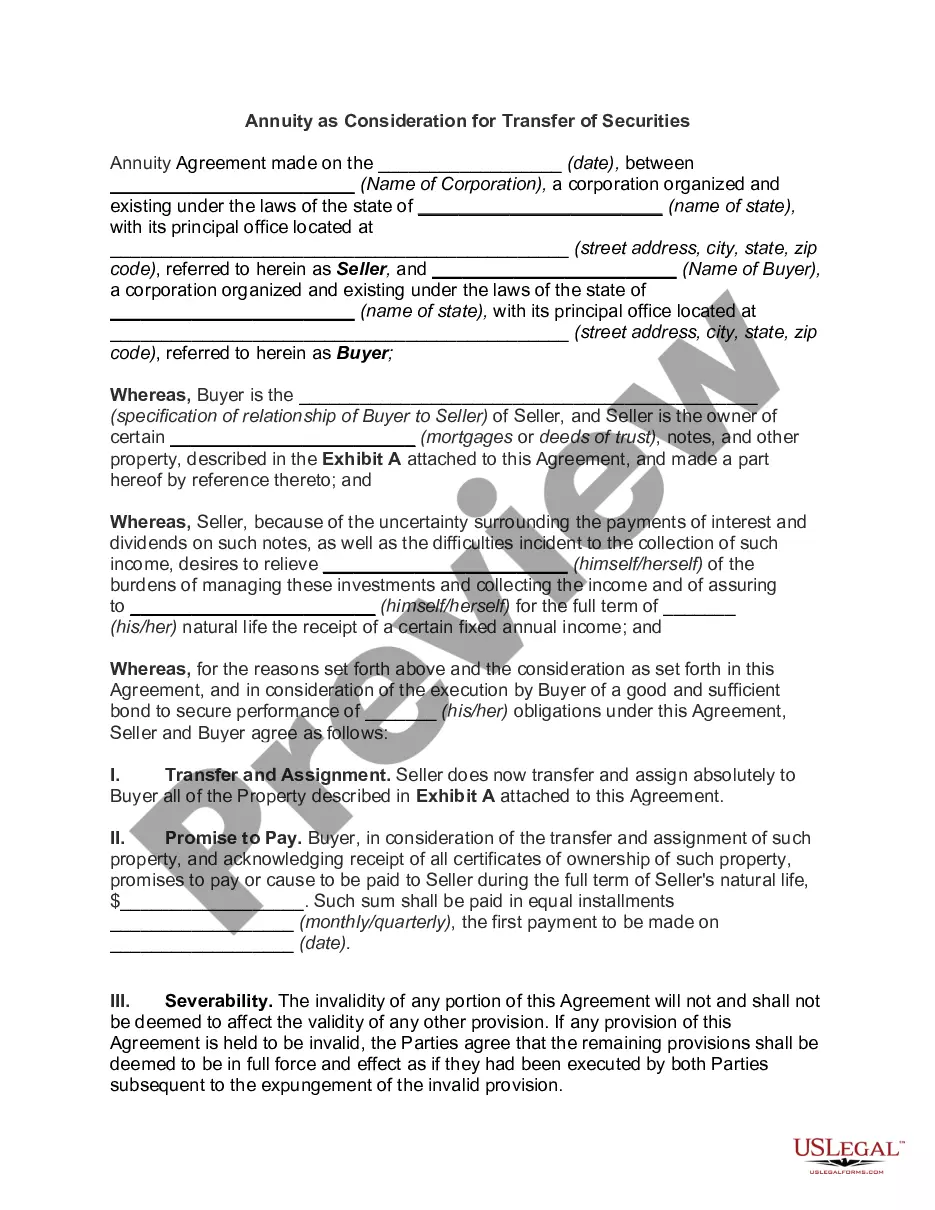

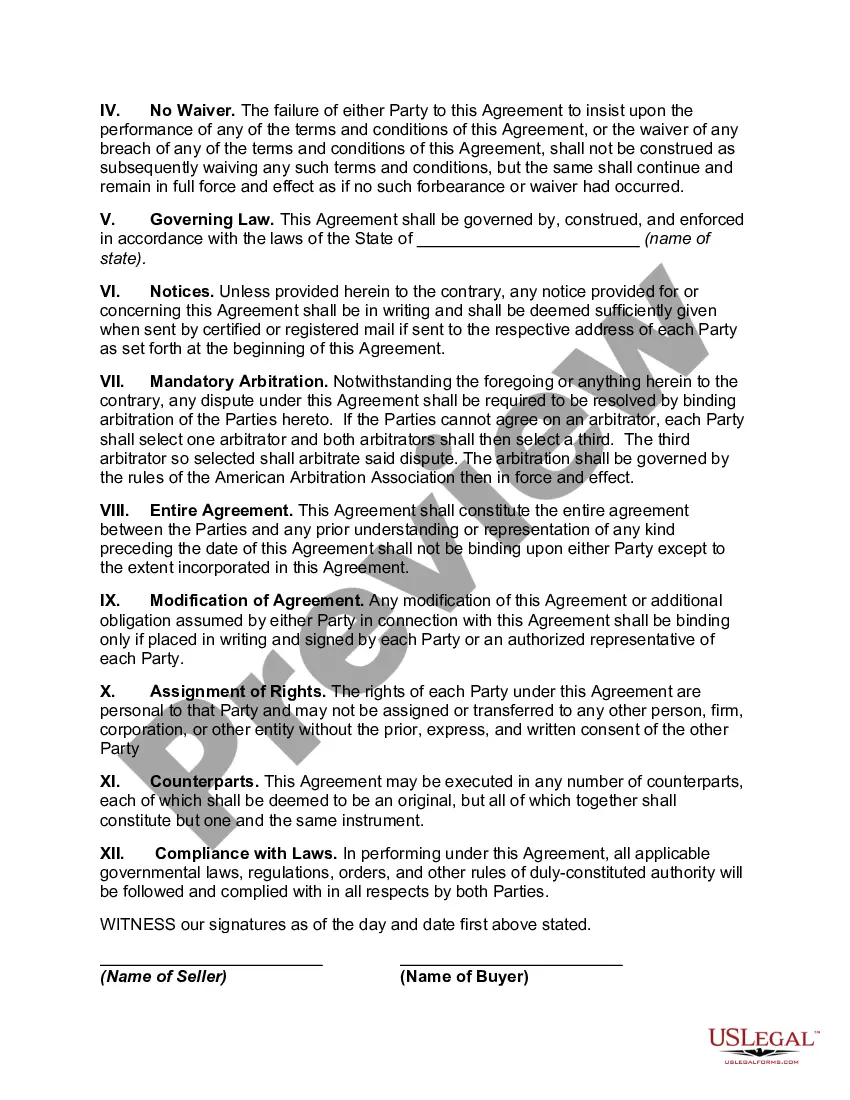

Oklahoma Annuity as Consideration for Transfer of Securities: A Comprehensive Overview Introduction: Oklahoma Annuity as consideration for the transfer of securities refers to a financial arrangement where an annuity is used as a means of payment in exchange for the transfer of securities. This arrangement allows individuals or organizations to exchange their securities for a fixed stream of income, providing them with a reliable income source over time. In this detailed description, we will explore the concept of Oklahoma Annuity as Consideration for Transfer of Securities, its benefits, and the various types of annuities commonly used in such transactions. Key Concepts: 1. Annuity: An annuity is a financial contract between an individual (annuitant) and an insurance company, where the annuitant invests a lump sum or periodic payments in exchange for regular income payments after a certain period. The income stream may be fixed or variable, depending on the type of annuity chosen. 2. Securities: Securities refer to tradable financial assets such as stocks, bonds, or mutual funds that represent ownership or debt in a company or government entity. These instruments are often bought and sold in financial markets, and their value can fluctuate based on market conditions and other factors. Oklahoma Annuity as Consideration for Transfer of Securities Explained: Oklahoma Annuity as consideration for the transfer of securities offers an alternative method for individuals or organizations to diversify their investment portfolios or monetize their securities holdings. Instead of selling securities immediately for a lump sum, this arrangement allows them to transfer the securities to an insurance company in exchange for an annuity. Benefits of Oklahoma Annuity as Consideration for Transfer of Securities: 1. Tax Efficiency: By choosing an annuity as consideration, individuals may benefit from tax deferral on their securities' capital gains. Rather than incurring immediate capital gains taxes on the sales, the gains are only taxed when received as income during the annuity payout phase. 