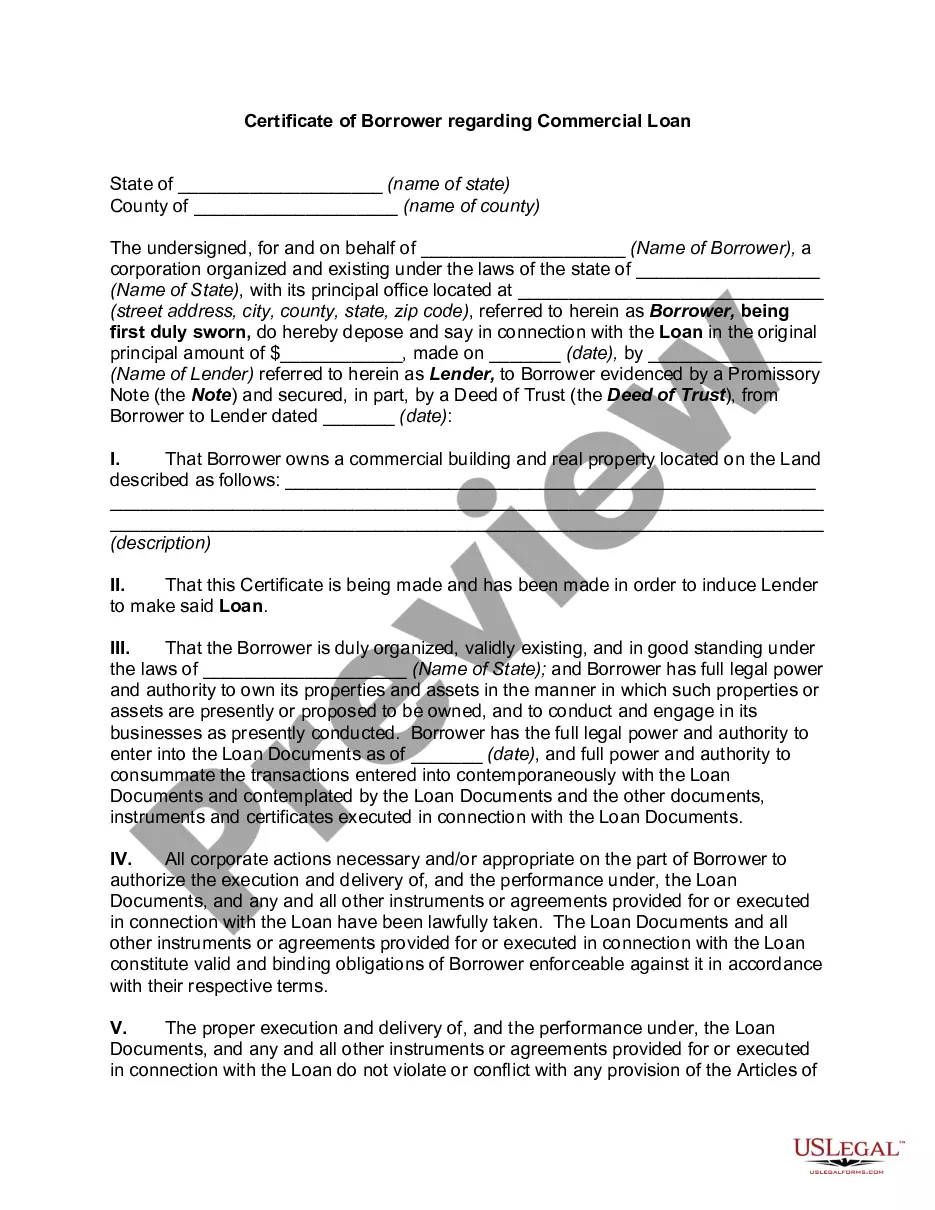

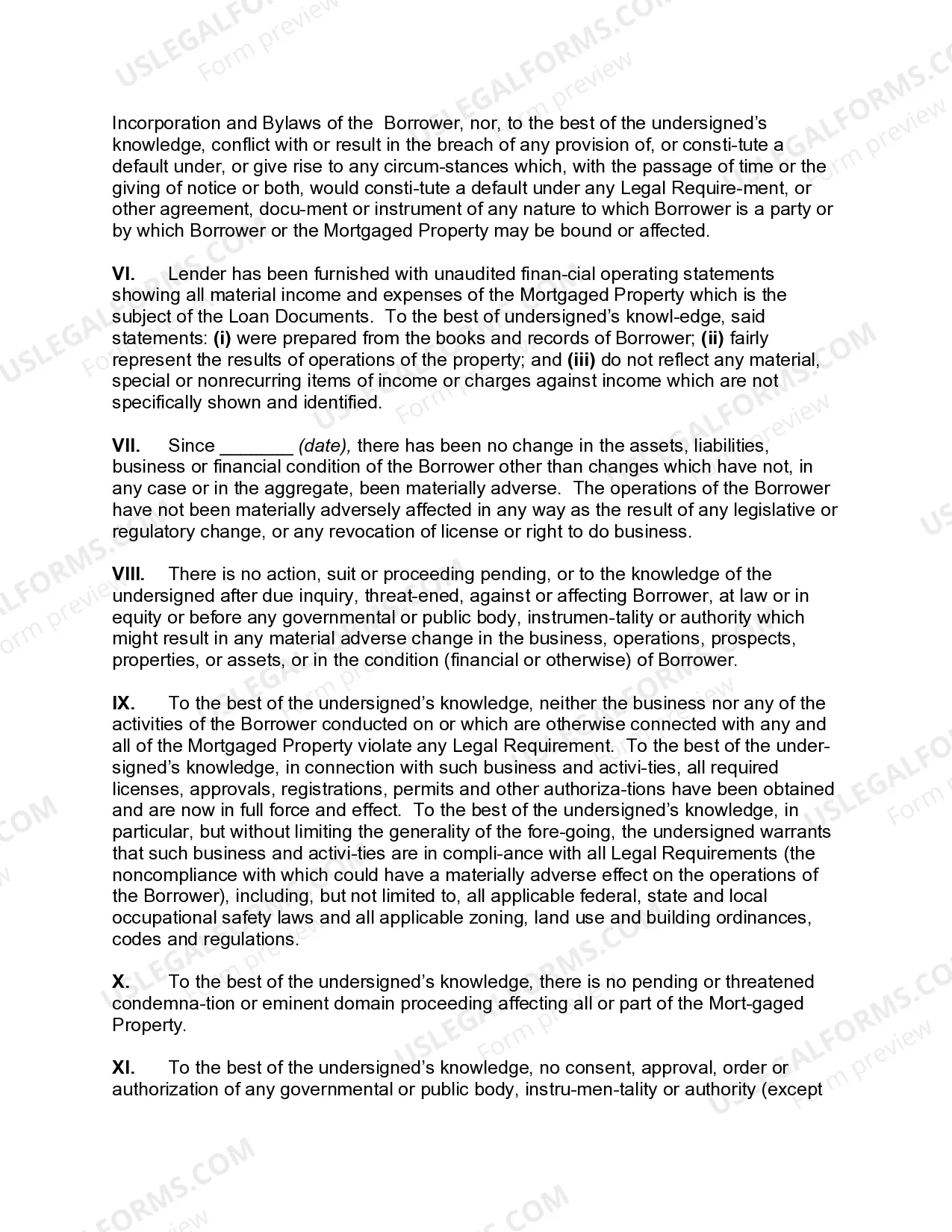

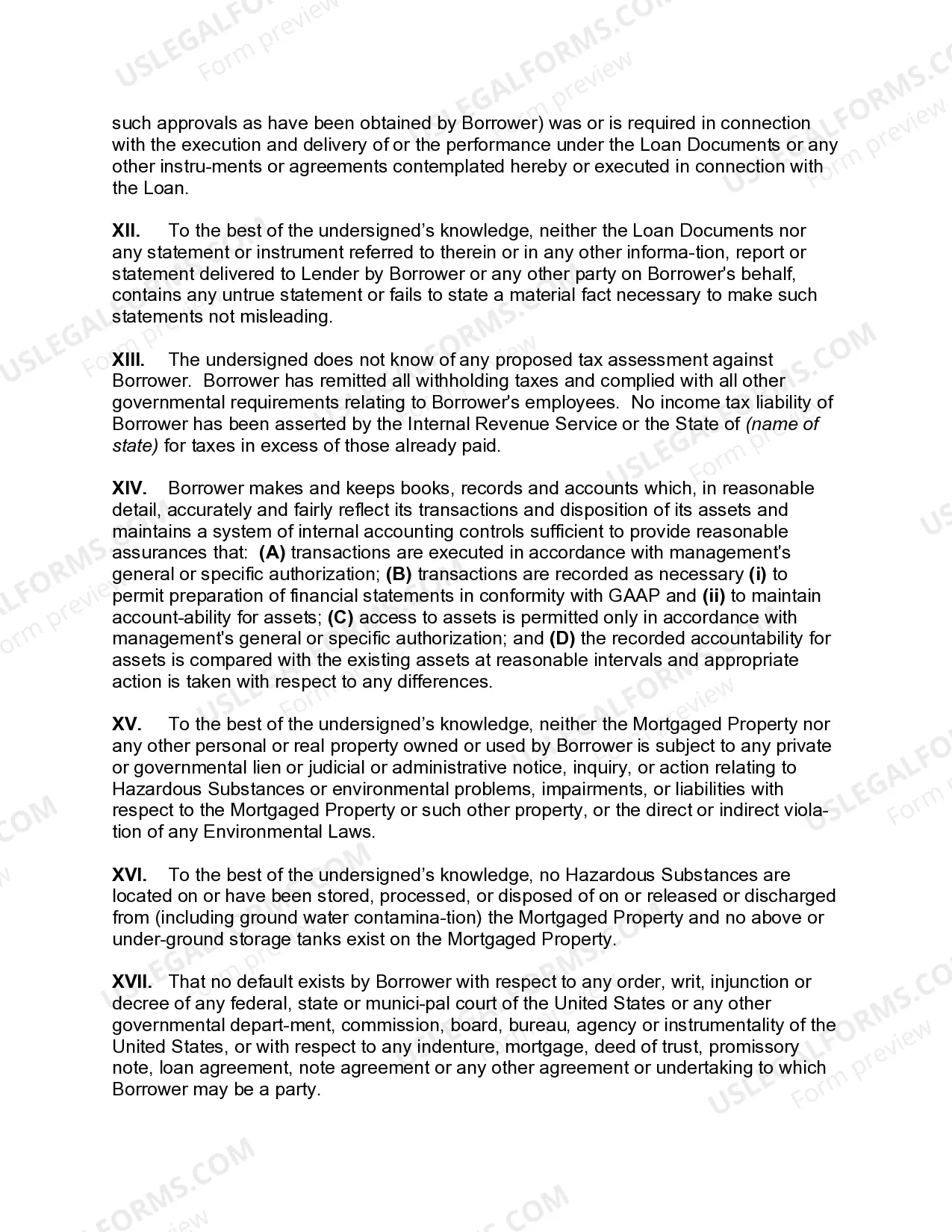

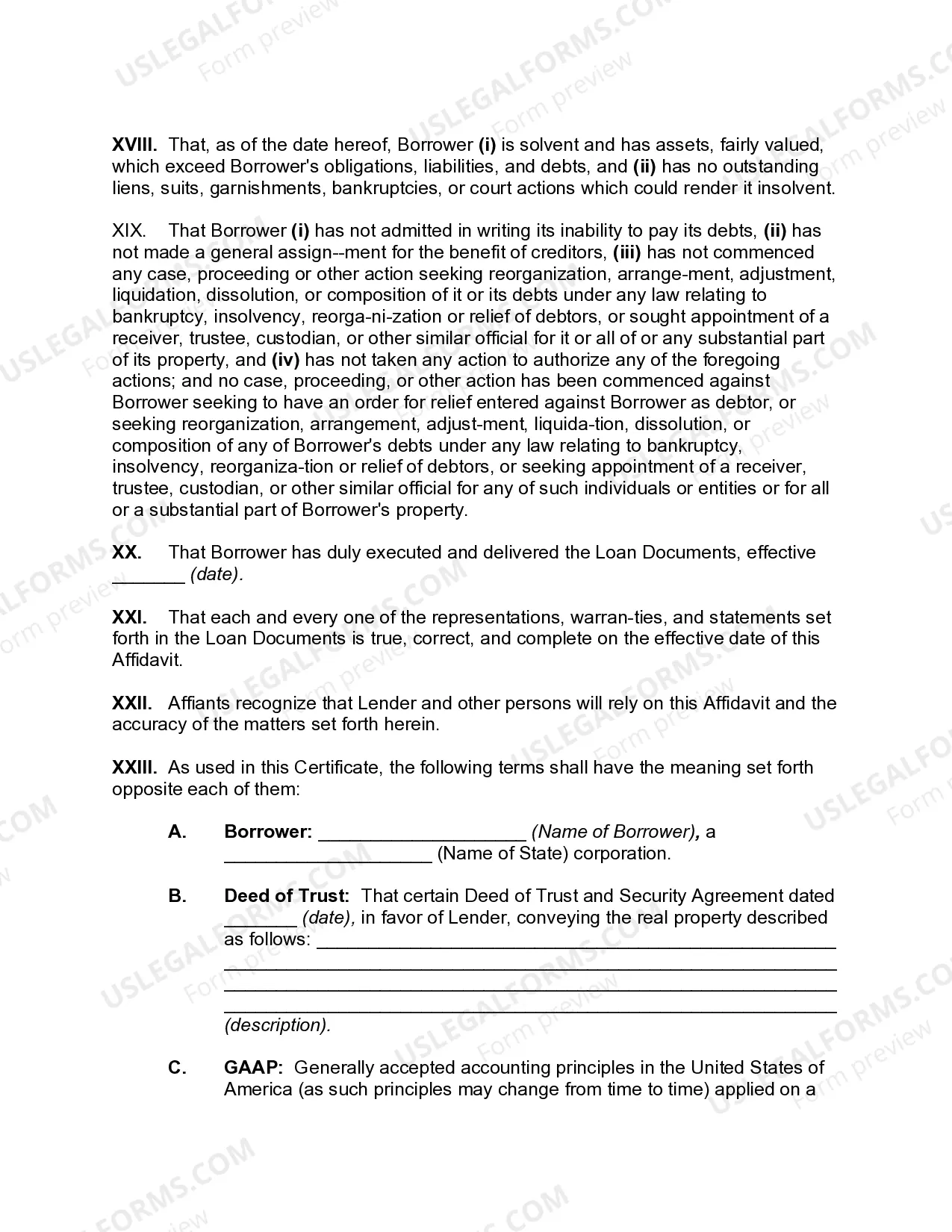

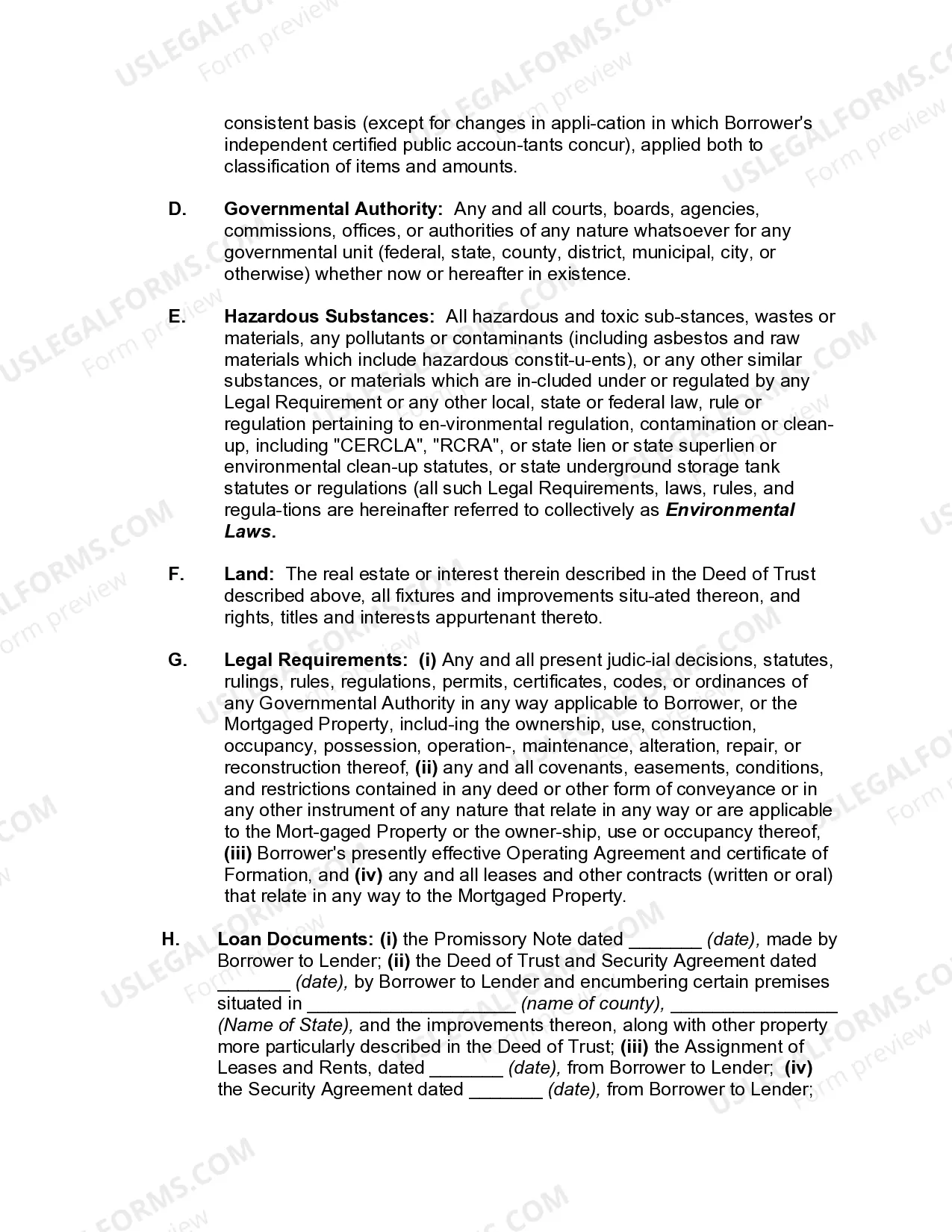

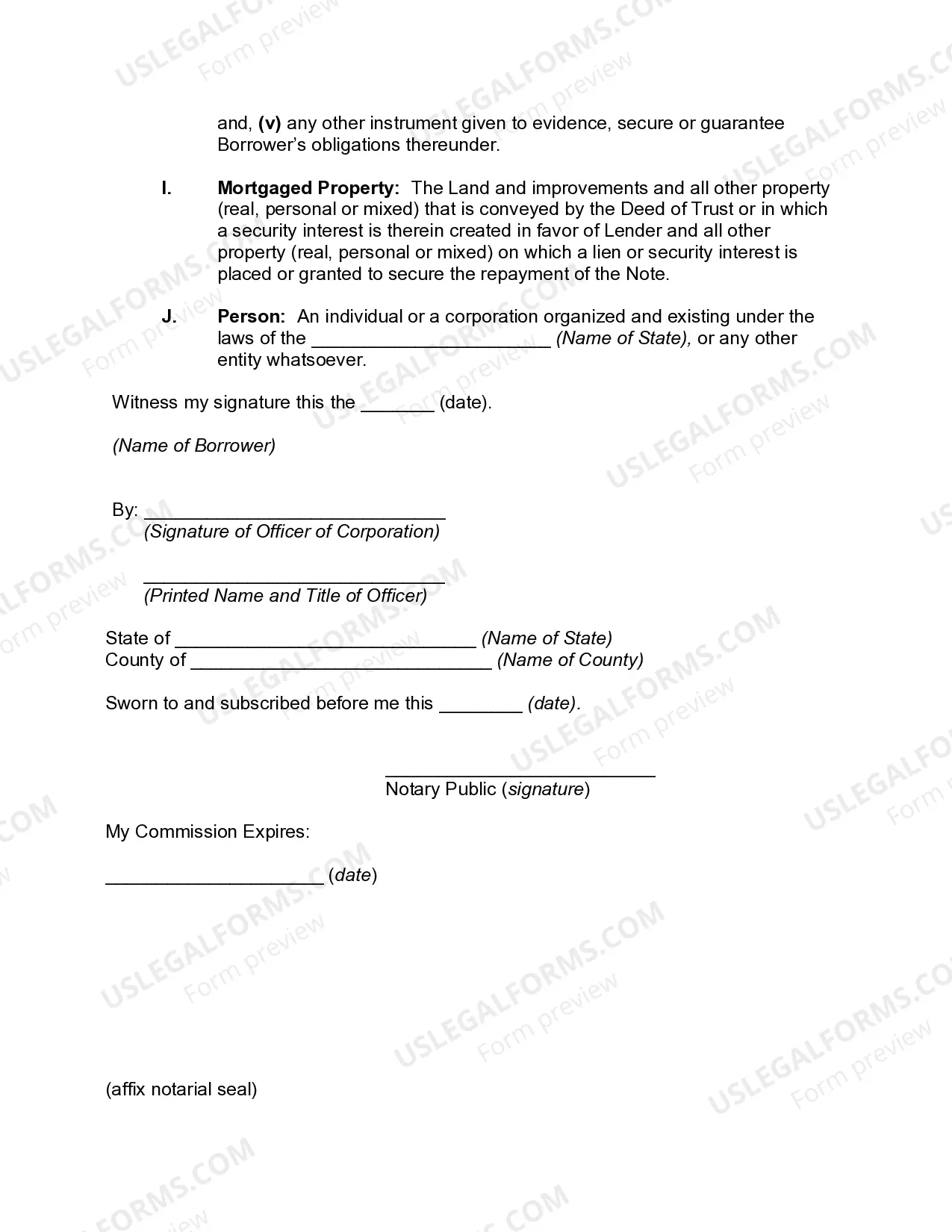

The Oklahoma Certificate of Borrower regarding Commercial Loan is a legal document that pertains to commercial loan transactions in the state of Oklahoma. It serves as a declaration by the borrower, providing important information about the borrower's business, financial standing, and ability to repay the loan. This document is typically required by lenders as part of their due diligence process before approving a commercial loan. The