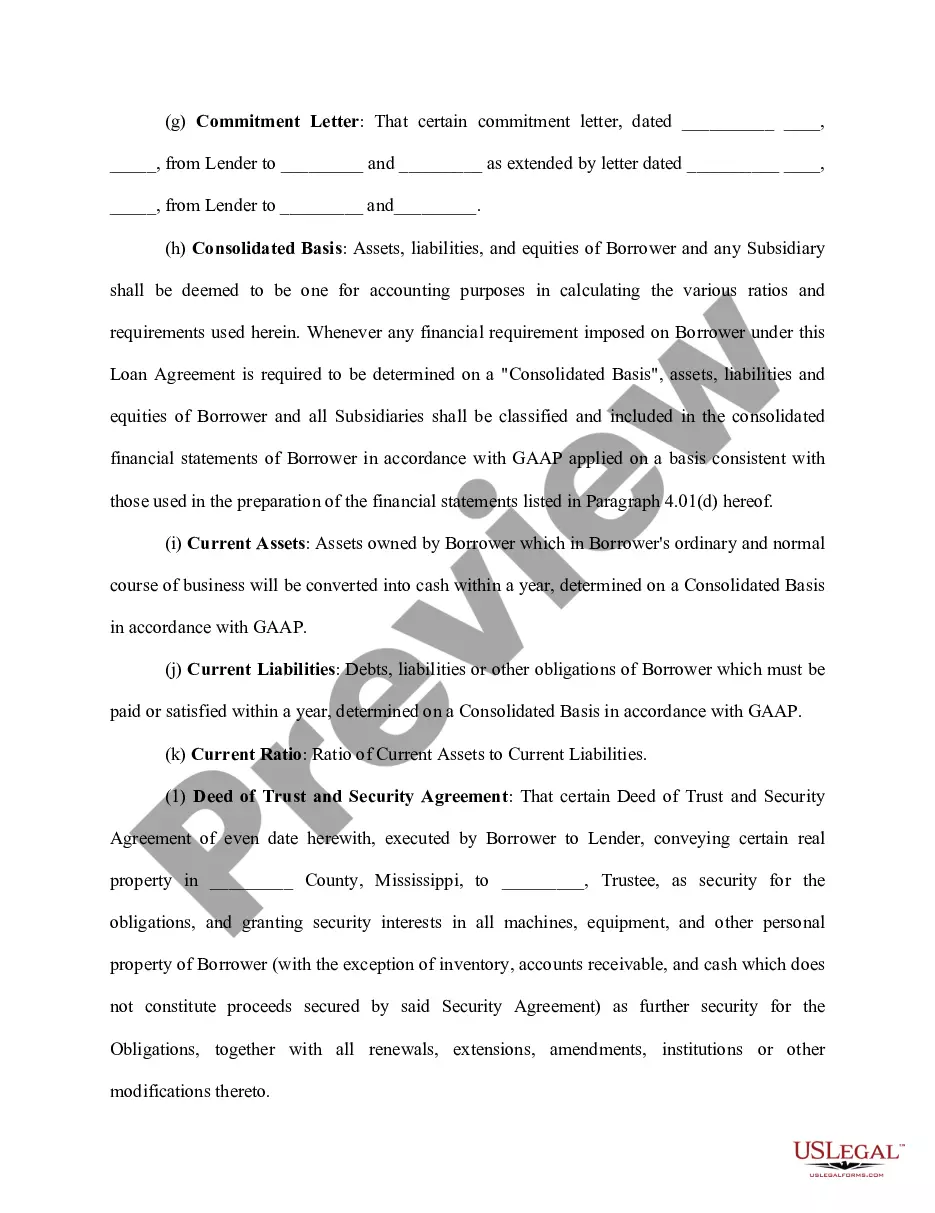

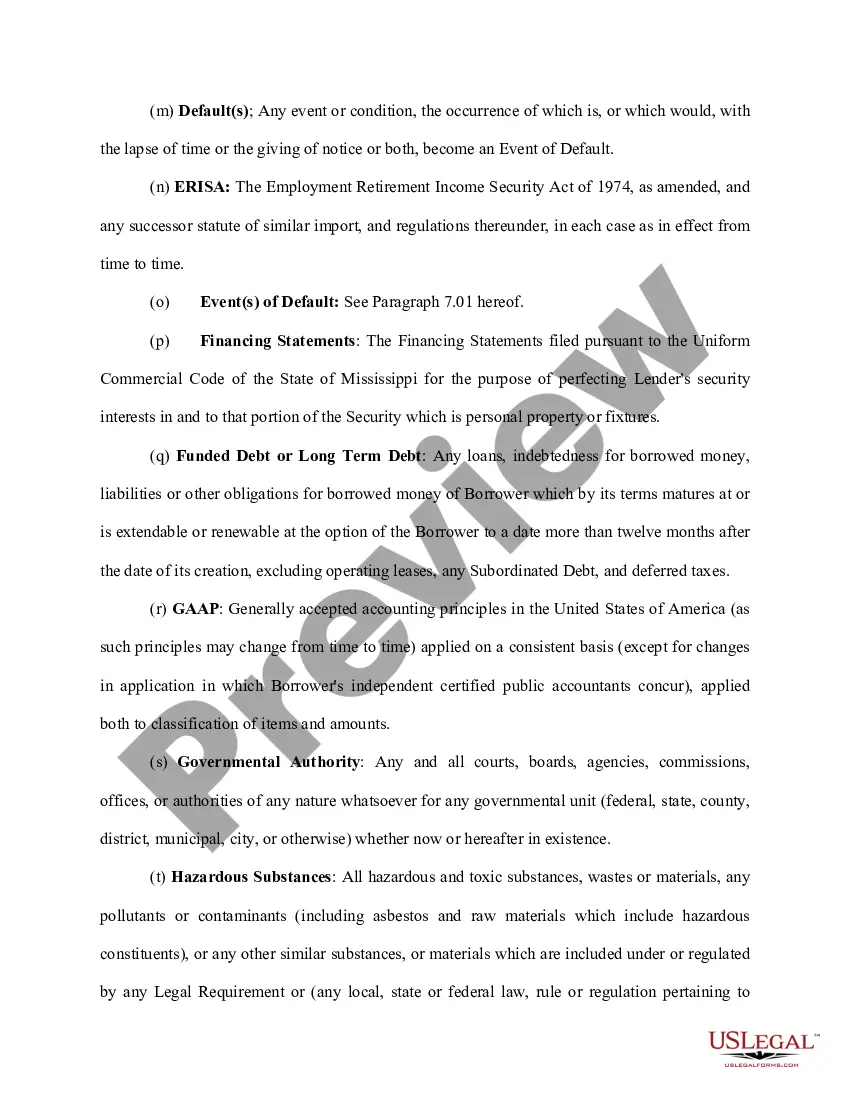

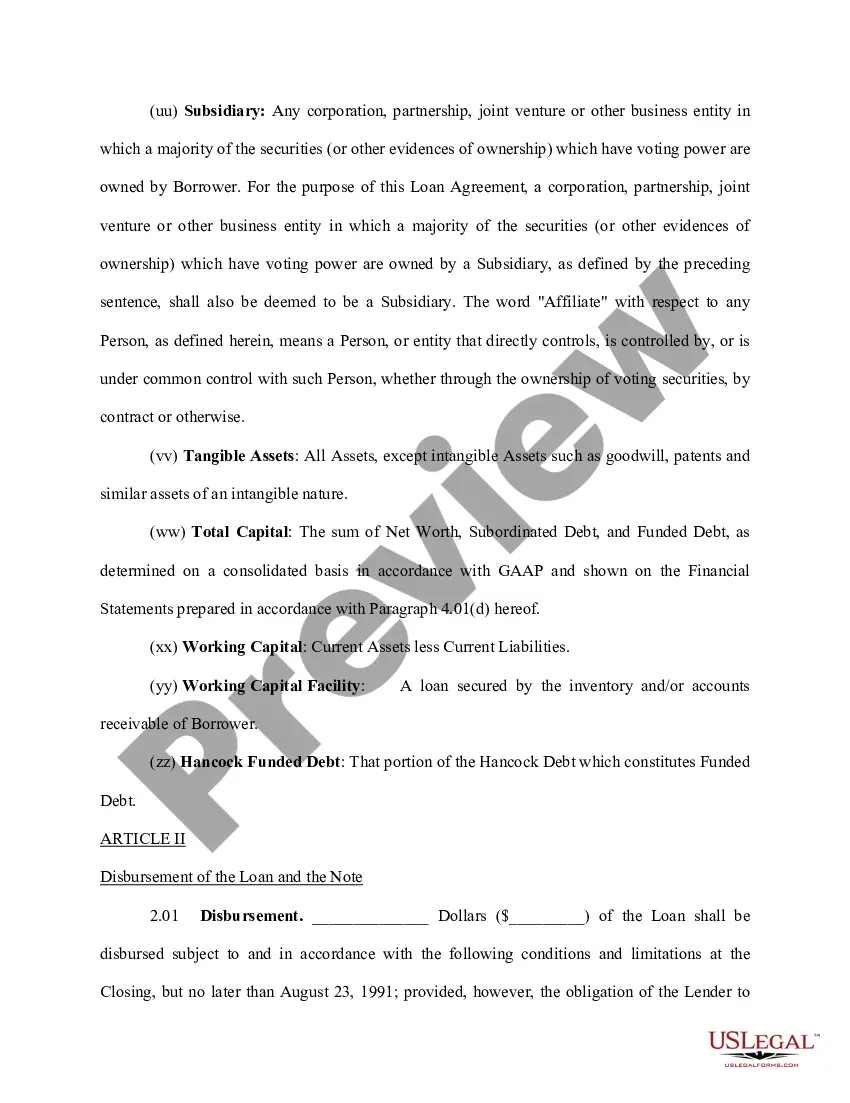

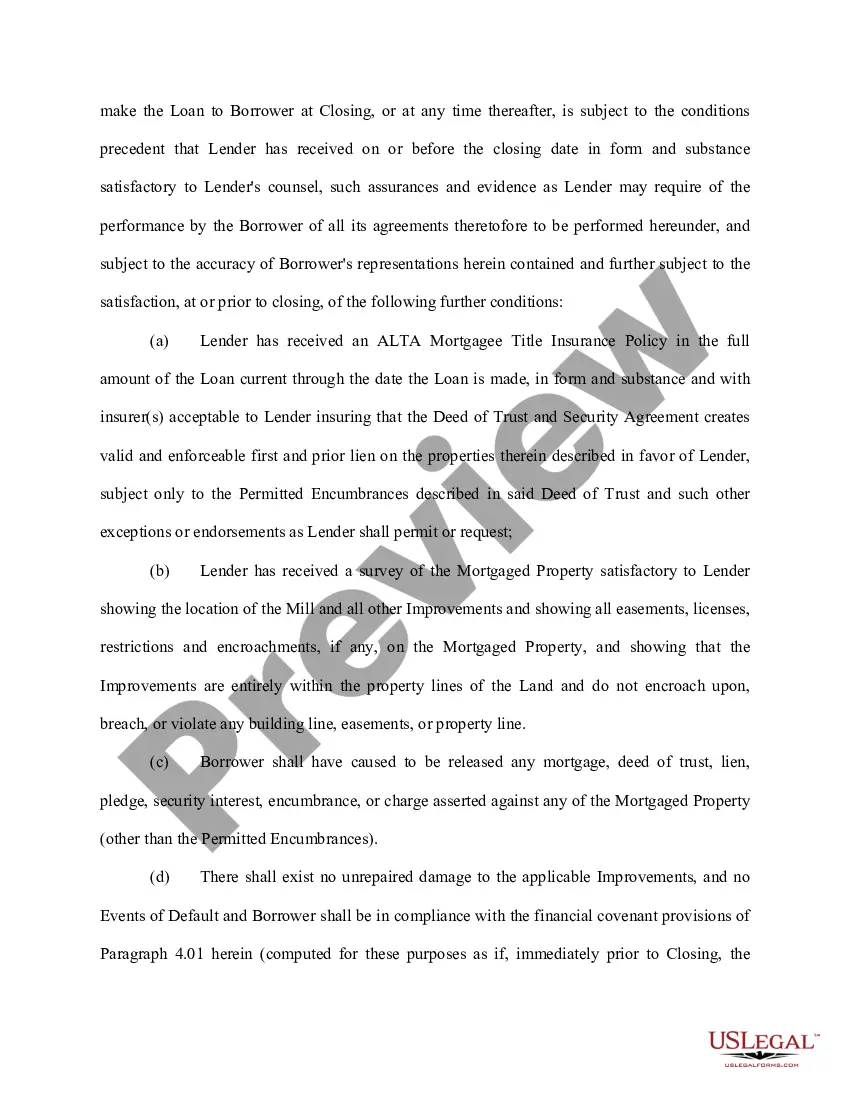

The Oklahoma Loan Agreement for Employees is a legal contract that outlines the terms and conditions under which an employer provides a loan or advances funds to an employee. This agreement serves as a formal document that establishes the borrower's obligation to repay the loan amount within a specified time frame, along with any applicable interest rates, late payment penalties, and other terms agreed upon by both parties. Key Features: — Loan Amount: The agreement specifies the principal amount that is being loaned to the employee. It takes into account the purpose of the loan, whether it's for personal emergency expenses, educational purposes, medical bills, or other permissible reasons. — Interest Rates: If applicable, the agreement will detail the interest rate at which the loan is being extended. It can be fixed or variable, and is typically based on the prevailing market rates or the employer's internal policies. — Repayment Terms: This section explains the repayment schedule for the employee to follow. It specifies the duration of the loan, the installment amounts, and the frequency of repayment (e.g., monthly, bi-weekly). — Late Payment Penalties: The agreement