2. Steady Income Stream: Opting for an annuity ensures a predictable and regular income stream. This can be advantageous for individuals seeking a stable source of funds to cover living expenses during retirement or other financial goals. 3. Long-Term Planning: Annuities allow individuals to plan for their financial future with a long-term perspective. By receiving regular payments over a specified period or for life, individuals can better estimate their income stream and make informed decisions regarding other financial aspects. Types of Oklahoma Annuity as Consideration for Transfer of Securities: 1. Fixed Annuity: In a fixed annuity, the insurance company guarantees a fixed rate of return on the annuitant's investment. This offers a stable income stream, making it a popular choice for risk-averse individuals or those with conservative investment preferences. 2. Variable Annuity: Unlike fixed annuities, variable annuities' returns are tied to underlying investment options, often mutual funds. The annuitant bears the investment risk and has the potential for higher returns but also faces market fluctuations. 3. Hybrid Annuity: Hybrid annuities combine features of both fixed and variable annuities. They offer a guaranteed minimum return while allowing some investment flexibility. These annuities often appeal to individuals seeking a balance between guaranteed income and potential growth. Conclusion: Oklahoma Annuity as Consideration for Transfer of Securities provides a convenient option for individuals or organizations to convert their securities holdings into a reliable income stream. By understanding the concept, benefits, and types of annuities associated with this arrangement, individuals can make informed decisions based on their financial goals, risk tolerance, and long-term planning requirements. It is advisable to consult with financial professionals or experts before entering into such agreements to ensure suitability and compliance with applicable regulations.

Oklahoma Annuity as Consideration for Transfer of Securities