Oklahoma Certificate of Borrower contains various sections, each addressing specific aspects related to the borrower's profile and loan application. The information provided in this document helps lenders assess the creditworthiness of the borrower and evaluate the risks associated with extending a commercial loan. Key sections of the Oklahoma Certificate of Borrower may include: 1. Business Information: This section requires the borrower to provide comprehensive details about their business, including its legal name, address, organizational structure, industry sector, and the nature of its operations. 2. Financial Statements: Borrowers are typically required to include their financial statements such as income statements, balance sheets, and cash flow statements for a specific period. These statements give lenders insights into the borrower's financial health and their ability to generate sufficient revenues to meet loan repayments. 3. Existing Liabilities: Borrowers must disclose any existing debts or liabilities they have incurred, including outstanding loans, lines of credit, or other financial obligations. This information helps lenders evaluate the borrower's overall debt burden and assess their capacity to manage additional loan obligations. 4. Collateral: If the commercial loan is secured by collateral (such as property, inventory, or equipment), this section outlines the details of the collateral being offered as security. Lenders use this information to assess the value and quality of the collateral and determine its suitability as a form of security. 5. Guarantors: In some cases, the borrower may have guarantors or co-signers for the loan. This section collects information about the identity, financial standing, and relationship of any individuals or entities providing guarantees for the loan. Different types of Oklahoma Certificate of Borrower regarding Commercial Loan may exist based on the specific requirements of different lenders or loan programs. Some common variations may include: 1. Oklahoma Small Business Certificate of Borrower: Designed specifically for small businesses seeking commercial loans, this version may have additional sections related to the borrower's business plan, industry analysis, or marketing strategy. 2. Oklahoma Real Estate Loan Certificate of Borrower: If the commercial loan is intended for real estate projects, this version may place more emphasis on property-related details such as property appraisals, proposed developments, leasing agreements, or land use permits. 3. Oklahoma Agricultural Loan Certificate of Borrower: In cases where the commercial loan is intended for agricultural purposes, this version may include specialized sections related to crop yields, livestock inventory, farm management practices, or government subsidies. 4. Oklahoma Construction Loan Certificate of Borrower: This version may focus on construction projects, including details about contractors, building permits, architectural plans, construction timelines, and disbursement schedules. It is important to note that the specific contents and requirements of the Oklahoma Certificate of Borrower may vary among lenders, loan programs, and the nature of the commercial loan being sought. Borrowers should consult with their lenders or legal advisors to ensure they provide accurate and relevant information in accordance with the lender's specific requirements.