may address the consequences of late or missed payments by outlining the penalties or additional fees that the employee will incur. These penalties are designed to ensure timely repayment of the loan. — Security or Collateral: In some cases, loans may require collateral as security, which provides the lender with a form of assurance in case the borrower defaults on the loan. The agreement will mention any assets or property that the employee must provide as collateral. — Loan Termination: This section clarifies the circumstances under which the lender may terminate the loan agreement. It may include events such as the borrower's termination or resignation from employment or a breach of the terms agreed upon in the agreement. Types of Oklahoma Loan Agreement for Employees: 1. Short-Term Loan Agreement: Typically covers smaller loan amounts that are expected to be repaid within a shorter duration, often ranging from a few months to a year. These loans are commonly used for immediate financial needs or unexpected expenses. 2. Long-Term Loan Agreement: Involves larger loan amounts that are repaid over an extended period, often several years. These loans are commonly utilized for significant expenses like home renovations, buying a vehicle, or funding higher education. 3. Employee Advance Agreement: This type of agreement is used when an employer provides an employee with an advance payment on their salary. The agreement outlines the terms of repayment, including installment amounts and any deductions from future paychecks. In conclusion, the Oklahoma Loan Agreement for Employees is a crucial legal document that protects the interests of both the employer and employee when providing financial assistance. By clearly outlining the terms and conditions, this agreement ensures transparency, compliance with state laws, and timely repayment of the loan.

Oklahoma Loan Agreement for Employees

Description

How to fill out Oklahoma Loan Agreement For Employees?

You are able to commit hrs on the Internet looking for the legitimate document template that fits the state and federal demands you need. US Legal Forms provides 1000s of legitimate forms that happen to be evaluated by specialists. You can easily acquire or print out the Oklahoma Loan Agreement for Employees from your assistance.

If you already possess a US Legal Forms bank account, you may log in and then click the Down load option. Next, you may comprehensive, modify, print out, or indicator the Oklahoma Loan Agreement for Employees. Each legitimate document template you acquire is the one you have for a long time. To get yet another duplicate of the purchased type, visit the My Forms tab and then click the related option.

If you are using the US Legal Forms internet site the very first time, stick to the easy instructions under:

- Initial, make sure that you have chosen the proper document template to the region/metropolis of your liking. See the type information to make sure you have picked the appropriate type. If available, take advantage of the Preview option to search with the document template as well.

- If you want to get yet another edition of your type, take advantage of the Search area to get the template that meets your requirements and demands.

- Once you have found the template you would like, just click Buy now to proceed.

- Pick the rates strategy you would like, type in your accreditations, and sign up for an account on US Legal Forms.

- Total the transaction. You can use your Visa or Mastercard or PayPal bank account to pay for the legitimate type.

- Pick the structure of your document and acquire it to the gadget.

- Make modifications to the document if possible. You are able to comprehensive, modify and indicator and print out Oklahoma Loan Agreement for Employees.

Down load and print out 1000s of document layouts utilizing the US Legal Forms website, which offers the largest collection of legitimate forms. Use skilled and condition-particular layouts to tackle your small business or individual requires.