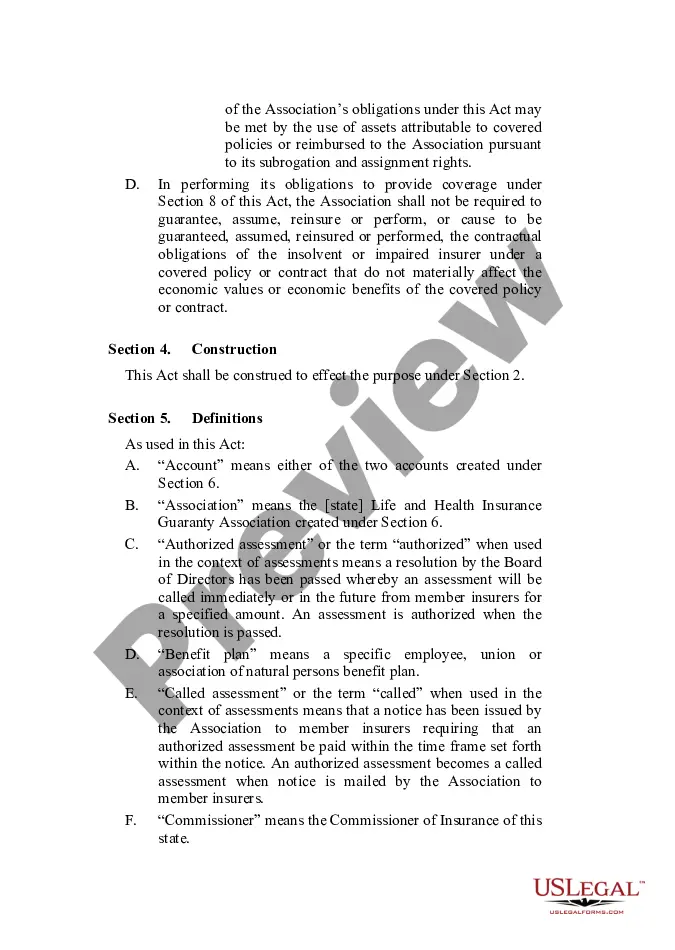

Full text and statutory guidelines for the Life and Health Insurance Guaranty Association Model Act.

The Oklahoma Life and Health Insurance Guaranty Association (OLGA) Model Act is a legislative framework established to protect policyholders and claimants when an insurance company becomes insolvent or goes into liquidation. The OLGA Model Act defines the powers, responsibilities, operations, and funding mechanisms of a state guaranty association for life and health insurance policies. It sets the stage for safeguarding the interests of policyholders by assuring a safety net in case their insurance provider faces financial difficulties. Under the OLGA Model Act, there are various types of coverage provided: 1. Life Insurance: This provision covers individual and group life insurance policies. It ensures that the death benefits and policy cash values payable to beneficiaries are protected. 2. Health Insurance: This aspect covers individual and group health insurance policies. It aims to safeguard coverage for medical expenses, including hospitalization, surgery, prescriptions, and other health-related services. 3. Annuities: The OLGA Model Act covers annuity contracts up to specified limits. This coverage ensures that annuity holders receive their promised benefits, such as periodic income payments, even if the annuity issuer fails. The OLGA Model Act outlines the responsibilities and powers of the guaranty association. These responsibilities typically involve the following: 1. Providing Coverage: The association must step in to cover policyholder claims when an insolvent insurance company cannot fulfill its obligations. 2. Policy Transfers: It may transfer policies to a financially sound insurance company, enabling the policyholders to retain their coverage without interruption. 3. Policyholder Notifications: The association must notify policyholders in the event of an insurer's insolvency, keeping them informed about the process and their options. 4. Claims Processing: OLGA ensures that claims get processed and paid promptly, ensuring minimal disruption and financial hardship for policyholders. 5. Funding: The Model Act outlines funding mechanisms for the association, which typically involve assessments of solvent insurance companies within the state. The OLGA Model Act serves as a critical tool to protect policyholders from potential financial losses in circumstances where their insurance provider becomes insolvent. It creates a safety net that ensures the continuity of coverage and the payment of valid claims. By maintaining the stability and integrity of the insurance market, the OLGA Model Act instills confidence in policyholders and contributes to the overall sustainability of the life and health insurance industry.The Oklahoma Life and Health Insurance Guaranty Association (OLGA) Model Act is a legislative framework established to protect policyholders and claimants when an insurance company becomes insolvent or goes into liquidation. The OLGA Model Act defines the powers, responsibilities, operations, and funding mechanisms of a state guaranty association for life and health insurance policies. It sets the stage for safeguarding the interests of policyholders by assuring a safety net in case their insurance provider faces financial difficulties. Under the OLGA Model Act, there are various types of coverage provided: 1. Life Insurance: This provision covers individual and group life insurance policies. It ensures that the death benefits and policy cash values payable to beneficiaries are protected. 2. Health Insurance: This aspect covers individual and group health insurance policies. It aims to safeguard coverage for medical expenses, including hospitalization, surgery, prescriptions, and other health-related services. 3. Annuities: The OLGA Model Act covers annuity contracts up to specified limits. This coverage ensures that annuity holders receive their promised benefits, such as periodic income payments, even if the annuity issuer fails. The OLGA Model Act outlines the responsibilities and powers of the guaranty association. These responsibilities typically involve the following: 1. Providing Coverage: The association must step in to cover policyholder claims when an insolvent insurance company cannot fulfill its obligations. 2. Policy Transfers: It may transfer policies to a financially sound insurance company, enabling the policyholders to retain their coverage without interruption. 3. Policyholder Notifications: The association must notify policyholders in the event of an insurer's insolvency, keeping them informed about the process and their options. 4. Claims Processing: OLGA ensures that claims get processed and paid promptly, ensuring minimal disruption and financial hardship for policyholders. 5. Funding: The Model Act outlines funding mechanisms for the association, which typically involve assessments of solvent insurance companies within the state. The OLGA Model Act serves as a critical tool to protect policyholders from potential financial losses in circumstances where their insurance provider becomes insolvent. It creates a safety net that ensures the continuity of coverage and the payment of valid claims. By maintaining the stability and integrity of the insurance market, the OLGA Model Act instills confidence in policyholders and contributes to the overall sustainability of the life and health insurance industry.