Description

How to fill out Oklahoma Annuity As Consideration For Transfer Of Securities?

It is possible to spend time on the Internet searching for the authorized file design that fits the state and federal requirements you want. US Legal Forms provides thousands of authorized types which can be evaluated by pros. You can easily obtain or printing the Oklahoma Annuity as Consideration for Transfer of Securities from the services.

If you have a US Legal Forms account, you can log in and click on the Acquire key. Afterward, you can comprehensive, revise, printing, or signal the Oklahoma Annuity as Consideration for Transfer of Securities. Every single authorized file design you purchase is the one you have forever. To obtain an additional version of the purchased kind, go to the My Forms tab and click on the corresponding key.

If you use the US Legal Forms web site for the first time, adhere to the easy guidelines below:

- Initially, be sure that you have selected the best file design for the region/area that you pick. See the kind description to make sure you have picked out the correct kind. If offered, make use of the Preview key to search with the file design also.

- If you wish to discover an additional variation from the kind, make use of the Search field to obtain the design that suits you and requirements.

- When you have located the design you need, click Acquire now to carry on.

- Choose the costs strategy you need, enter your credentials, and sign up for an account on US Legal Forms.

- Full the purchase. You should use your bank card or PayPal account to fund the authorized kind.

- Choose the file format from the file and obtain it in your system.

- Make modifications in your file if possible. It is possible to comprehensive, revise and signal and printing Oklahoma Annuity as Consideration for Transfer of Securities.

Acquire and printing thousands of file web templates using the US Legal Forms Internet site, which provides the most important assortment of authorized types. Use skilled and condition-distinct web templates to tackle your business or individual needs.