Oklahoma Certificate of Borrower regarding Commercial Loan

Description

How to fill out Oklahoma Certificate Of Borrower Regarding Commercial Loan?

Choosing the right authorized file template can be a struggle. Needless to say, there are a lot of web templates available on the Internet, but how will you find the authorized form you want? Utilize the US Legal Forms website. The assistance provides 1000s of web templates, including the Oklahoma Certificate of Borrower regarding Commercial Loan, that can be used for business and personal demands. All of the kinds are checked by professionals and satisfy federal and state needs.

When you are currently authorized, log in for your account and then click the Down load option to have the Oklahoma Certificate of Borrower regarding Commercial Loan. Make use of your account to search throughout the authorized kinds you may have bought in the past. Go to the My Forms tab of your account and get an additional duplicate from the file you want.

When you are a brand new customer of US Legal Forms, listed here are simple guidelines for you to adhere to:

- Very first, make certain you have selected the appropriate form for your city/state. You are able to look through the form utilizing the Preview option and look at the form explanation to ensure it will be the right one for you.

- When the form fails to satisfy your requirements, take advantage of the Seach area to obtain the proper form.

- Once you are certain that the form is acceptable, go through the Acquire now option to have the form.

- Select the costs program you need and enter in the necessary info. Build your account and buy your order using your PayPal account or credit card.

- Pick the submit file format and download the authorized file template for your device.

- Total, revise and print out and signal the acquired Oklahoma Certificate of Borrower regarding Commercial Loan.

US Legal Forms is the biggest collection of authorized kinds for which you will find different file web templates. Utilize the company to download expertly-created paperwork that adhere to status needs.

Form popularity

FAQ

Mortgage Loan Officer Salary in Oklahoma Annual SalaryHourly WageTop Earners$110,966$5375th Percentile$92,500$44Average$63,802$3125th Percentile$33,300$16

Oklahoma statute 14A-3-501 describes a supervised lender as any business entity who issues loans in which the rate of the loan finance charge exceeds 10% per year. BondExchange now offers monthly pay-as-you-go subscriptions for surety bonds.

In the state of Oklahoma, mortgage loan originators are required to: Complete a Criminal Background Check (CBC). Authorize a credit report through the NMLS. Fulfill all state and federal education requirements as designated by your state agency. Take and pass a National Test.

MLOs work closely with real estate agents, helping borrowers field the financial side of a home purchase. While Mortgage Brokers work for a brokerage, Mortgage Loan Originators are often employed by a bank or mortgage company.

ZipRecruiter pins your MLO median annual salary at $70,115 or roughly $35 per hour. California performs pretty competently against the national annual average of $74,838.

Oklahoma's statutory interest rate limit is 6 percent unless stated otherwise through a valid contract (which may be as simple as agreeing to the "fine print"). Exceptions to this limit include pawnshops, small loans, and retail installment plans.

Any employer who willfully or repeatedly violates the requirements of section 5 of this Act, any standard, rule, or order promulgated pursuant to section 6 of this Act, or regulations prescribed pursuant to this Act, may be assessed a civil penalty of not more than $70,000 for each violation, but not less than $5,000 ...

In the state of Oklahoma, mortgage loan originators are required to: Complete a Criminal Background Check (CBC). Authorize a credit report through the NMLS. Fulfill all state and federal education requirements as designated by your state agency. Take and pass a National Test.